Quick Takeaways

- You can maintain your current health insurance: Once approved for Federal Disability Retirement, you can continue your FEHB coverage. You’ll keep paying your portion of your premiums and the OPM will take on the percentage that your agency used to cover.

- Life insurance options remain available: You can continue your FEGLI coverage into disability retirement if you’ve been enrolled for five years, though premiums increase significantly after age 62.

- Survivor annuity affects health insurance continuation: Your spouse can only continue FEHB coverage after your death if you elect at least a partial survivor annuity (5% or 10% reduction in your monthly payment).

- Working while on Disability Retirement is allowed: You can work in the private sector earn up to 80% of your old position’s current salary while receiving your Disability Retirement annuity, creating significant income potential.

- Health insurance reinstates retroactively if terminated: If your benefits were terminated after separation, they can be reinstated retroactively once you’re approved, with premiums deducted from back pay.

Common Questions

Q: Can my spouse and dependents stay on my health insurance during Federal Disability Retirement?

A: Yes, they can continue coverage just as they currently have. However, if you don’t elect at least a partial survivor annuity, your spouse cannot continue FEHB coverage after your death.

Q: What happens to my health insurance premiums on Federal Disability Retirement?

A: You’ll pay your portion of the premium, and the government continues to pay their portion. Premiums are deducted from your annuity payment instead of your paycheck.

Q: Can I keep my FEGLI life insurance on Disability Retirement?

A: Yes, if you’ve been enrolled in FEGLI for five full years. You can maintain your Basic coverage and Options A, B, and C, though premiums increase significantly after age 62.

Q: What’s the difference between maximum and partial survivor annuity?

A: Maximum survivor annuity (10% reduction) pays your spouse 50% of your unreduced retirement. Partial survivor annuity (5% reduction) pays 25%. Without either election, your spouse loses health insurance continuation rights after your death.

Q: What happens to my insurance at age 62?

A: Your disability retirement converts to regular retirement with recalculated benefits. Health insurance continues, but FEGLI premiums increase substantially, making it worth exploring private insurance options before this age.

Full Webinar Transcript

Federal Disability Retirement Basics

Nick Child (Director of Client Acquisition): Hey everyone, welcome into today’s webinar. My name is Nick Child and I’m the Director of Client Acquisition here at Harris Federal Law Firm. I’m really excited to have everybody here today as we’re going to talk about some good stuff for federal employees to know that are interested in Federal Disability Retirement.

I have Grant Ostrander here with me today. He is our Director of Operations here. He’s also a Chartered Federal Employee Benefits Consultant and is also a Certified Federal Retirement Consultant. In addition to those, he has his life insurance license, so he really is the perfect person to be talking to you about this today. Grant’s been with Harris Federal since the beginning for over 17 years now. He’s been helping people walk through all of this and really guiding them towards the best possible future that they can find out of the tough circumstances that they find themselves in. So Grant, excited to have you here and for you to get to talk to everybody today.

Grant Ostrander (Director of Operations): Yeah Nick, thanks for having me. It’s a blessing to get to get on here and talk with some folks about what their options are heading into Disability Retirement.

Nick Child:So, what we’re going to cover today—we’re going to talk about the basics of Federal Disability Retirement. We’re not going to get into the weeds with it today. We’re not going to go into too much detail because hopefully you’ve already heard of that benefit before and all the benefits it offers you. But we’re going to cover those real quickly just so that we know that everybody has a baseline understanding of what we’re talking about. That’s including how much it pays, the other highlights, and then we’re going to specifically get into the insurance options—the health and life insurance options that federal employees have with Federal Disability Retirement. And then talking a little bit about survivor annuity options and then what happens once I turn 62 and get on my regular retirement.

Who Federal Disability Retirement Can Help

Nick: So first let’s get into the basics of Federal Disability Retirement so that we can make sure that everybody’s on the same page here and we know what we’re talking about. So let’s talk first about who it can help.

Grant: This is a benefit that really applies to federal employees who have some kind of medical condition that is preventing them from completing at least one of the essential functions of their job. Medical condition could be an illness or it could be an injury. It doesn’t have to be an on-the-job injury. It just has to be some kind of diagnosis that’s preventing them from being fully successful in all the areas of their job.

Nick: Yeah, so if you’re having a tough time doing your job because of injury or illness, this is something that you need to be looking at. And like Grant said, this can be caused on the job but it doesn’t have to be. So that’s something that you need to be thinking about and know.

