Quick Takeaways

- No offset on VA disability or military retired pay: Veterans can receive these concurrently with Federal Disability Retirement, stacking multiple income sources.

- Occupational disability, not total disability: You only need a condition that prevents you from doing one major function of your specific job — a far lower bar than Social Security.

- The same injury can qualify twice: A condition rated by the VA can later worsen during federal service and become the basis for Federal Disability Retirement.

- You keep earning years of service: Time on Disability Retirement counts as creditable service, which is especially valuable for younger employees far from age 62.

- Military buyback is often a strong investment: Buying back military time adds 1% of your high-three per year of service for life, frequently at a low cost — but it must be completed before retirement is finalized.

Common Questions

Q: Who qualifies for Federal Disability Retirement?

A: Any career federal employee under FERS with at least 18 months of service who has an illness or injury expected to last longer than a year that keeps them from performing a major function of their current job. The condition must have arisen or worsened during federal service.

Q: How much does the benefit pay?

A: 60% of your high-three average salary the first year, then 40% every year after, until age 62, when it converts to regular retirement. The benefit is subject to federal income tax.

Q: Can I work while receiving Disability Retirement?

A: Yes. You can earn up to 80% of what your former federal position currently pays in a private-sector job that fits your medical restrictions.

Q: Does VA disability or military retired pay reduce the benefit?

A: No. There’s no offset — you can receive VA disability pay and military retired pay alongside Federal Disability Retirement. (You can’t buy back military time if you’re already receiving military retired pay unless you waive it.)

Q: What is the “high-three average”?

A: The average of your highest 36 consecutive months of basic pay. Overtime is generally excluded unless it’s a mandatory part of your regular salary, as with some law enforcement or firefighting positions.

Full Webinar Transcript

Ashley Withers (Client Education Consultant): Today in this webinar we’re going to go over Federal Disability Retirement and how it is a little bit different for military veterans. So we’ll go over what Disability Retirement is, the benefits and how much it pays out, and we’re also going to talk a little bit about how there can be additional benefits for veterans applying for Disability Retirement.

Okay, so let’s just jump into the Federal Disability Retirement benefit. Grant, can you give us just some information on who this benefit applies to?

Who Can It Help?

Grant Ostrander (Director of Operations, Chartered Federal Employee Benefits Consultant & Certified Federal Retirement Consultant): Absolutely. Federal Disability Retirement can help anybody who is a career federal employee who’s struggling with an illness or injury that’s keeping them from being fully successful at work. It can’t be something that’s short-term — it’s got to be something that’s considered permanent, and for this specific law, permanent means anything that’s going to persist longer than a year.

Ashley: Right, and this is something that has to have arisen while they’re in federal service, or worsened.

Grant: That’s right. The cause of the injury doesn’t have to be work-related at all. It could totally be just getting sick of something and having an illness, or it could be an injury you had from, you know, college athletics, or — I mean, obviously in the military.

But the actual disability can’t exist prior to employment in its current state. So it either has to have arisen while employed or worsened to the point that it’s causing a problem with your ability to perform your job while you were employed there.

Ashley: Exactly. And we’ll talk a little bit about where this benefit comes from.

Where Does It Come From?

Key Point: Federal Disability Retirement is already built into your retirement system — but you must apply for it and prove your case through OPM’s adjudication process. It isn’t automatic.

Ashley: So this is a benefit that is already built into the retirement system for federal employees. Specifically, there are just a few employees that are still under the Civil Service Retirement System, but for the most part this is for federal employees that are under the FERS [Federal Employees Retirement System] system.

This benefit is paid out through the OPM [Office of Personnel Management] — that’s the office that adjudicates this benefit. So while any federal employee that has 18 months of service with an injury is eligible, this is a benefit that you do have to apply for and be approved for.

Grant: Right, and not only do you have to apply for it, a lot of times federal agencies are really bad about informing their employees that it even exists — and half that’s because those HR offices aren’t even familiar with it. So it exists for all of them, but they do have to actually know about it and put together their applications.

And not only do you have to prove your case — with the burden being on the applicant — you have to actually understand what you’re applying for, because it’s not as easy as just sending in a piece of paper and getting a benefit. So you have to know whether or not it’s actually going to be good for you and be something that makes sense for you at this stage in your career. That’s one thing we always want to try to highlight for people: kind of what is the benefit that you get, and is it worth it for you?

