Quick Takeaways

- Federal Disability Retirement pays 60% the first year, then 40% thereafter: You’ll receive 60% of your high-three average salary in year one, then 40% every year after until age 62, when it converts to regular retirement.

- Years on Disability Retirement count as creditable service: Every year you’re on Federal Disability Retirement counts toward your federal pension, so if you retire at 52 and reach 62, those 10 years add to your total service calculation.

- You can work in the private sector and earn up to 80% of your old salary: This is an occupational disability benefit, meaning you can pursue new career paths that accommodate your medical restrictions while collecting your annuity.

- You must meet seven qualification requirements, not just three eligibility requirements: Being eligible (18 months of service, under FERS, disabled while employed) doesn’t guarantee approval—you must also prove diagnosed conditions, service deficiency, accommodation denial, and more.

- Your health and life insurance continue at the same employee rates: You won’t lose your federal health and life insurance benefits or pay higher premiums—they remain locked in as if you were still actively employed.

Common Questions

Q: How long does my medical condition need to last to qualify?

A: Your condition must be expected to last at least 12 months from the date you submit your application to OPM. This is a prognosis requirement, not how long you’ve already had the condition.

Q: Can I qualify if I’m still working full-time with no absences?

A: Yes, but it’s more difficult. Without a service deficiency (like excessive leave or poor performance), you must prove your medical condition is incompatible with necessary job duties, which requires stronger justification.

Q: Does my injury or illness have to be caused by my federal job?

A: No. Your condition only needs to have arisen or worsened while you’ve been employed in your federal position—it doesn’t have to be work-related like workers’ compensation.

Q: What happens if my agency offers me a different position?

A: The reassignment must be reasonable: same pay and grade, within your commuting area, a position you’re qualified for and medically able to perform. If it doesn’t meet all these criteria, you can decline it.

Q: What’s my high-three average salary?

A: It’s the average of your highest 36 consecutive months of basic pay, including locality pay and for some law enforcement positions, certain overtime hours. Contact your HR department for your exact figure.

Full Webinar Transcript

Nick Child (Director of Client Acquisition): Welcome into this webinar today where we’re going to talk more about how to qualify for Federal Disability Retirement. This is a question that lots of people ask all the time. When there’s any situation where they’re wondering, “Hey, I can’t work anymore. I know this benefit’s out there—how do I actually get it?”

I’ve got the man you want to talk to about that, and that’s Caleb McKinley, our Senior Disability Consultant here at Harris Federal. Caleb talks to thousands of federal employees every year about this specific topic and helps them really understand whether or not they can qualify for the benefit and what their path forward really looks like.

Caleb McKinley (Senior Disability Consultant): Thanks Nick. Like you said, I do speak with a lot of folks on a daily basis about this topic—how to qualify for Federal Disability Retirement. There’s a lot of information about this, so simplifying it and explaining it quickly is kind of what I do. I’m very excited for today’s webinar to discuss this in detail and walk through a lot of these important questions.

Nick: On a webinar we only have a certain amount of time. This is a big topic, there’s lots of complexities with it, but what we’re going to try to do is distill it down into a few topics. First, what is Federal Disability Retirement—we’re going to go over that so everybody really understands the main points of the benefit. Then we’re going to talk about eligibility requirements—am I eligible for it first? Have I worked in the federal government for long enough? Then qualification requirements—okay, I’m eligible, but now do I meet those qualification requirements with my injury or illness, my prognosis, all of those sorts of things? And then we’re going to get into how we come alongside you and help you through this process.

Understanding Federal Disability Retirement

Nick: Federal Disability Retirement at its most basic principle is a benefit that allows you to retire early if you can’t keep working due to illness or injury.

Caleb: It is an option for your Federal Employee Retirement. Every FERS employee pays into FERS or CSRS, and like Nick said, if you’re not able to work until your full retirement age—which for most folks is going to be age 62—you also have the option for a minimum retirement age retirement with a certain amount of years of service. But essentially, if you’re unable to work until that age, if you need to retire early, then Federal Disability Retirement is an option for you if you’re struggling with your health, medical condition, injury, etc.

Like I said before, this benefit, because it is part of your Federal Employee Retirement plan, is provided by the Office of Personnel Management [OPM], and it’ll last until you reach your retirement age, which is age 62. Then you’ll receive your regular FERS retirement. So in a lot of ways, it’s a transition—it’s a way for folks to retire early and then transition them until their full retirement age of 62.

Nick: A lot of times we call this a bridge to 62 around here. It’s that idea of, “Hey, I can’t keep working right now, but I need to supplement some income while maybe I go work somewhere else in the private sector.” We’ll talk about that in just a minute. It’s a supplemental benefit to help us get to that age of 62 where we’re then going to get our full retirement from the federal government, and it’s going to convert over.