So this is a benefit that comes from your FERS retirement package, right. So this is built into it. It’s there for every full-time federal employee. CSRS employees are eligible for this benefit too. It’s built into your package, but it looks slightly different with that calculation there for them and you need to be aware of that. We’re not going to get into the details of that here because most of our audience is going to be under FERS.

And then this is a benefit that is handled by the Office of Personnel Management [OPM].

Federal Disability Retirement Highlights

Nick: So to get into the highlights of this benefit real quick and just talk about what that looks like for somebody that needs to utilize this benefit—the first thing we’re going to look at is the monthly annuity, stand to earn some monthly income, the ability to work in the private sector, creditable years of service, so continuing to earn those while you’re on this benefit, and then what we’re all here for today, which is the health and life insurance—really knowing what all the options are there. And we’ll get into that just a little bit later.

How Much Federal Disability Retirement Pays

Nick: But first let’s talk about how much it pays.

Grant: Right, this is the number one question for everyone whenever we’re thinking about something like this. We’ve got to know what could I expect to receive from a benefit like this.

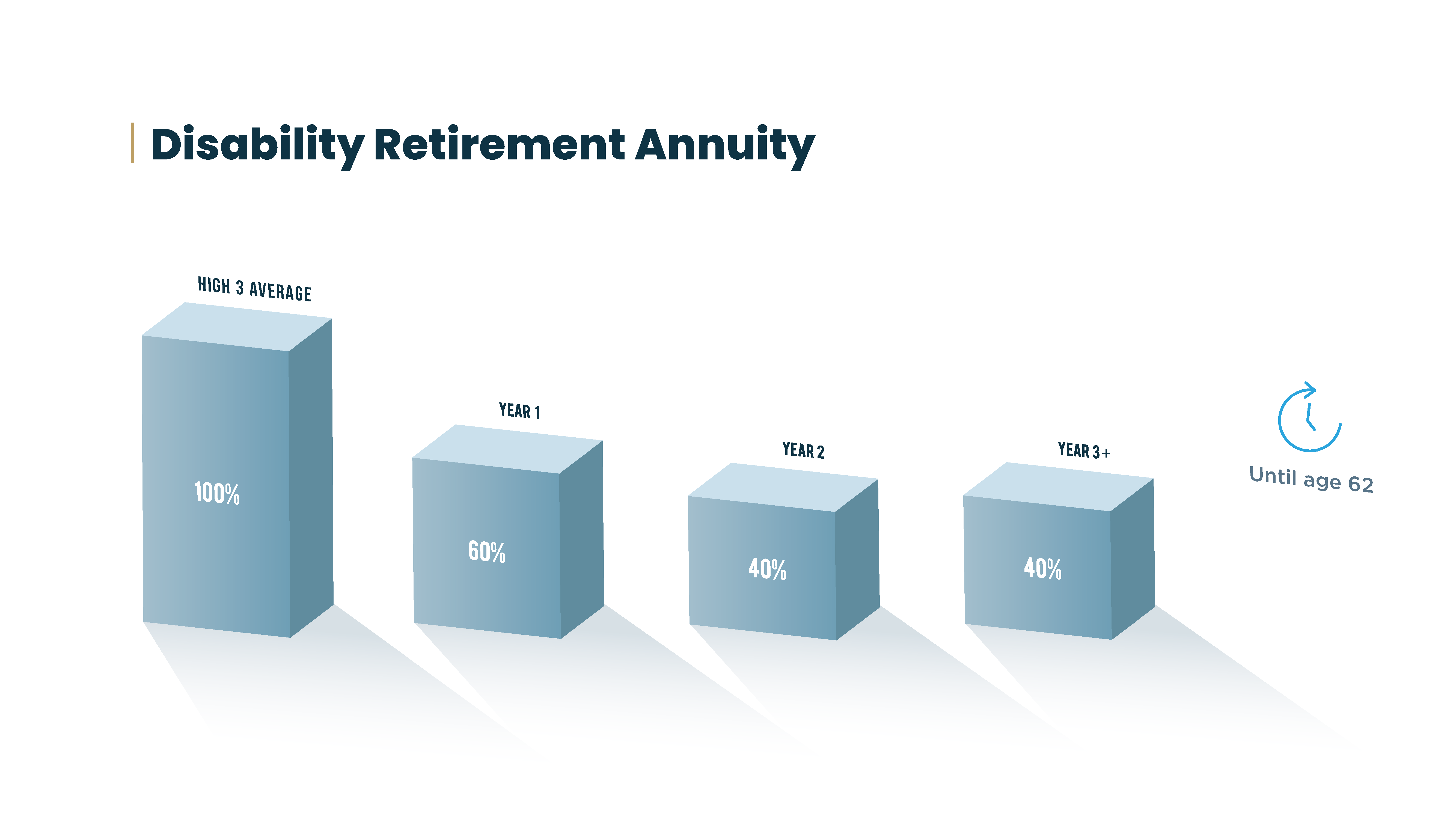

And so it’s got a fairly simple calculation. The first year you would receive 60% of your high three, and then every year after that until you turn 62 you would receive 40% of your high three.