The Monthly Annuity

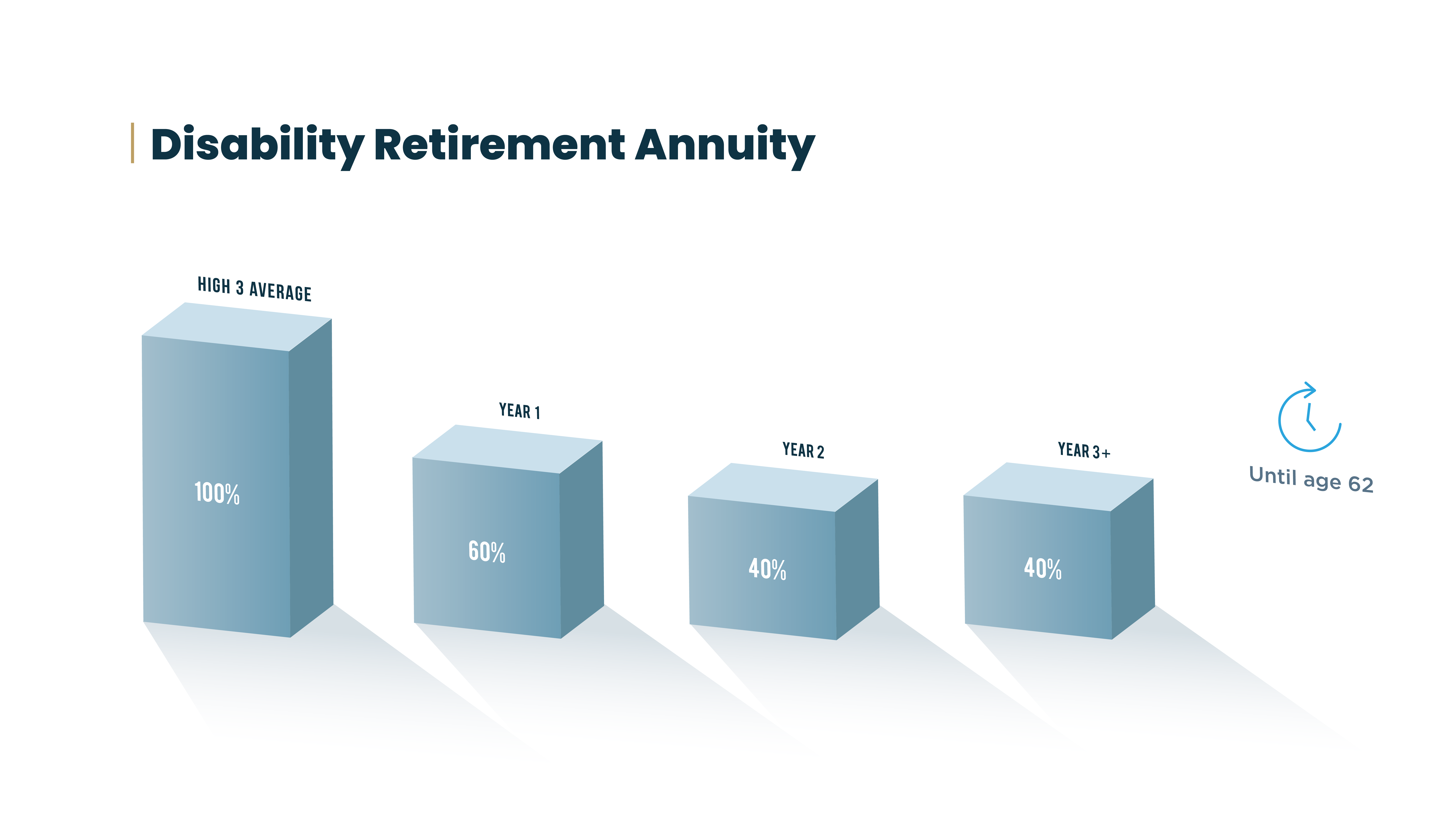

Ashley: Right. So let’s go through some highlights of this benefit. First off, we’re going to talk about the monthly annuity. So for Federal Disability Retirement, once an employee is approved for this benefit, the first year they will receive 60% of their high-three salary, and every year following that they will receive 40% of their high-three salary. And it is important to note that this benefit is subject to federal income tax.

Grant, can you give us a little bit of information on what the high-three average is, because this is not something that’s just their annual salary?

What Is the High-Three Average?

Key Point: Your high-three is the average of your highest 36 consecutive months of basic pay — not your current annual salary.

Grant: It — and this causes as much confusion as anything that’s involved with federal employee benefits — but it’s got a simple definition, and you have to kind of say it out loud to yourself a few times before it makes any sense. But the idea is that it’s the highest 36 consecutive months of your basic pay.

A lot of times people will say things like, “Well, what about overtime?” And really, that overtime is excluded from most employees unless it’s a part of your regular salary. And if you think to yourself, “Well, I don’t know if it is or not,” then it probably isn’t. If you’re in federal firefighting or law enforcement, there’s some things that are mandatory, and those are things we’re really referring to. So if you’re one of those employees — especially special provisions employees — you already know that that’s part of your salary. So if you’ve got a lot of questions about whether or not your overtime counts, likely it doesn’t.

Ashley: Right.

Grant: But the truth is, this all gets calculated by OPM and you can’t change it. The good news is, though, if you’ve been on workers’ compensation, they’re still counting your actual salary that you would have received — not your compensation rate — in that high-three. So if that’s part of the highest 36 consecutive month period, you’re not losing out on that.

That calculation will stay the same until your 62nd birthday, and on your 62nd birthday that benefit gets recalculated as if you had just continued working at your present position until that date.

Continuing to Accrue Years of Service

Ashley: Right. So another benefit of receiving Disability Retirement benefits is that you do continue to accrue years of service while on this benefit. So right here we have just a good visual representation of the benefits that you can receive — the first year being that 60% and every following year being 40%.

And this is such a big deal for employees who are unable to reach the retirement age: you will continue to accrue years of service on this benefit. And accruing federal years of service is such a big deal for employees who are unable to reach the age 62.

And another big benefit of Disability Retirement benefits is that you are able to continue working in the private sector while on this benefit. Grant, can you talk a little bit about the parameters of working in the private sector?

Working in the Private Sector

Grant: Sure. This is a really big deal. And I think that, you know, most of our clients and most people we talk to — they have a career with the federal government, and their plan was to continue to work in that career until they retired. So this unexpected illness or injury that’s impeding their ability to continue working is a big change, and so they haven’t thought about what they might do somewhere else.

But truly, most of our clients find an opportunity that maybe they always wanted to do — something or thought they’d be good at something but didn’t feel like they could earn the same kind of compensation. Or, certainly now that they’ve got an injury and illness, they don’t necessarily have the bandwidth or the ability to do it at a level that would provide an income for them that keeps them in a stable spot.

But with between 40% and 60% of their salary being paid through the retirement benefit — the Disability Retirement — there’s an opportunity to do something in the private sector that fits inside their medical restrictions, that perhaps they’ve always wanted to do or always had a talent for. And there’s the ability to earn up to 80% of your federal salary in a private-sector job.

So we see folks that are getting into real estate or getting into teaching, and there’s a lot of people that have special skill sets that are only taught by the government — especially law enforcement guys that get snapped up by consulting groups because they have a special skill set. So we see a lot of folks find good, sustainable employment that fits in their medical restrictions, and maybe they only work part-time, but they don’t need a full-time salary anymore because almost half of their compensation is being paid through that retirement benefit.

So it is a massive ability that this doesn’t end your earning ability — it just supplements it and helps you take the next step in your career, rather, on your way to a full retirement once you reach that age.

Ashley: Exactly. And just to be specific, federal employees are able to make up to 80% of what their former position is currently paying.

If you look on this next slide, here is a good representation of what you can earn while receiving Disability Retirement benefits as well as income from the private sector. And you’ll see that you are able to potentially make more than you were receiving just in your federal position.