Main Highlights of the Benefit

Nick: The main highlights of this benefit—and there are some other benefits to this as well, but these are the ones that generally everyone needs to understand:

This benefit pays out a monthly annuity. This is that supplemental income that we’re talking about. It’s going to pay out monthly.

You’re going to receive creditable years of service. This is in addition to any years of service that you already have. So while you’re on this benefit, you will continue to receive those creditable years of service that will add up once this benefit recalculates into regular retirement at 62.

You can go work in the private sector. Now, we know not everyone can—some people are totally disabled and can’t continue working—but if you can, you can go work in the private sector in a new job or new career.

You can also continue your health and life insurance through the federal government while you’re on this benefit, which is significant to a lot of people that would have a hard time going and finding that out in the private sector.

How Much Does It Pay?

Caleb: This is a question that I get asked very often, and it’s very important. The answer would be: for the first year, OPM will pay you 60% of your high-three average. Then every year following until you turn 62 years old, OPM is going to pay 40% of the high-three average.

Key Point: The high-three is the average of your highest 36 consecutive months of basic pay. This doesn’t necessarily mean your calendar year salary—it is month to month, 36 consecutive months of basic pay. It does include locality pay. For a lot of law enforcement officers, it does include some overtime hours. Also keep in mind, this is taxable income, so there will still be some federal taxes taken out of this annuity.

As Nick said before, you do have the option to keep your life and your health insurance, and it will be at the same rate as if you were still working as a federal employee. So your health insurance and life insurance premiums are going to be locked in as normal.

Nick: A lot of people are probably thinking, “How am I going to live off of 60% the first year and then 40% every year after of my high-three average?” I know that probably does sound daunting, but remember, this is supposed to be supplemental. Most people that we talk to can go work in the private sector and continue to earn income on top of this. So this is to be a safety net to help you bridge that gap between now and 62 and the income that you need to find something that you can do that’s within your medical restrictions.

People that can’t go work also have another benefit that they can tap into, which is Social Security Disability, and those two can add together to get them a little bit more income. So it’s not solely dependent on this annuity.

Let’s look real quick—we have a visual here of the high-three and then what that looks like to earn each year. You can see the high-three average stack over on the left-hand side—let’s just say that’s $60,000. This is the average of your highest 36 consecutive months of basic pay.

Year one, you’d be receiving $36,000 in monthly payments—that’s broken out over 12 months. Then every year after that until you reach the age of 62, it’d be $24,000 a year.

That’s what it looks like from a number standpoint. Obviously, it’s going to look different depending on what your high-three average is. If you want to know what your high-three is, you can talk to your HR department and they can get you that so you have some numbers to work with. But typically this is your last three years of pay for most people, and that’s a good way to get an estimate of what you’re talking about.

Creditable Years of Service

Nick: Let’s switch now from the annuity itself—how much you’re going to get—to creditable years of service. This is a piece of it that a lot of people miss that they need to know about, because this is critical to the full calculation and how this will benefit you once you get to 62.

Caleb: This is one of the most important aspects of your retirement benefits. As you can see here, every year on Federal Disability Retirement is going to count as another earned year of creditable service for your federal retirement. That means if you are thinking about retiring and you’re 52 years old, for example, then that means there’s a 10-year gap—there’s 10 years from 52 to 62—and if you’re approved for Federal Disability Retirement, those 10 years are going to count as creditable years of service.

For anybody, if you’re thinking about retiring, if there’s a gap that you’re looking at between your current age and your full retirement age of 62, just know that that gap is going to be counted as creditable years of service by OPM. What I tell folks is that this is good time. Your time on Federal Disability Retirement is good time. It’s not wasted time, it’s productive. As Nick said, while you’re receiving these annuities, you can still work in the private sector, still earn money. This is a very stable benefit and it is long-term, so it’s certainly worth considering if you’re unable to keep working.

Nick: Here’s the situation that most people are in: they never thought they were going to be on this benefit. No one ever goes into a career thinking, “I’m going to get injured and I’m going to have to access a disability benefit.” But this is what’s so critical about this one.

Imagine you start working in the federal government at the age of 42. You’re 52 now, so you’ve worked there for 10 years. You decide, “Okay, now’s the time for me to go on this benefit. I just can’t keep working.” Most people are thinking in their minds, “Man, but I need to make it to 62 because I need that pension for the rest of my life. I need that FERS retirement.” A lot of people are like, “I’m just going to try to put up with this injury or illness to get to 62 years old”—that’s another 10 years.

What we’re talking about is: if you got on this benefit at 52 years old, you would then have another 10 years of creditable service while you’re on this benefit until you get to 62. So those are going to add up once you turn 62 to 20 years of service and recalculate your regular retirement benefit at 62, like you’d been working there for 20 years. I hope people can see that and understand how this is going to impact them long-term.

