Quick Takeaways

- Medical Conditions Don’t Have to Be Work-Related: You don’t have to have an injury on the job.

- Secure Monthly Income: It’s a great way to secure that monthly income for you in a season of uncertainty. It is something that can be very stable.

- Additional Earning Opportunities: You can also earn money in the private sector while continuing to earn creditable years of service.

- Insurance Benefits Continue: You get to keep your health and life insurance benefits if you so choose, as long as you’re eligible. Note that while the USPS covers 55% of your premiums, when you move over to the benefit, the OPM will cover 50%.

- Processing Timeframe: The processing timeframe over at the U.S. Postal Service is unfortunately that one to six months, but if you ever have questions or concerns, you are always welcome to reach out to us.

Common Questions

Q: How much will I receive monthly on Disability Retirement?

A: 60% of your high-three salary for the first year, then 40% for each year until age 62. Your high-three is the average of your highest 36 consecutive months of basic pay – usually your most recent three years. To estimate your annuity payment, check out our Disability Retirement calculator.

Q: Can I work other jobs while receiving Disability Retirement?

A: Yes! You can earn up to 80% of what your current USPS position pays in private sector employment. Learn more about how much you could earn on Disability Retirement.

Q: What medical conditions qualify for Disability Retirement?

A: Any medical condition that prevents you from performing at least one major function of your current USPS position. Learn everything you need to know about qualifying conditions here.

Q: Will being on light duty or modified duty affect my eligibility?

A: Light duty assignments might actually support your disability claim because they typically don’t let you perform all the duties of your position which is necessary to be considered valid accommodation. Learn more about reasonable accommodation here.

Q: How long does the USPS Disability Retirement process take?

A: The process involves multiple steps and could take anywhere from 9-12 months from start to finish. See here to learn more about OPM processing time.

Full Webinar Transcript

Understanding Federal Disability Retirement for USPS Employees

Grant (Director of Operations): We’re excited to talk today with our postal employees about how Federal Disability Retirement specifically works when you are a postal employee. I’ve got Kimberly here with me today. She’s an expert in case processing. She’s the director of case processing here at Harris Federal, and she’s a federal retirement consultant.

Kimberly (Director of Case Processing): I’m really happy to be here. This is some really good information for those postal workers to know since their process is a little bit different, so this is going to be some great, important information.

Grant: One thing that’s really interesting is they have a few things that are more uniform and also more difficult than other agencies in the federal government, and there’s a lot of them – a lot of folks that work in the postal service.

What is Federal Disability Retirement?

Kimberly: Disability Retirement is actually a benefit that’s already sort of built into your retirement system, and it’s a great benefit that only federal employees have. Ultimately, you have to go through the process with the OPM (Office of Personnel Management) to be approved for this benefit through the federal retirement system.

Grant: There are very few people left anymore that are still on the Civil Service Retirement System. Almost everyone has transitioned to the Federal Employee Retirement System [FERS], but either way, it’s got to go through the OPM.

The Monthly Annuity Benefit

Grant: When we talk about the benefit itself, at a high level, there’s a monthly annuity, there’s the availability to earn money in the private sector in addition to that monthly annuity, you get to keep adding creditable years of service to your service history, and you get to keep your health and life insurance and move those things on into retirement.

Kimberly: For the Disability Retirement annuity, this is going to be based off your high-three salary, and you will receive 60% of that high-three for your first year, and every year after until the age of 62, you are going to receive 40% of that high-three. Just be aware that if you are going to keep your health and life benefits, that does have that premium into retirement, and this is taxable income as well.

Grant: One question we get all the time is “how is it taxable,” and the number one answer we can give you is you need to talk to a CPA and get some tax advice. But it comes in as retirement income or ordinary income, not as earned income, so it does reduce your tax bill because you’re not going to pay FICA taxes, but it is definitely still taxable income.

Understanding Your High-Three Calculation

Kimberly: When people say the high-three, what they are referring to is the average of your highest 36 consecutive months of basic pay. For most employees, this is going to be the most recent 36 months, but it could be your first couple of years of service if that was when you earned the highest consecutive pay.

Grant: One thing that’s really interesting about this is people say, “Well, I’ve been off of work,” and it actually calculates at your salary even if you didn’t earn money during that period. So, if you were on workers’ compensation or on leave without pay, whatever your salary was at that time, that’s still getting counted if it’s part of that highest 36 consecutive months.