And high three is an important number and it can be confusing for people, but let’s talk about that for just a second. The average of your highest 36 consecutive month period of your basic pay is how they get a high three. And this begs a lot of questions—well, what about my overtime or what if I have LEAP pay or there’s all these different kind of caveats and exceptions. But it’s important to remember that if these things are mandatory, they’re calculated as part of your basic pay. And if they’re not mandatory, they’re generally not. And you know whether or not you have these things mandatory in your pay. But the best news of all is that the OPM will calculate it for you. You don’t have to do a lot of math.

Nick: Exactly. And this is something that you can find on your SF-50, so it makes it a little bit easier for you. And we know this is a unique number to kind of base this off of, but it’s how OPM calculates it.

So let’s look at a graph real quick here just so that we can kind of visually see what this is going to look like. So over here on your left you’re going to see that bar that says 100% and that represents your high three average. So the first year that you could be on this benefit, you would receive 60% of that high three average. Okay? And then every year after that first year until the age of 62, you’re going to receive 40% of that high three average.

So we wanted to put this graph here just so that you could get a good visual of what that income is going to look like. So like I mentioned here, that’s gonna last until you’re 62 years old. And so what we typically call this is a bridge to 62. This is not meant to be a total replacement of your income. It’s meant to supplement your income that you’ve lost from not being able to work. So in our office this is what we call it—a bridge to 62. It’s to get you from today until you’re 62 years of age.

Grant: That’s right. And the reason we have that number in there—we didn’t choose it. Everything inside of the FERS retirement system is built to get you to that 62nd birthday as a full retirement age. That’s when you’re eligible to start receiving Social Security unreduced, and there’s little structures that are built in to incentivize you to get to that age. So the disability retirement works the same way and we talk about a bridge to 62. If we imagine a career being a road towards a retirement at some day, if a medical condition were to interrupt that path, this Disability Retirement benefit would bridge you to your full retirement age. And that’s what happens with this benefit—on your 62nd birthday it recalculates as if you had just kept right on working to your 62nd birthday and then retired.

Working in the Private Sector

Nick: Yeah, so we’ll talk a little bit more about that here in just a second with creditable years of service. That’ll hopefully help that make more sense to you. But before we get there, let’s look at working in the private sector real quick. This is extremely unique to this benefit. You’re not going to find another disability benefit out there that’s going to allow you to work and continue to work while you’re receiving it. So this is something that a lot of our clients take advantage of—the ability to go and work in the private sector and continue to receive income. Right, Grant. I mean this is something that really allows people to kind of start their second career in some ways.