Working in the Private Sector

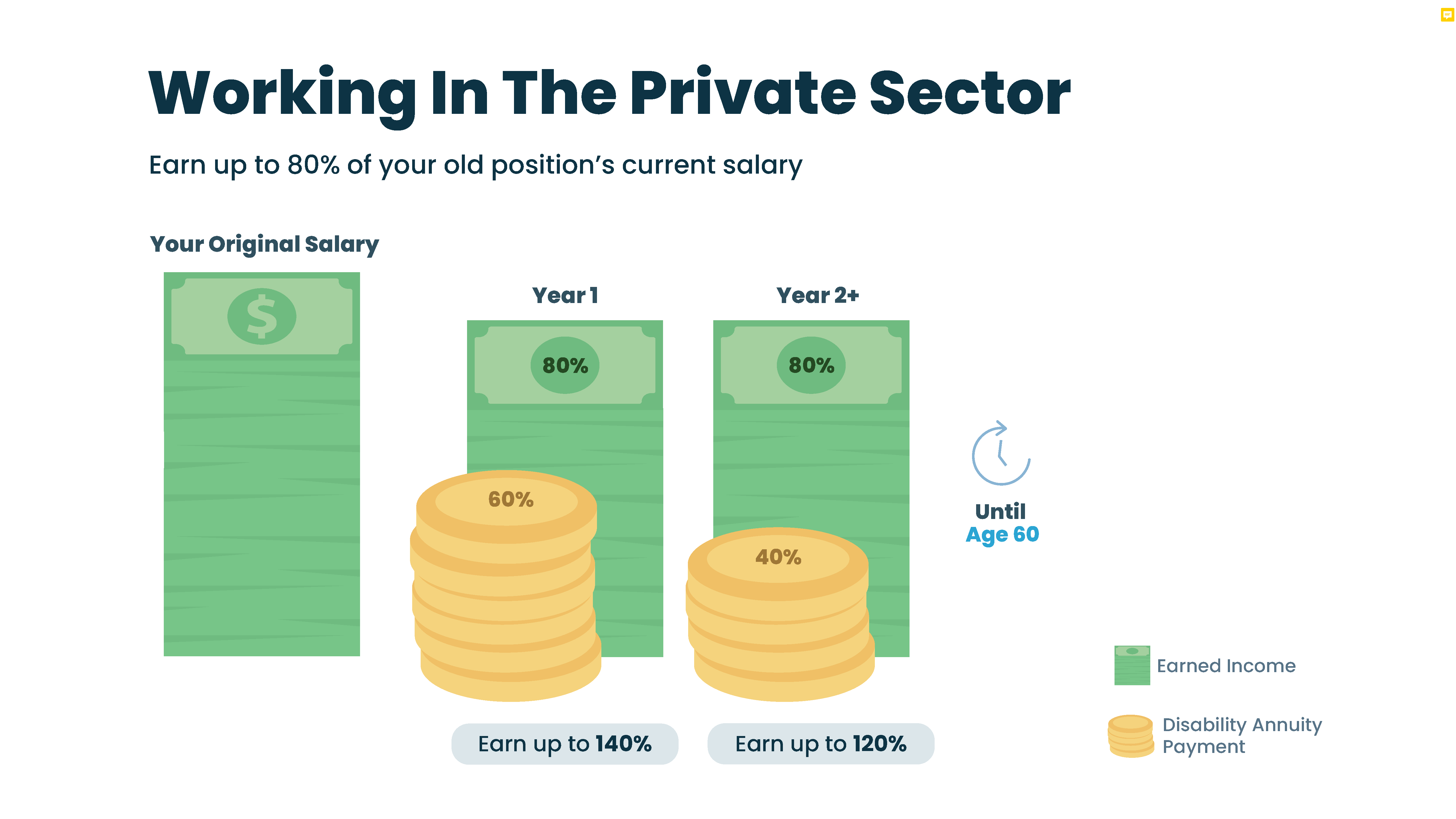

Nick: The next unique piece to this benefit that people probably have a lot of questions about is going and working in the private sector. What we’re talking about here is an occupational disability. This is not a total disability—while it can be, that’s not the point of this. What we’re saying is you just can’t do your job. We’re not saying you can’t do any job, just your job specifically.

You do have some jobs that you could go work that are within your medical restrictions that will allow you to continue receiving income. This is where we go back to the idea of the annuity being supplemental. That income cap looks like 80% of your old position’s current salary. The position that you’re retiring from, whatever that salary is, you can earn up to 80% of that in the private sector.

Caleb, I know you talk to a lot of people about this and they’ve got a lot of questions about what that actually looks like. What kind of jobs do you see people going out there and working in the private sector?

Caleb: This can be a very confusing issue because a lot of benefits—and especially whenever we talk about the D-word, whenever we talk about disability—Social Security Disability means total disability. Of course, VA disability is rated on a percentage scale. But this definition of disability, as Nick said, is purely occupational. The argument would be you can no longer work in your present federal position.