The Bridge to Age 62

Grant: What we call this here in the office is a “bridge to 62,” and what we mean there is FERS was set up with all of its components to incentivize federal employees working until they turn 62 years old. That’s when the premiums come in and the boosts and the bonuses, and when you’re first eligible to receive Social Security benefits. You’ll be past 59 and a half, so you can draw out of your TSP [Thrift Savings Plan].

Everything in FERS was designed for federal employees to work to their 62nd birthday, and so this is usually only something we can help somebody with when they’ve got a medical condition that is preventing them from making it to 62. When they turn 62, if they’ve been on Disability Retirement, that time recalculates, and it adds those creditable years in, and they do get paid that 10% bonus if they’ve got the minimum year requirements.

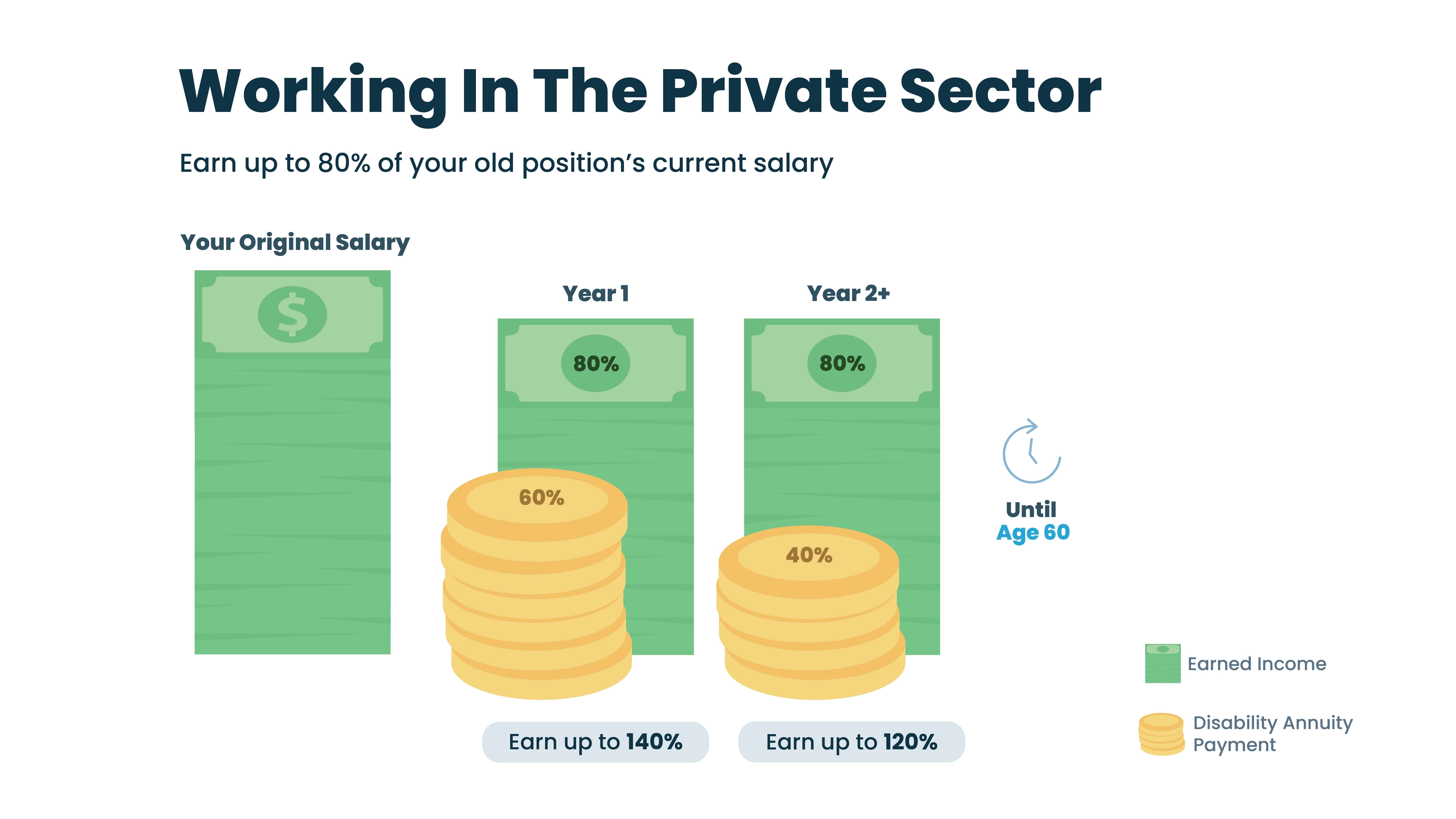

Earning Additional Income

Kimberly: One of the great benefits that Grant mentioned earlier is being able to work in the private sector. This is one of the things that’s specific to Disability Retirement. While you’re receiving that annuity payment, you can receive up to 80% of what your position currently pays, so as long as you’re within those medical restrictions, you can get a job elsewhere if you’re able to – such as teacher, realtor, some kind of desk job, or something like that that you’re able to do.

Grant: I’ve been here for 17 years, and “what could I do?” is a common question I hear. The answer is anything you want, as long as it’s within your medical restrictions.

Many clients have successfully found employment in the private sector and really come out in a good spot.

During that first year, there’s actually potential to earn significantly more than you did on your federal salary alone.

Continuing to Earn Service Credit

Kimberly: While you’re receiving the Disability Retirement, those years are actually counting towards your creditable years of service. So, if you retire with, or move on to Disability Retirement with just a few years of service, you are still earning years of service that will be calculated into your regular retirement at the age of 62.

Grant: You could be drawing 60% or 40% of your high-three from the first component, you could be earning up to 80% of your high-three in a private sector job, but still receiving credit as if you were working for the government and adding on to that long-term, 62-and-older time period of your life.

Example: How Service Credit Accumulates

Kimberly: Let’s look at a visual example of what we mean and how to calculate those extra years of service. This example client worked for 10 years and at age 40 had to take disability retirement. They continued to receive that Disability Retirement for 22 years until age 62. When OPM recalculates things for them at 62, they are going to calculate their regular annuity with 32 years of service as if they worked that whole time.

Grant: It really is the unsung hero behind this benefit because it allows the retirement to continue to grow. Not only does it preserve what’s already earned, but it continues to get better for the long-term annuity.

Health and Life Insurance Benefits