Why Creditable Service Matters Long-Term

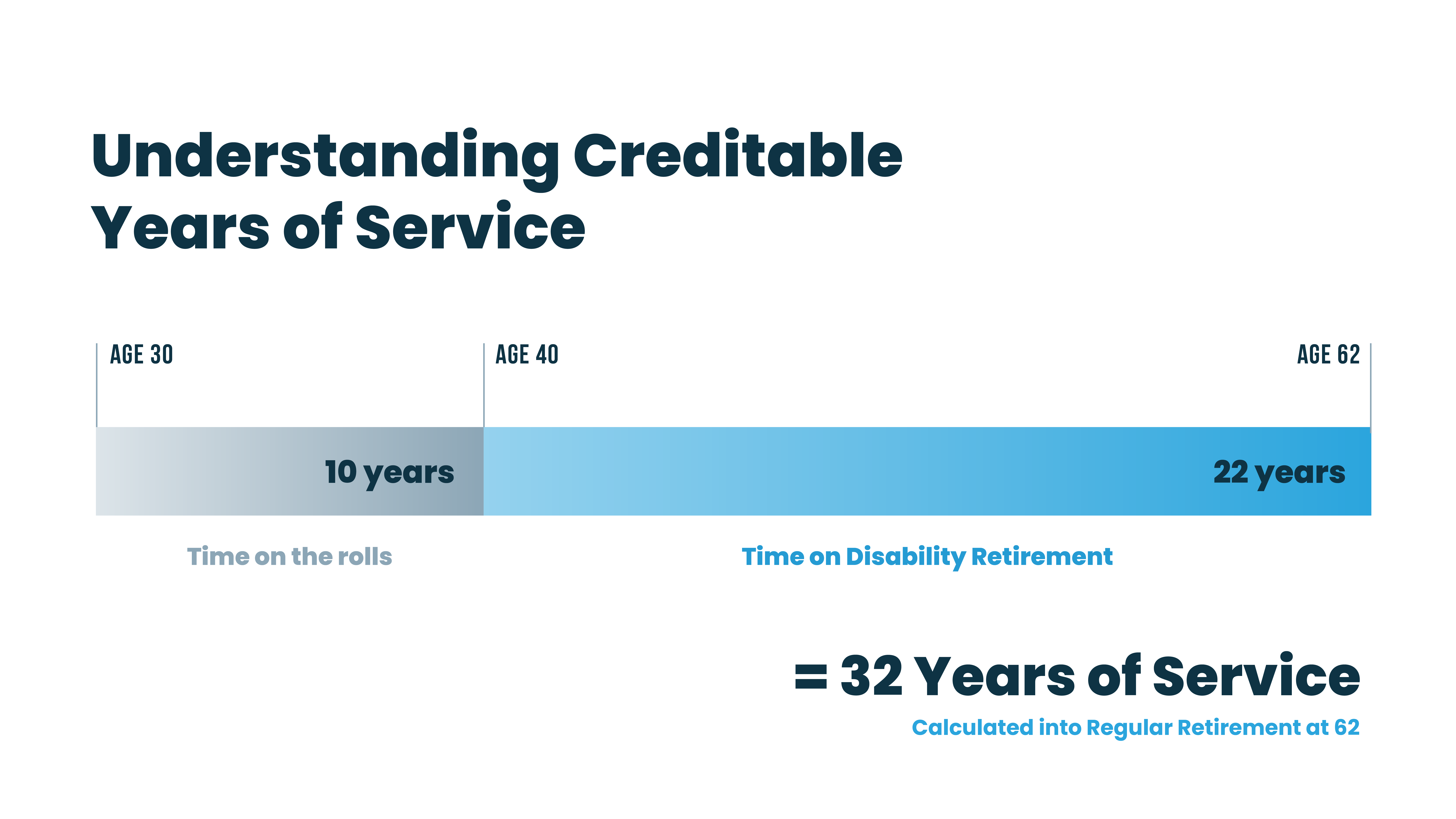

Grant: Yeah, and we touched on how important it is to continue to accrue creditable years of service, but this next slide really kind of talks about that and gives you a visualization. For some people, you’re in your mid-50s or even pressing into a minimum retirement age or late 50s, and you look at it and say, “Hey, this just gets me a couple more years and gets me the last push to age 62, when I would have reached my full retirement age.”

But for other people, they might be in their 20s or 30s or early 40s, and they’re a long way away. And so the idea of what my retirement might be after 10 years of service is pretty small. But if you look at this chart here, this little graph, you see that if you’re age 40 when you get on this, it’s going to add 22 years of creditable service, giving you a total career of 32 years. And that’s massive.

So I can’t stress enough how much that means to somebody in the long term, because once we hit our 60s and 70s and our earning ability starts to decline, the more stability we can have in that last bit of retirement — when we can’t go out and earn at a job as easily as we could when we were younger — that stability means a whole lot. So raising the long-term is sometimes even more important than those years between 40 and 62. So I think that that’s something that needs to be kind of understood by everyone, just so that they know what they’re looking at.

Ashley: Right. And the difference here is receiving 1% on your regular retirement versus that 1.1% for having over 20 years of service, which can make a big difference.

Grant: Right, and you only get that if you’re 62. And this benefit does that for you — it takes you to 62 to get that 1.1. You have to have over the 20 years, and you have to be 62 when it gets calculated, and this benefit does that. If you’ve hit 20 years by the time your 62nd birthday rolls around, this benefit gives you that bonus.