I’ve seen folks medically retire from the federal government and work as realtors, teachers, volunteers. They’ve started nonprofits, done delivery, gone into customer service jobs. There are a lot of opportunities that you have. A lot of people will go back to school and get either retrained or re-certified in a new craft or new career field. That’s what I encourage people to do—find a job that you are passionate about, that you enjoy doing, and fits entirely within your health. We certainly want to prioritize your health and well-being and to not work in a job that would be either disabling or contributing negatively to your health in any kind of way.

Nick: Going back to that occupational idea, what we’re trying to do is prove that you can’t do one of the required functions of your position. Let’s say you’re a letter carrier—you’ve got to carry around a 75-pound satchel—and let’s say you have a knee injury that prevents you from doing that. But that doesn’t mean you can’t go work in the private sector as a teacher or a realtor, something that just doesn’t require you to be walking up and down stairs carrying a satchel. That’s what we’re talking about here when we talk about an occupational disability.

On this slide, what we want to show you is how all of these things add up. We’ve got your original salary over on the left, and every year you can earn up to 80% of that salary. Now that is going to be in addition to the annuity that we talked about before. So the first year on this benefit, you could earn up to 140% of what you were getting paid in your federal job. Then every year after that, you could earn up to 120% of what you’re making in your federal job.

That’s something that a lot of people don’t realize about this benefit, and it’s really important to consider as you’re doing all the math to look at this benefit and whether or not it’s actually going to be viable for you. The earned income here is also going to change as that job continues to get raises and earn more money in the future—that 80% will adjust. Everybody needs to know that as well.

Maintaining Health and Life Insurance

Nick: The last piece here we do want to talk about is maintaining your health and life insurance. This is a really critical piece for people because a lot of people, especially that have illnesses or injuries, are hard to insure. Especially as you talk about keeping your family on your health insurance plan—I’m sure Caleb, you hear about that a lot. This is something for people that’s really important.

Caleb: It is, and this is a big reason why folks continue to work for as long as they do—because they are scared of losing their health insurance. I speak with a lot of people who, this is the reason why they keep working: to maintain their health and life insurance.

I tell folks that if you had to medically retire, if that was the option that was best for your situation, then you’ll get to keep these benefits. You will not lose—for yourself, for your family members—you will not lose your health and life insurance benefits. Those will get locked in and you’ll be able to maintain those at the same rate. So you’re not going to be paying 100% of those premiums—the federal government will continue to subsidize their portion and then you’ll pay the same rate as if you were still working as an employee.

If you’re considering your choices here, just know that Federal Disability Retirement does include these health and life insurance benefits. This is a massive benefit for you.