Kimberly: That health insurance and life insurance carries on into Disability Retirement and over to regular retirement as well if you’re eligible. Just take note that right now, currently, the postal service pays 55% of your premiums while you’re employed with them. When you move over to OPM, the OPM will cover 50% of those insurance premiums for you.

Grant: The health insurance and life insurance portion of this is something that’s super important. It’s a great benefit when you are a federal employee, and being able to keep it even with an early retirement and have it continue on is something that gives annuitants a lot of flexibility and options when it comes to their retirement and what their fixed costs are going to be.

Qualifying for Disability Retirement

Grant: This is unique – only federal employees and postal employees have this definition of disability when it comes to a Disability Retirement.

Kimberly: Let’s talk specifically about the way that OPM defines disability. This is any medical condition that inhibits an employee from continuing to complete at least one of those major functions of their duties in their current position.

Grant: In layman’s terms, I always think it’s easier to think about it as: Are you less than fully successful in one of the major aspects of your job? Those would include attendance, performance, and conduct. If you’re not hitting all those areas, if there’s even one area that you have a deficiency, you could have what is considered a disability by the OPM.

Occupational vs. Total Disability

Kimberly: A lot of times people hear “disability” and think that means they absolutely cannot work in any capacity. For OPM’s definition, they just mean that you have an occupational disability, meaning you can’t do this job specifically – at least one function of this federal job. That is going to be different than that total disability.

Grant: We want to emphasize that we’re talking about your job, not some other job that someone else can do. We’re talking about the one that you currently occupy.

Types of Medical Conditions That Qualify

Kimberly: I talk to clients every single day here, and I have had clients with medical conditions – physical conditions, really any condition on the books – you can qualify if it prevents you from doing that specific function at your job.

A lot of people are concerned if this happened during employment or if it happened outside of work. The thing that’s special about Disability Retirement is that your condition or injury did not have to specifically happen while you were on the job, but this does have to have arisen during your federal employment with your current position. It could be just a pre-existing condition that has worsened while you were in this federal position.

Grant: The idea is not that the medical condition started while you worked for the government or in that position, but that the inability to do the job arose while you’re in the federal position. You can’t come in with the disability, have no worsening of the disability, and then claim the disability. You have to have been successful for a period of time and capable of doing that work, and then have the medical condition either originate or worsen while you’re currently performing the position.