Qualifications: Total vs. Occupational Disability

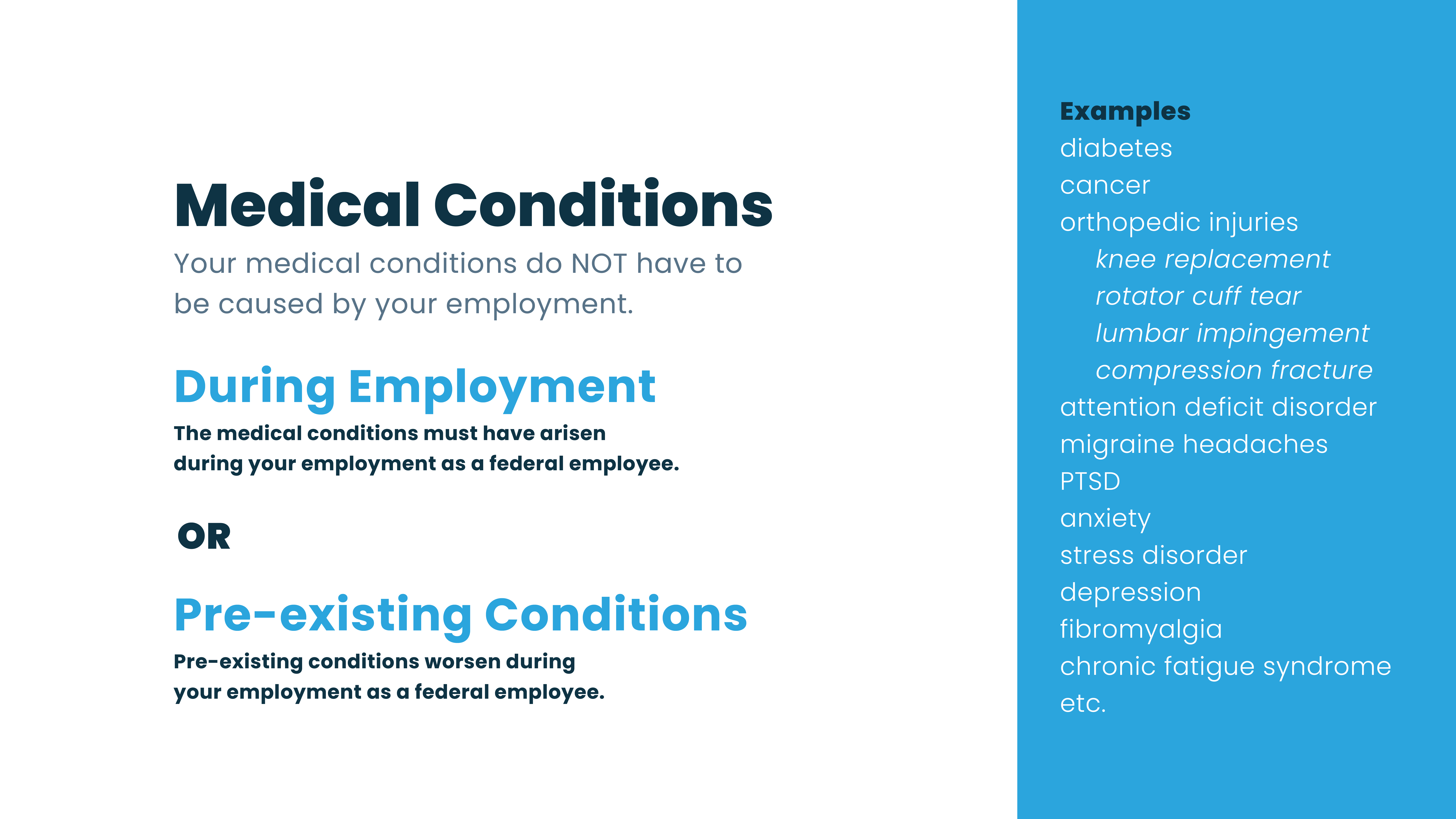

Ashley: So let’s jump into the different qualifications for Disability Retirement. Specifically, employees need to have a medical condition, as we stated earlier, that has either arisen in federal service or worsened. Specifically, it needs to be a medical condition that inhibits an employee from continuing to complete at least one of the major functions of their current position.

So while you don’t need to be completely, totally disabled from working, you just need to be unable to complete one of the tasks or functions of the position that you’re currently holding. Grant, can you talk a little bit about the difference between total and occupational disability?

Key Point: Federal Disability Retirement uses an occupational disability standard — can you do your specific job? — which is very different from Social Security’s total disability standard of being unable to do any job at all.

Grant: Absolutely. Total and occupational disability are simple concepts, but it’s not common language. So a lot of people, when they’re considering a disability, they just equate federal disability and Social Security disability, and those two things are really, really different.

Social Security disability is available to anyone who’s paid into the Social Security system enough and becomes totally disabled, and their criteria is a high standard. They require you to show that you’re not capable of what they call gainful employment activity, and that’s a really high threshold. So you have to show that you’re basically incapable of any real job at all.

Whereas with Federal Disability Retirement, here is what’s called an occupational disability. And this is important because it specifically relates to each person’s individual job. Because that definition up there you read said it: a failure to be able to complete at least one of the major functions of the current position. All we’re saying is, do you have a medical condition that prevents you from doing that specific job — not any job, not some other job, but that job?

It then becomes incumbent on your agency to be able to show that they have another job that’s equivalent that you can do or can transfer to. And if they don’t have that — which most agencies don’t — then the disability can be granted.

So when we talk about occupational versus total, you may be totally disabled, which is a much higher burden and should qualify you for the federal disability. But you may also only have a disability that affects your job, not any job.

And let me give you a perfect example: law enforcement agents that carry a firearm have a very high standard for being able to qualify with that firearm. So if they have a medical condition that requires them to take any medication that’s a narcotic or an antidepressant, they’re automatically disqualified from carrying their firearm, which then makes them automatically disqualified from their position as a law enforcement agent.

So you can see there, that person might physically be able to do all kinds of things — and that includes shoot, you know, playing pickup basketball with friends — but if they are suffering from a depression condition and the doctor puts them on an antidepressant, that can disqualify them immediately and put them into an occupationally disabled status, which would make them eligible for this benefit.

Medical Conditions Do Not Have to Be Job-Caused

Ashley: Exactly. And just to reiterate, this medical condition does not need to have been caused by your current employment. It just needs to have arisen, or — if you do have that pre-existing condition, like if you are a veteran — just something that’s worsened during your time as a federal employee.

Grant: Yeah, and worsened to the point where it actually causes that inability to do your job.

Ashley: Right, any kind of service deficiency. I mean, you’ll see here on the right of this slide just some common examples that we see here at our firm of medical conditions that can cause those service deficiencies.

How It’s Different for Military Veterans

Ashley: We’re going to touch on some different benefits that veterans may be eligible for. So in regard to Federal Disability Retirement, we’re going to talk about military buyback, military retired pay, as well as VA disability pay.

So we’ll jump in right now to talk about military veterans specifically and how this benefit can look a little bit different. Like we mentioned, veterans that were injured during active duty have conditions that may have worsened over time. So a veteran could be receiving a 100% VA disability rating while they’re employed by the federal government. However, when they have an injury that’s worsened over time that now causes them a service deficiency that makes them unable to work in their federal position, they are now eligible for Federal Disability Retirement.

Grant: Right. And this is important because I think a lot of veterans — especially a lot of federal employee veterans that we talked to — maybe did their four years in an enlistment and reached an E-4 and had a good service career, then they rolled out on a voluntary discharge. They become federal employees under a preference point system. They take a job with the federal government — maybe they have a skill set they learned in the military and they’re in law enforcement, or maybe they work for the postal service or wherever.

And those four years they spent in the military kind of get lost, because it’s not enough to have reached a full retirement and it’s kind of a small amount. But it’s important for them to understand that they can buy those years into their FERS retirement, and it’s not as expensive as you might think. You only have to pay the deposit amount that you would have paid into FERS had that service time been under the government system.

So for a lot of folks in that situation I just described — where they got three or four years in the military — it’s a pretty small amount, especially when you consider that it’s going to add a year of service for every year you spent in the military.

And that’s going to equate to 1% of your high-three for the rest of your life from 62 on.

So you might find a situation where it costs $1,500 to buy your service back, and that is going to equate to $1,500 a year for a 25-year period of your life. So by most standards, that’s a pretty good investment to get a 25-times return on your money. So when we get to military buyback, that’s one thing I think that we offer to people: the ability to help them understand when it’s good and when it’s not a good idea to buy their buyback.

And while we’re never going to buy somebody’s time for them — that’s not our role — it is important that it’s considered by any veteran whether or not it’s a good decision. So that’s something that we always want to stress: like, hey, have you bought it back? And if you’re going to buy it back, you have to do it before your retirement is finalized. If it gets finalized, you can’t do it anymore.