Federal Disability Retirement Eligibility Requirements

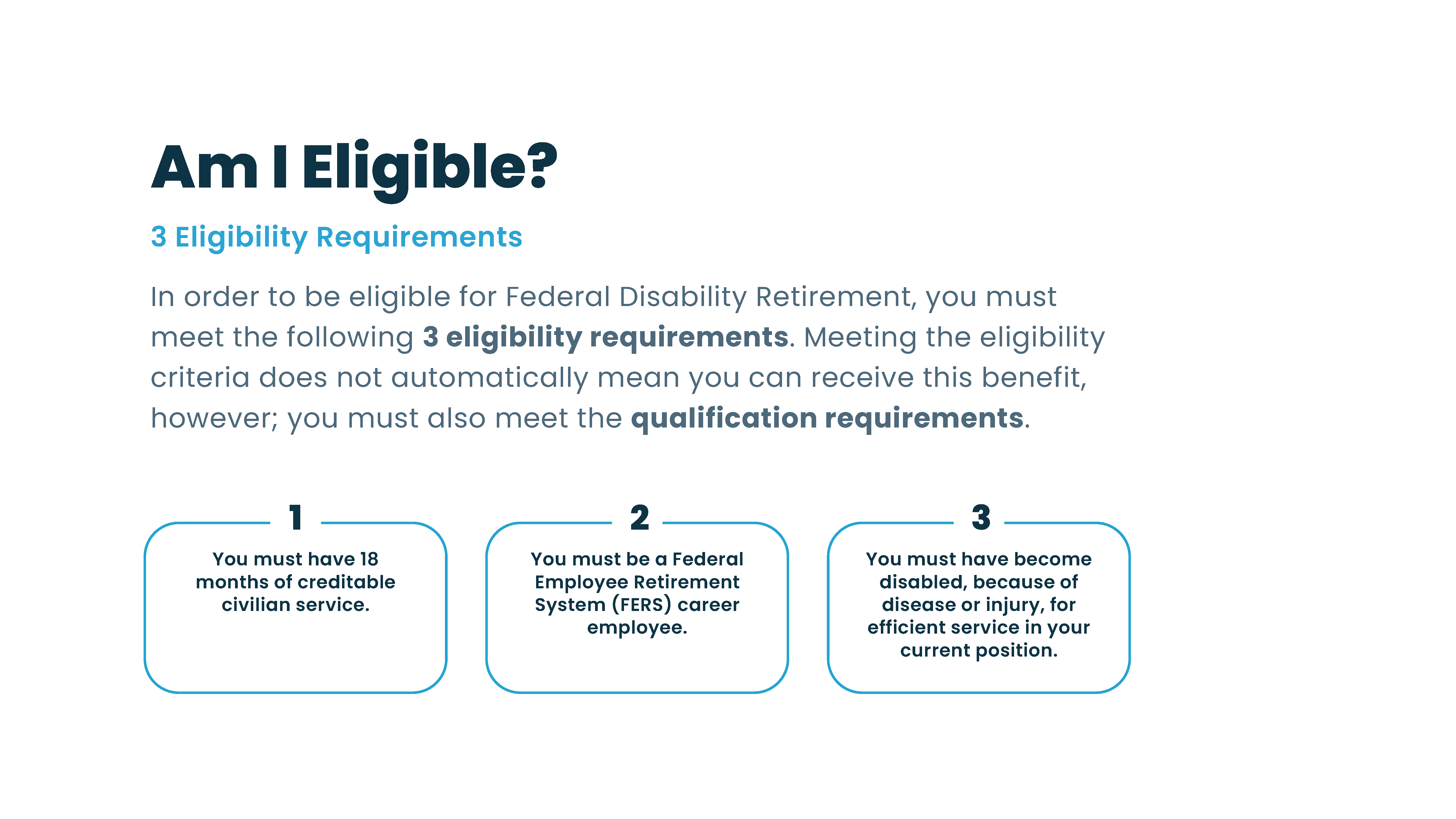

Nick: We’ve probably exhausted talking about the benefit itself. Now I’m guessing most people here are wondering, “Okay, am I eligible? Do I qualify for it?” Let me cover the eligibility real quick, because it’s pretty basic, and then I’ll let Caleb go a little bit deeper into the qualification.

There are three eligibility requirements that you must have to even apply for Federal Disability Retirement:

- You have to have 18 months of creditable civilian service in your federal job. You’ve had to work there for 18 months.

- You must be under the FERS Retirement System. You have to be a career employee under the FERS Retirement System.

- You must have become disabled because of a disease or injury for efficient service in your current position. Now, the way that that’s worded might be a little bit confusing for people, but essentially what we’re saying is: since you’ve been employed, there’s some illness or injury that you have that has begun or worsened while you’re employed, and it’s keeping you from doing your job.

Federal Disability Retirement Qualification Requirements

Caleb: Now that we understand the three eligibility requirements and now you’re through the door, there are still seven main qualification requirements for Federal Disability Retirement. What this means is that OPM is adjudicating and essentially judging cases based on whether they fit within these qualifications.

In your application packet, what you’ll need to do is you will need to justify to OPM that you meet their qualifications for an occupational disability. Again, just because you are eligible—you’ve met the three requirements—it does not mean that you qualify for the benefit, because you still have to meet these seven qualifications.

Qualification #1: Diagnosed Medical Condition

The first qualification is a diagnosed medical condition. You must have a medical condition, which is defined as a health impairment resulting from a disease or injury, including a psychiatric disease. I speak with a lot of people who have mental medical conditions—anxiety, depression, PTSD, etc.—and for them, they certainly do qualify for Federal Disability Retirement if it is diagnosed.

This goes back to the very basics: it must be diagnosed by a doctor, a medical provider who’s been treating you for that medical condition. If you have not yet seen a doctor for any undiagnosed medical condition, it might not qualify for Federal Disability Retirement. It must be diagnosed by a medical professional.

Qualification #2: Length of the Condition

The second major qualification is the length of the condition. Your medical condition must be expected to last for at least the next 12 months. This does not necessarily mean that you’ve been diagnosed with the medical condition for 12 months, but it’s more of a prognosis. It’s more about, in a lot of ways, ascertaining the future—determining whether or not there’s a level of stability and consistency with the medical condition that it’s expected to continue for the next 12 months.

Nick: Is that from today’s date or is that from the date that I apply for Federal Disability Retirement?

Caleb: That’s a great question, and it is from the date that you submit your application to OPM. So your date of application becomes the date that you have to then prove that your medical condition is expected to last.

Nick: That’s something that a lot of people don’t realize, and there’s even nuances within all of that that we help people walk through as they’re going through this portion of the application.