Light Duty and Accommodations

Grant: A big thing people ask is, “If I’m disabled, but my employer – the postal service – has given me a light duty assignment, and I’m casing my route and staying back at the office working on some other projects because my knee is the main culprit of my disability, and they’re accommodating me with this light duty assignment, can I still claim disability?”

Kimberly: That light duty assignment – while, it’s great because you’re able to still work at your current postal office – but that doesn’t mean that you are working your job. You can’t perform your functions of your job; you’re doing a light duty, which just is not your full-time duty.

The USPS Reasonable Accommodation Process

Kimberly: Once you submit that reasonable accommodation request, one of the first things that you can expect is to be contacted to do that DRAC meeting. If you don’t know what that is, that’s the District Reasonable Accommodation Committee. They will contact you to discuss over the phone what you can and can’t do and how to move forward with your reasonable accommodation. This can be either over the phone or in person.

If you are in a leave without pay status and are intending to apply for that disability retirement, you would not want to attend this meeting because the postal service will pay you, and that is going to affect your last day in pay, which will affect that back pay.

Grant: That’s certainly something we would want you to contact us about if you’re faced with that and you have questions. Don’t just go – call us, and we’ll walk you through it.

USPS Application Processing

Kimberly: The postal service is very unique in their processing, and we process them just a little bit differently. The HRSSC – that is going to be the Human Resource Shared Service Center – this is the overall HR. Most of you are probably pretty familiar with this. This is who processes these applications. They are a third party; they handle all of the personnel matters, and so this is where ultimately your initial application is submitted to.

Grant: It’s done by a third party out of Greensboro, North Carolina, and they have a unique process. They do some of the legwork with regards to filling out some of the supervisors’ forms and the agency forms, but it’s still good to be a good communicator. When you’re working with us, that’s something we try to be proactive with and try to help you know when to communicate with your supervisor.

Once the application is received and all things are verified and collected, they send the package to the finance center – the postal service finance center, which is in Eagan, Minnesota – to collect the payroll records that will accompany any application for retirement, whether it’s immediate or disability.

The Automated Blue Book Process

Grant: Maybe the most confusing thing that the postal service does differently from other agencies is when they receive the first page of an application for retirement – whichever type – they automatically send that employee a giant blue book that gives instructions about how to set up retirement counseling sessions where they plan to walk through the process with you.

They’re not there to advise you; they’re simply there to process your paperwork.

Kimberly: If you take a look at those blue books, they are all of the forms that you likely have already completed, either on your own or with your case manager here, because we submit that whole application for you.

It’s important to know that that information does not have to be repeated, but it’s just a good thing to know to keep in the back of your mind: “I received this blue book; I know that they are starting to process my application.”

Grant: I can’t tell you how many times we’ve submitted a completed application with all of the necessary forms and documents, and then three weeks later, our client calls us in a panic saying, “They just sent me all these forms; I thought we already did them.” The answer is we did. This is automated; it’s not something that is thought through by anybody, and they didn’t make a decision. You didn’t do anything wrong; they just automatically send it whenever they receive a piece of paper from an employee about a retirement.

Processing Timeline and Review

Kimberly: With their restructuring, their processing of applications right now can take anywhere from one to six months and still be pretty normal.

Grant: Once they process that, it goes on to Eagan. Eagan pulls the pay records and then they forward it to the OPM for that actual review. Nobody in the postal service is going to review the application for merit. They may review it for completion or all the documentation, but they will never review it for merit at the postal service. It’s not their job to do, and if they were to review it, it wouldn’t actually have any bearing on a case anyway.

Navigating the Process

Grant: As we go through this process with folks, one thing to remember is that it is a process. I’ve been doing this for 17 years, and I’ve been a part of over 6,000 cases. Each one presents unique challenges, but at the end of the day, we always get to the end by finding the areas where we can communicate and walk people through how to finish out this process – whether it’s with the shared service center, with Eagan finance center, or with the OPM office in either Boyers, Pennsylvania, or in Washington, D.C.

Kimberly: That’s one thing that’s great about us in our office – we know how most of these places process, when they process, what they’re doing, and on what time frame. That’s a huge benefit in working with us and just having that comfort of knowing what’s going on in your claim.

Grant: The process will be one to six months at the postal service, and then we turn it over to the OPM, and they have their own timeframes as well. But the processes, in general, are something that we’d love to talk with you about if you have any questions.

Feel free to call us and schedule a free consultation.