Ashley: Exactly. And this must be paid back, like Grant said, paid back in full prior to separation — so not necessarily by the time you apply for Disability Retirement, but by the time you’re approved or separated from the federal government.

Military Retired Pay

Ashley: Okay, so we’ll talk a little bit about military retired pay. This can be really important for federal employees because there’s no offset with Federal Disability Retirement. So you are able to receive your military retired pay as well as the Federal Disability Retirement benefits. You’re not able to buy back that time if you’re already receiving military retired pay; however, you do have the option to waive that if you’d rather buy back that military time.

Grant: This is one of those math equations that we try to walk through with people when we can. But the important thing to note here is that everybody’s situation is different, and a lot of this depends on what their rank was and how many years of service they had in the active duty, and then also what their job is now and what their earnings are in the federal sector.

So really, this comes down to which benefit is better for you and which version of this is better for you. And that’s something we’re happy to walk through and kind of explain to people on an individual basis, but it’s not something you can explain in a webinar, because if you have 100 people, you have a hundred different scenarios. So the last thing we want to do is tell anybody, “Oh, you should or shouldn’t do this,” because it’s going to depend on your situation.

Ashley: Exactly. And every veteran’s situation can be so different. And another thing that veterans want to consider is if they’re eligible or receiving VA disability pay.

VA Disability Pay

Key Point: VA disability pay does not offset with Federal Disability Retirement. You can receive both concurrently, with no reduction to either.

Grant: Yeah, that’s a huge one. I would say a large number of our clients that are disabled have a VA disability claim. And whether it’s a small disability percentage or 100% disabled from the VA, it does provide a tax-free payment to a veteran who sustained some kind of long-lasting injury or illness as a result of, or during, their time in the military.

The good news is there’s no offset. So if you’re currently receiving a VA disability payment, that doesn’t change anything. Nothing happens with the Disability Retirement or with your VA payments, so you can continue to receive those concurrently without having any kind of offset.

Ashley: Exactly. So this is another way you can just maximize these annuity payments. A lot of veterans may be eligible for different military benefits as well as the ability to apply for Federal Disability Retirement.

Grant: I think the fact that those things can be based off of the same injury is important. And we talked about that earlier already, I know, but I just want to re-emphasize how important it is to understand that it could be the same knee that you’ve got a VA disability claim for that later worsens during your federal career and can be the reason that you get a Disability Retirement.