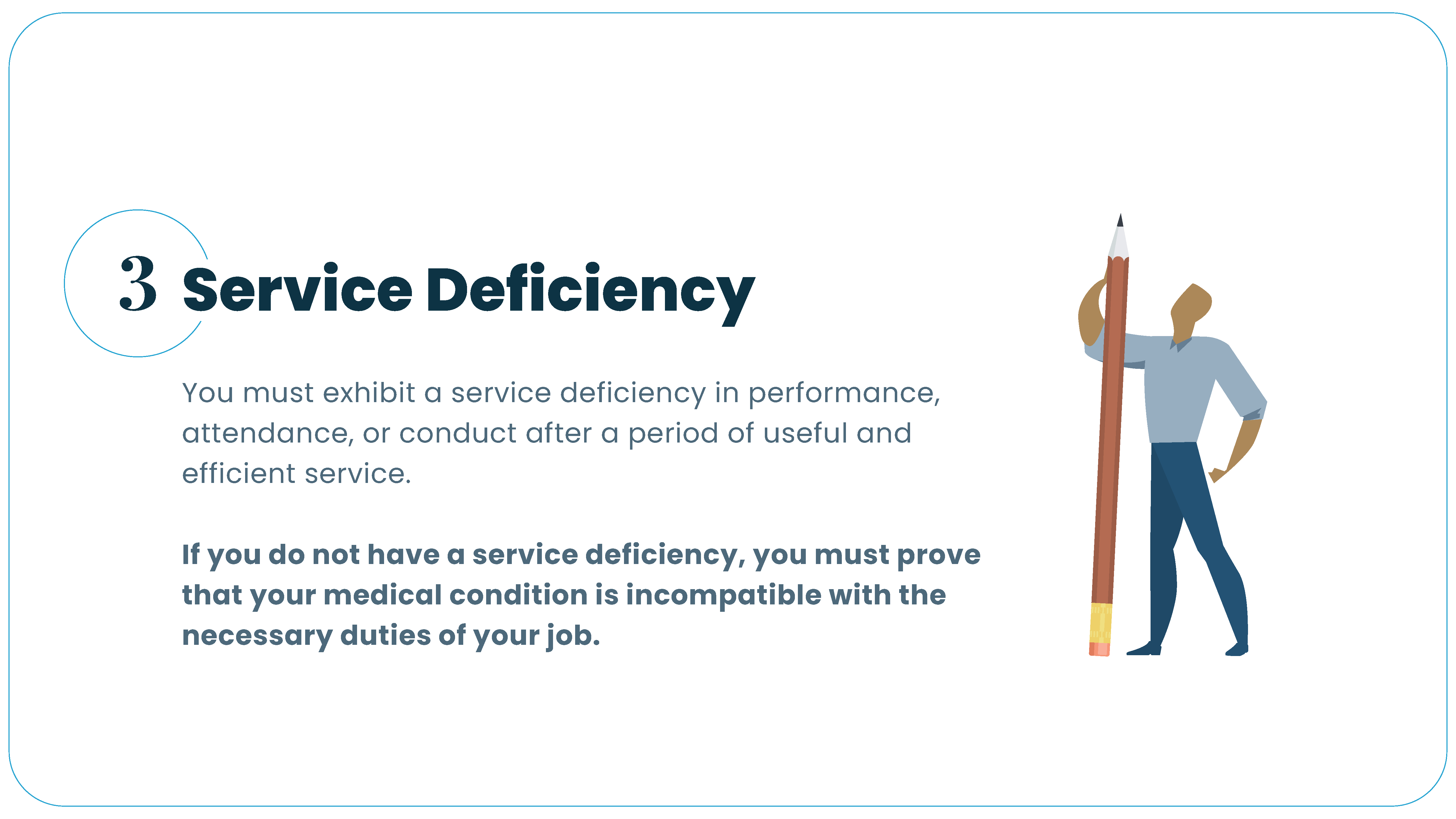

Qualification #3: Service Deficiency

Caleb: Let’s talk about service deficiency—important one. The service deficiency is defined as a deficiency in your performance, attendance, or conduct after a period of useful and efficient service. What this basically could mean: it could mean that you’re taking excessive sick leave, annual leave, leave without pay. It could mean that you’re getting either a negative performance evaluation or Performance Improvement Plan. A conduct deficiency could be a disciplinary action, it could be verbal or written warnings from a supervisor.

There are a lot of forms that a service deficiency can take, but it’s a tangible example of how your work has been impacted by your health and by your medical conditions.

If you do not have a service deficiency—in other words, if you’re still working full-time, full duty, you’ve never taken a day off, you’ve never gotten below a five out of five performance appraisal—then you must prove that your medical condition is incompatible with the necessary duties of your job. This can become very difficult, of course. It’s certainly doable, but it requires a higher level of justification to prove that your medical conditions are incompatible with your job if you’re still performing at a high level.