Example Federal Employee: Meet John

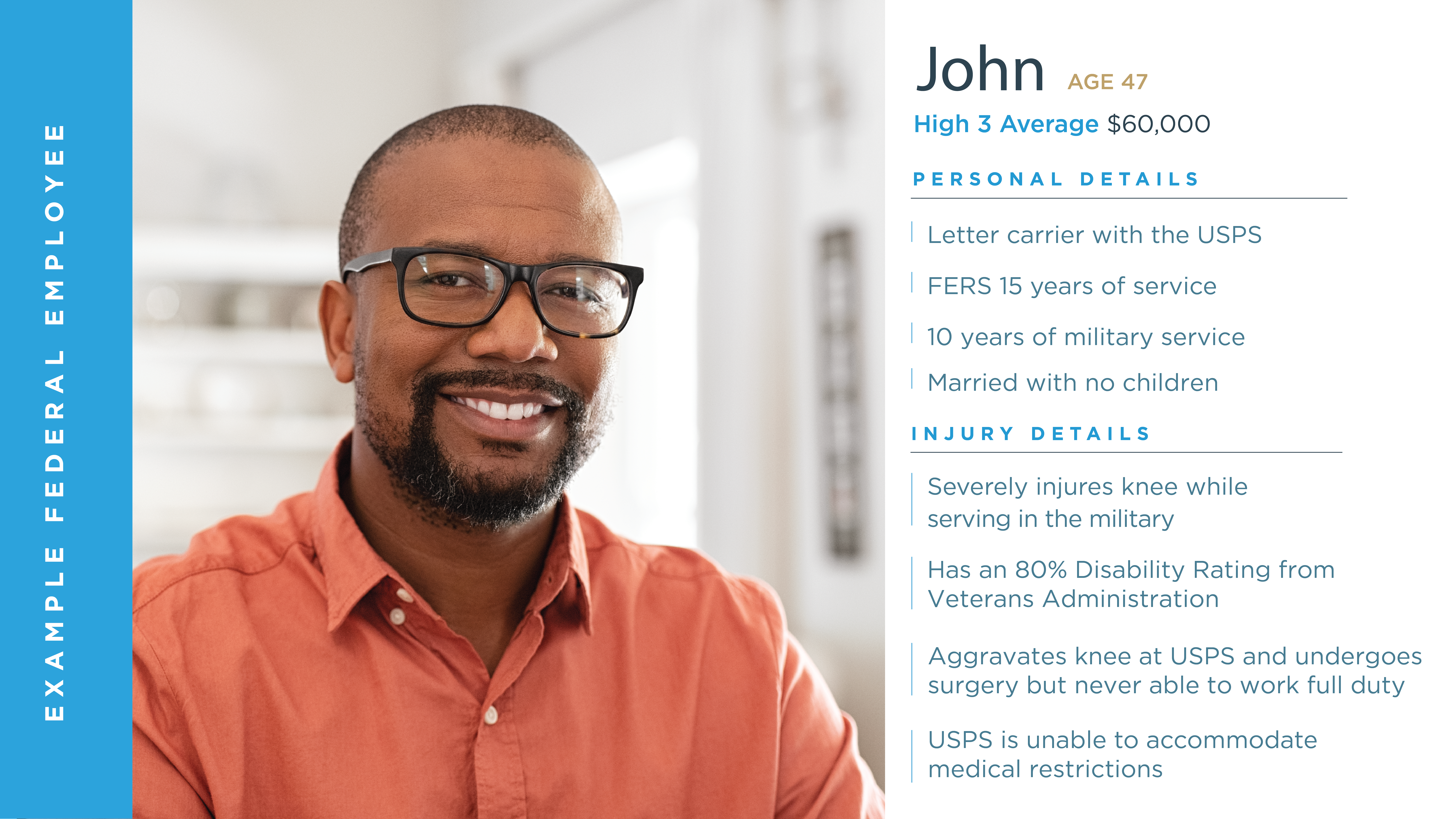

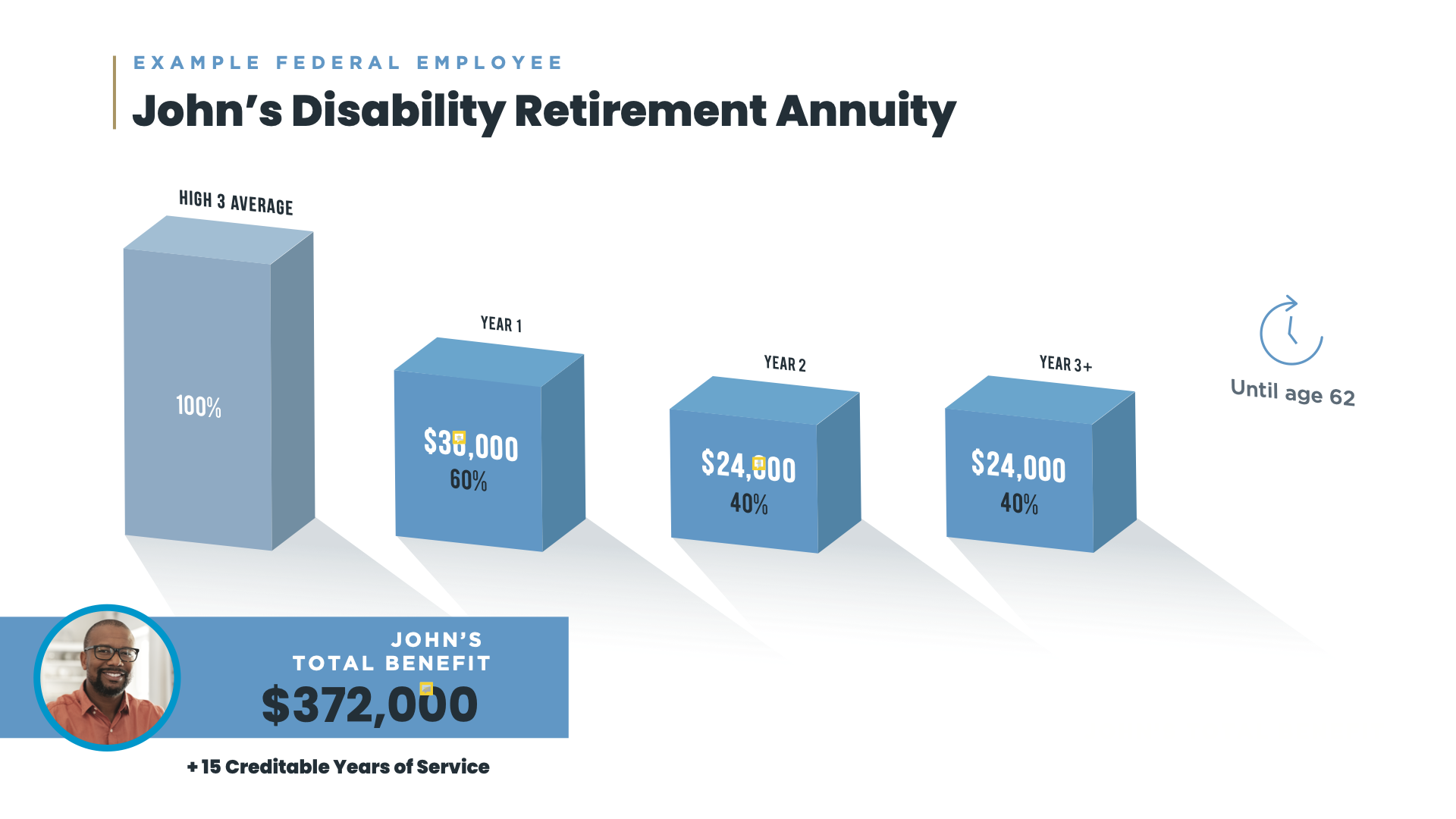

Ashley: So now we want to go over an example federal employee so we can go over a breakdown of his benefits. So this is John. He’s 47 years old. His high-three average salary is $60,000. He’s a letter carrier with the U.S. Postal Service and he’s worked there for 15 years. John also has 10 years of military service and he is married with no children.

So specifically for John, he injured his knee while serving in the military and he has received an 80% disability rating from the Veterans Administration. His injury worsened while in federal service, and he underwent a surgery, but he was never able to return to full duty, and the post office is unable to accommodate his medical restrictions. Grant, can you go over that monetary breakdown for John?

Grant: Sure thing. And obviously, all names and information have been changed to protect the innocent here. But, you know, I’ve probably spoken to a few hundred people where this is almost their exact situation. I mean, in 17 years of doing this, I’ve spoken with thousands of people, but this one is so common. And there are tons of other examples that are a little different here and there, but this is a really, really typical type of call that we get.

And as we go to this next slide, what we’re going to start to see is how these graphs play out in this type of a situation. So in John’s situation, his high-three average is $60,000, as we said — that’s that first block there, it’s the biggest, 100% of his pay is $60,000. That first year on disability, he’d qualify for 60% of that number, which is $36,000. After the first year, it drops to the 40%, and that’s $24,000, and he would receive that all the way to his 62nd birthday.

The total benefit from John’s Disability Retirement annuity in that 15 years is $372,000, in addition to the extra 15 years of creditable service.

Ashley: Right.

Grant: Okay, so that’s the core benefit itself, what it would actually pay. Keep in mind, you could just stay on your health and life insurance if you want to through the federal government, so those are other benefits that come along with it, but this is the raw payment.

Ashley: Exactly.

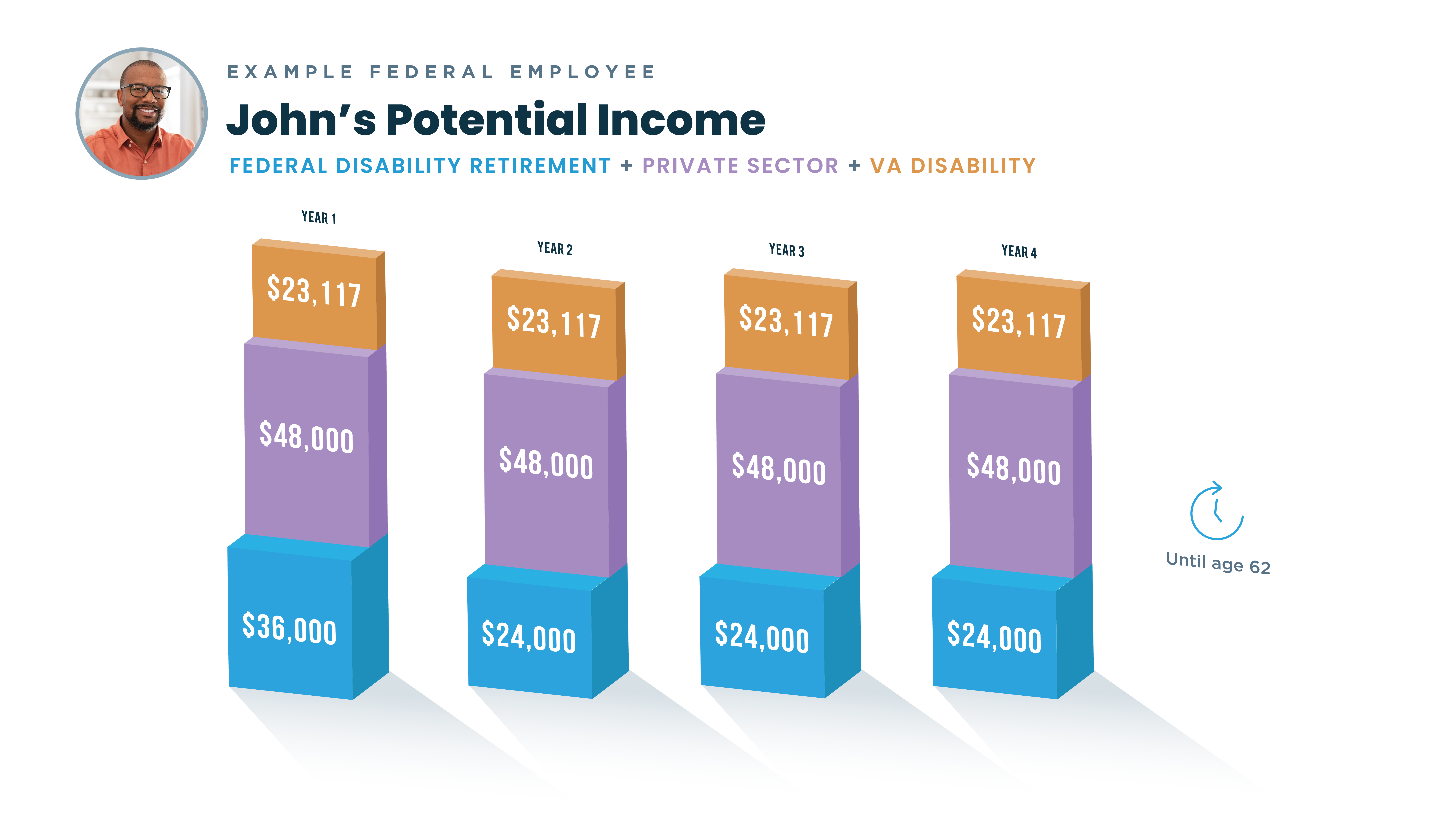

Grant: Now, if you add in his earning capacity in the private sector and go to this next slide, what you see is he still has his original $60,000 basic pay, or high-three. And then after that you see that same 60% block — that’s $36,000 — on the bottom in blue, and then above it in purple is the 80% of his job’s pay that he can earn in a private-sector position. And 80% of his pay is $48,000.

So during that first year, his total would be $84,000 potential, which is obviously 40% over his actual high-three number. And then after that first year, when it drops to 40% on the annuity plus the 80% earning capacity, that’s $72,000, which is 20% over his high-three earnings. And his potential private-sector income during that 15-year period is $720,000.

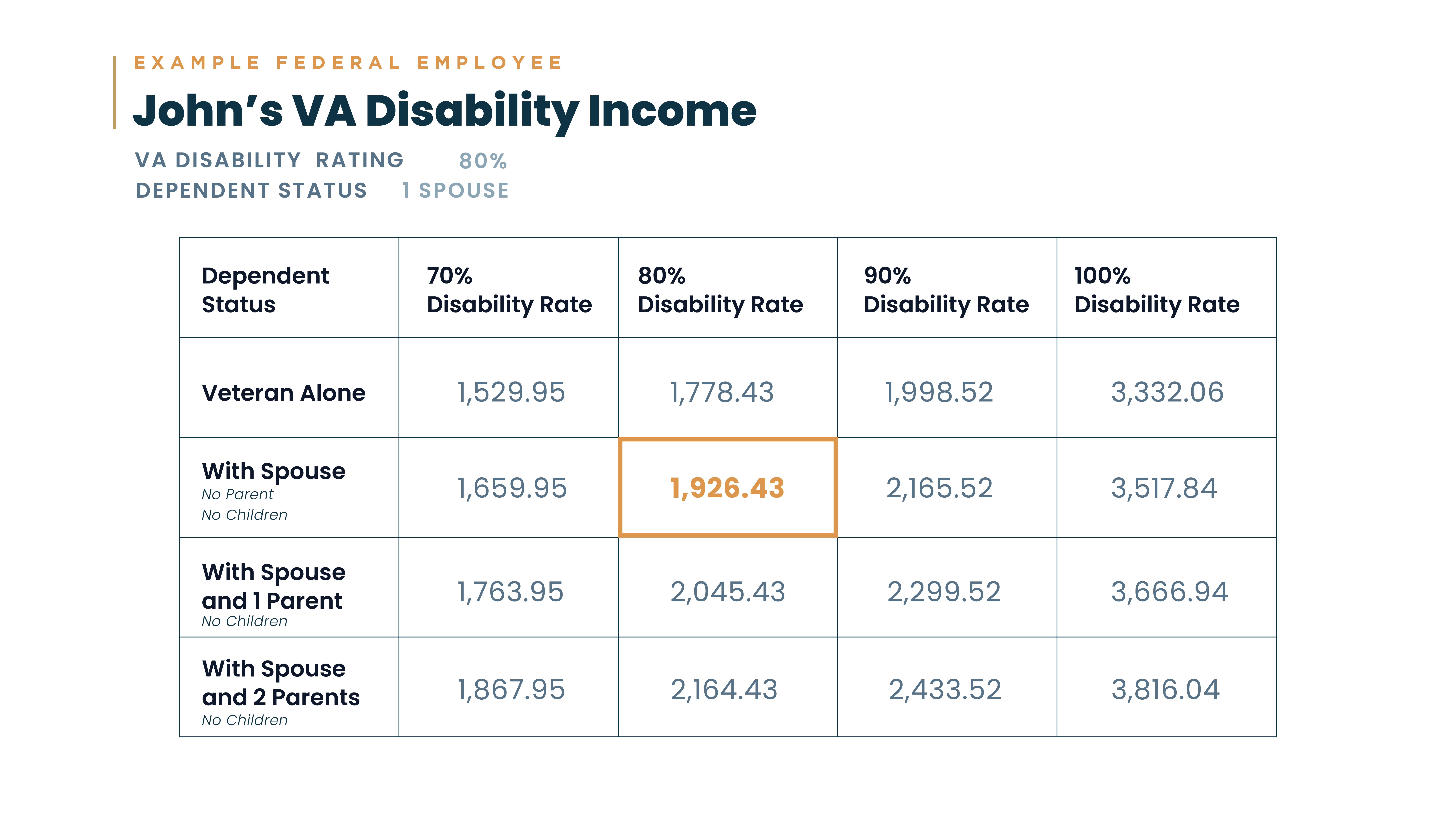

So the last bit of information that we’ve got for John is actually his VA disability income. And so when we look at this next chart, this is a standardized VA disability chart for an 80% disability rating. He doesn’t have any dependents — he is married — so his monthly payment for his VA disability rating is $1,926.43.