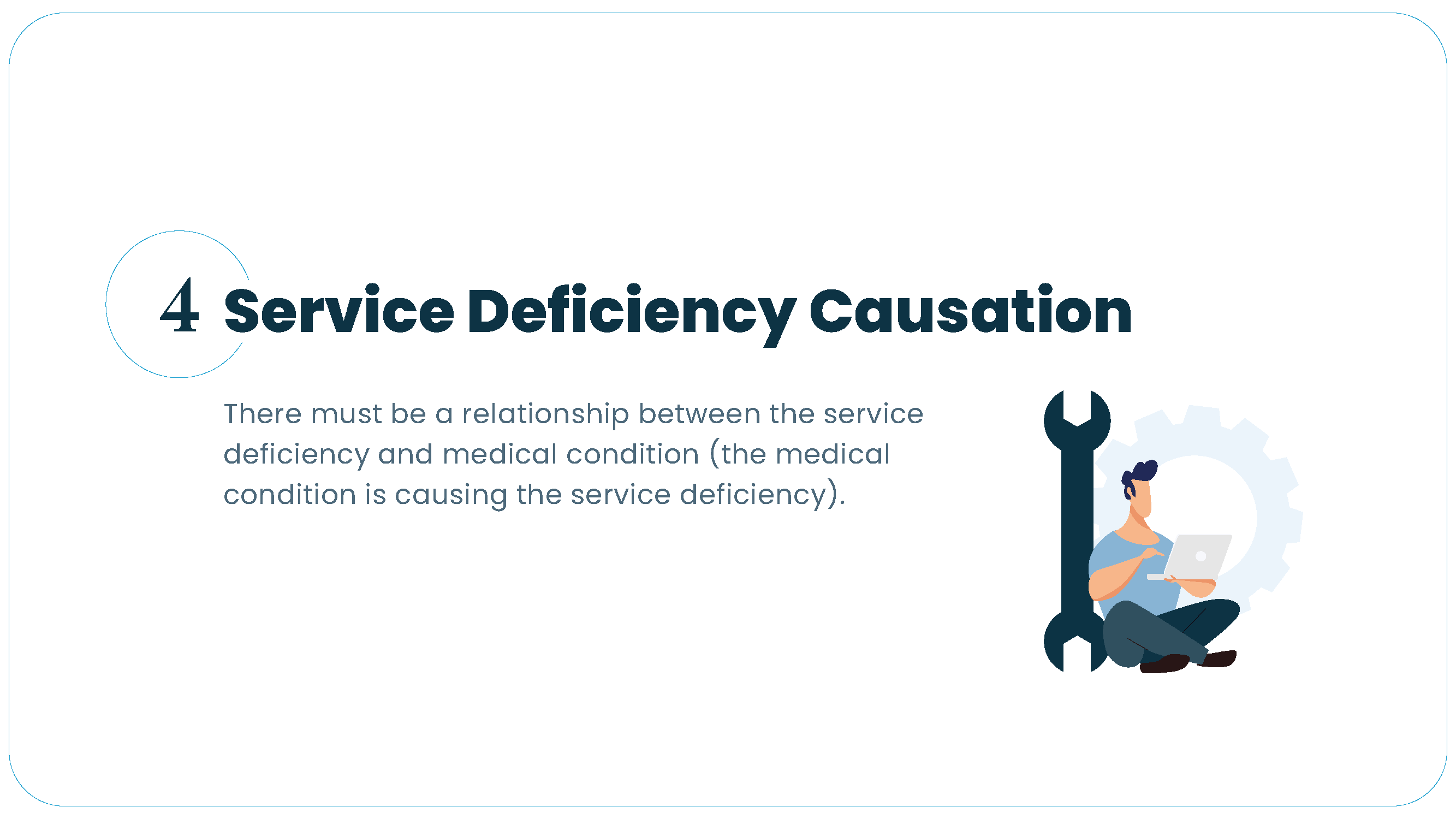

Qualification #4: Service Deficiency Causation

Nick: That’s really talking about number four here, right? Which is the service deficiency causation—the thing causing your deficiency in your work, the medical condition.

Caleb: Exactly. This leads right into number four, which is: there must be a relationship between that service deficiency and the medical condition. We talk often about how we have to connect the dots, and this is how we establish that connection between your health and your ability to perform at least one element of your job.

If you have an attendance deficiency—let’s say you’re taking time off to go on vacation or to either take a break for any other reason that is not medical—that would not necessarily count within this criteria. The service deficiency must be caused directly by a medical condition or injury.

Qualification #5: Condition Arose or Worsened During Employment

Nick: Let’s talk number five real quick. I mentioned this before, but that condition that Caleb’s talking about has to have arisen or worsened while you’re in your federal position. So it either started, or it’s something that has been lingering for a long time and has gotten worse while you’ve been working there.

One other thing I want to mention too is this does not have to be caused by work, like a workers’ comp injury would be. This could have been something that happened outside of work. This could have been something that happened back in college that’s just starting to really degrade at this point in your career. That’s what we’re talking about when it comes to whether or not it arose or worsened during work.

Caleb: That’s exactly right. A prime example of that would be a service-connected or a veteran’s disability. We speak with a lot of—probably the majority of our clients are military veterans—and they have pre-existing medical conditions. But as Nick said, over time, whether it’s through wear and tear or through stress or working in their job, their medical conditions have worsened over time. Again, it doesn’t necessarily have to be an on-the-job injury to qualify. We just have to prove that it has worsened during your period of employment as a civilian federal employee.

Qualification #6: Reasonable Accommodation

Nick: These last two that we’re going to cover here are probably the more unique ones that people need to understand. If you’ve never had a disability or injury before, you may not even be aware of. Let’s talk about reasonable accommodation and then reassignment.

Caleb: The biggest thing to understand with a reasonable accommodation is: your agency must be unable to accommodate for you in your current position. You must exhaust all of those accommodation efforts and options you would have within your agency before you take the next step and apply for Federal Disability Retirement with OPM.

A lot of times with reasonable accommodation requests, you can ask for something specific. You can ask for a schedule change, you can ask for either light duty or a reduction in certain aspects of your job. But in a lot of situations, these accommodations are denied. If your agency does deny an accommodation request, that will fully justify your decision to medically retire. This meets that criteria here.

If your agency cannot accommodate for you, if they deny your accommodation request, essentially that means that you’ve met that qualification and you would then be able to apply for Federal Disability Retirement with OPM. But the first step would be to request that accommodation from your agency.

Nick: One word I want to point out here is “reasonable.” They may be able to accommodate you in certain ways, but that may not always be a reasonable accommodation. There are specific requirements within this that they have to meet when it comes to reasonable accommodation. Just because they gave you an accommodation doesn’t mean that it works for you and it helps with your medical condition or restrictions there.

Qualification #7: Reassignment

Caleb: That is a very important word to remember, which is the accommodation has to be reasonable. Our last qualification is reassignment.

It would not be reasonable for your agency to reassign you to a job that pays you less. Based on this qualification here, your agency must be unable to reassign you to a vacant position within your commuting area at the same pay and grade level that you are qualified for and medically able to perform.

This means that your agency must furnish for you a job that you are medically able to perform, that pays you the same, is at your same agency, and within your commuting area. Again, it is not reasonable for them to relocate you, for them to pay you less, or for them to place you in a job that you’re medically unable to perform. You would be justified in declining that offer if your agency gave that to you.

Nick: If they offer that as a reassignment, it may not be a valid reassignment. What we’re saying here is these are requirements of Federal Disability Retirement. If they can put you in a position that meets these aspects of a reassignment, then it’s going to be difficult to get Federal Disability Retirement—not impossible, but really difficult—because they found you a job that you could do that meets all these.

But if they want to move you across the country to be in a different position, well obviously that’s not going to work here, and so that is not a valid reassignment, and that would help you in your Federal Disability Retirement claim.

Caleb: That’s right. A lot of the people I speak with have been working in their jobs for years and they have decades of experience, and they’ve moved up on their GS level. Because of their experience, because of their tenure, it would not be reasonable for their agency to give them an entry-level position. Again, if you’re further along in your career and you’ve reached a high level of step and grade, then their odds of finding you a valid reassignment become slimmer, which would therefore meet this qualification for Federal Disability Retirement.

Don’t Risk Your Future—We Are Here to Help!

Nick: We covered a lot there, but ultimately what we were all here for was to talk about the eligibility and qualification for Federal Disability Retirement. I know that this can be confusing. There’s a lot going on there, there’s a lot of pieces to this. There’s also a lot of nuance in everyone’s situation. Everyone’s different. Everyone has different medical conditions in different positions in different agencies.

This is why we always ask people to give our office a call. It’s not a sales pitch. It’s because it really requires talking to someone like Caleb or one of our other team members about your specific situation—your story, what is affecting your job, what can’t you do, have you been there long enough—all of these aspects that add up to whether or not you can qualify.

What our job is here is to really be your guide along that journey. We’re not saying that you have to go apply for Federal Disability Retirement. All we’re doing is showing you your options. If you do decide to go down the route of Federal Disability Retirement, we would love to continue to be your guide down that route and help you know the steps to take to try to get an approval. We want you to have your best chance at an approval.

This isn’t something to take lightly. I mean, this is your future you’re talking about. Like I said earlier, this is not something you ever thought that you would be getting into. We know that. We know it’s a tough situation for folks. It’s stressful. There’s a lot going on. We just want to be here to help you. We’ve done this over 8,000 times now for federal employees, and we’ve done that at a pretty good clip—99% success rate, I think, goes to speak for our ability to help people get approved.

Just because you get on a call with somebody and do a consultation doesn’t mean it’s a sales pitch at all. They are really passionate about helping people and giving people the information they need to make good choices about their future. That’s why Caleb, that’s why we’re putting on this webinar—so that you understand your options for your future, whatever is going to help you the most.

Caleb: That’s right. Hopefully this did answer a lot of your questions, and I’m sure for every question it answered, there’s going to be two more that pop up that we didn’t answer. Within these seven qualifications, there is a world of nuance in between every one there. There is no cookie-cutter way to do this. Everybody is unique, every situation is different. As Nick said, don’t be afraid to give a call. Have a commitment-free conversation about what your options are, and then we can discuss how we can potentially help you with representing you at the OPM level.

If you’re ready to discover your retirement options, give us a call today for a free consultation.