And because we’d like to be particular down to the decimal here, we’ve got some interesting numbers that start jumping in for us. So here’s the chart again when we’ve added the final benefit piece here: the VA disability payments, which for him are $23,117 a year, and that stays the same every year.

Ashley: That one’s constant.

Grant: Yeah, that doesn’t change. It doesn’t go down, doesn’t go up. It’s just what he has now. If his disability rating from the VA were to increase, we’d go back after that chart and watch it climb up as the 90% or the 100% disability rating came in. So that could change, but without him taking further action to increase that disability rating, it’s going to stay constant.

John’s Total: How the Benefits Stack

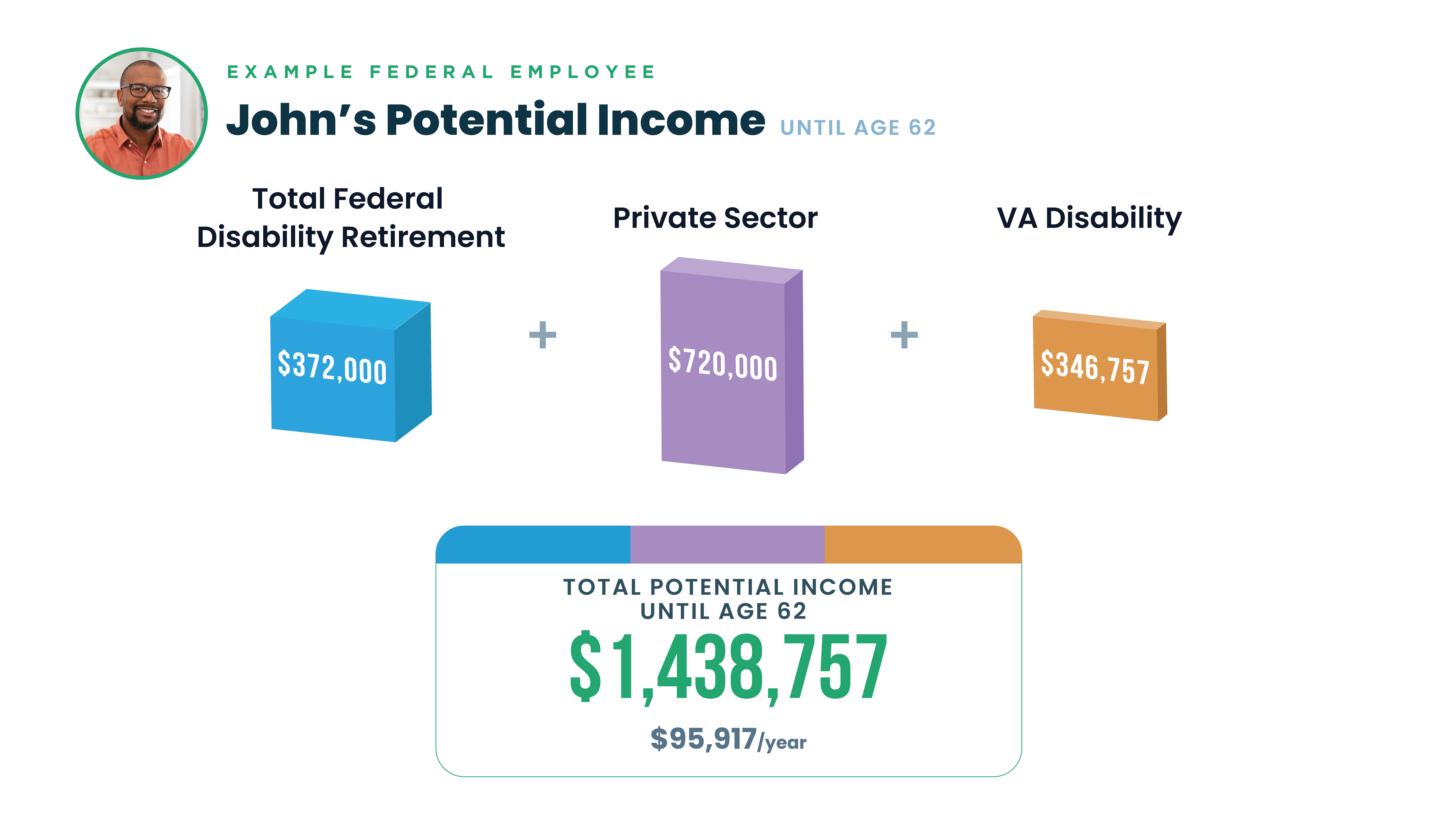

Grant: And we just add that to his federal Disability Retirement annuity, his earnings capacity, and then put that VA bit on top there. And what you see over this 15-year period between his age 47 and age 62, when he hits his full retirement age, is that the Disability Retirement benefit will pay him $372,000, he could earn up to $720,000 in a private-sector job, and his VA disability rating will pay him $346,757 — bringing us to this grand total of $1,438,757, which comes out to just under $96,000 a year. That would be the total kind of package potential up until his 62nd birthday.

One other thing to note here is that because he’s adding those additional 15 years of service onto his existing service record, that would give him a 30-year civilian career. If he chose to buy his military time, that would put him at 40 years total on his creditable service, which means on his 62nd birthday he would be entitled to the full retirement of a 40-year career — which for him would actually go up. He’d get the bonus 10%, and he would have a 44% annuity for the rest of his life, in addition to his VA payments.

Ashley: Wow. Thank you, Grant. I think it’s really important to see the way that benefit plays out, and the way that those different benefits can just be added on to one another, to see how much security that can provide a federal employee who’s unable to make it to that age 62.

Wrapping Up: Key Points

Ashley: So just as we wrap up — this is a lot of information that we’ve gone over. But just to touch on some key points that we talked about: the Federal Disability Retirement benefit does provide a monthly income after approval, and it does go up to age 62, when you would flip over into your regular retirement. You also earn creditable years of service while in Disability Retirement, and you’re able to work in the private sector and earn up to that 80% of what your previous federal position is currently paying. And these veteran benefits can work with Disability Retirement to maximize that income, in the short term and in the long term, through regular retirement.

Grant: I just want to re-emphasize that this stuff is complex, and if you’re not used to dealing with it, it can seem overwhelming. But don’t be intimidated.

If you want someone to walk through this with you, just give us a call today for a free consultation.