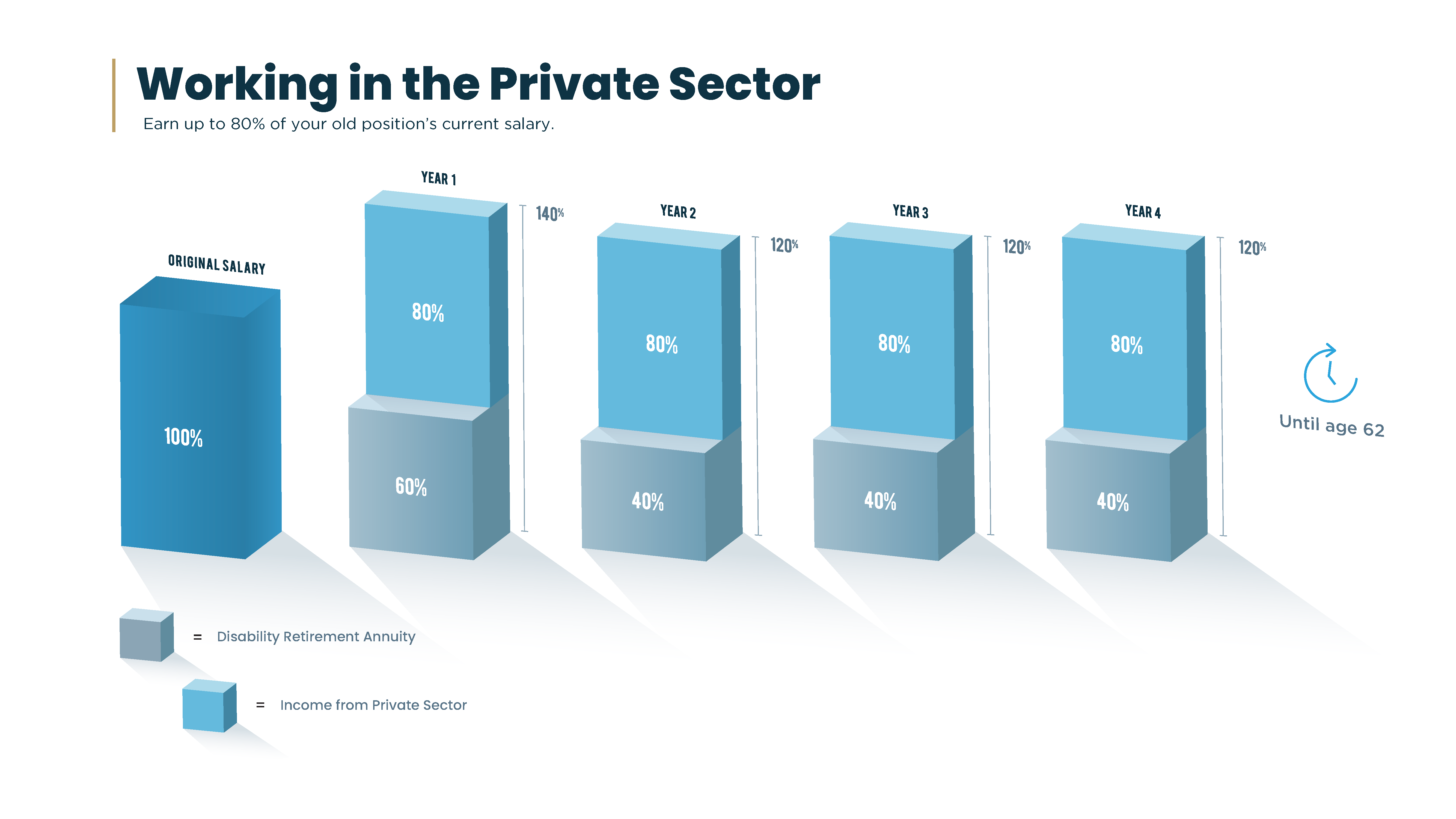

Grant: That’s right. And everyone’s situation is different. Some people have a permanent disability that’s not going to allow that to take place. But in these situations where someone is occupationally disabled from the federal government position, they could find something in the private sector that was within their medical restrictions. They’re allowed to earn up to 80% of what they’d be making if they still worked for the government in addition to receiving that 60 or 40% annuity. That’s a game changer as far as providing stability in the face of a serious medical condition.

So we think that this is not talked about enough and that people don’t understand it well enough. We’re happy to walk through it with anybody who calls and wants to chat with us about it. But it’s such an important part, and we want to reiterate this benefit—this Federal Disability Retirement benefit—is not designed to completely take care of you by itself. It’s designed to supplement you into the next stage of your life and, like you said, the second career or second half of your career.

Nick: Yeah, it really gives you a good safety net to take that next step.

Grant: Absolutely, and give you some security in the future.

Nick: And just to make sure everybody’s clear here, this 80% cap is on your old position’s current salary. So this is something that’s going to increase as you move into the future with salary increases and cost of living adjustments that are added to your old position. That number is based off of that.

So let’s look at a graph real quick here. This is that graph that we looked at before, but now we’re adding that 80% potential income on top of that. So if you look at year one there, we see that 60% that we looked at before. That’s our Federal Disability Retirement annuity that’s going to be 60% of your high three average. Now that 80% there is of your old position’s current salary, right? So we’re adding that on top of that 60%. So what we’re looking at there in that first year is a potential income of 140% of basically what you’re currently making, right?

And then from year two all the way until the age of 62, you have the potential to add that 80% on to the 40% annuity that you would be earning and a potential income of 120% of what you’re currently making.

So there’s a lot of numbers here that this can be confusing with all of the increases in your old position salary and all that kind of stuff. But what you need to know is that you have a pretty significant income potential that you might not be aware of today. So lots of our clients take advantage of this and utilize it to help them in the future.

Grant: Right. And one thing that I always want to emphasize here is there’s no guarantee you make that 80% in the private sector. But that 60 and 40—those are part of the benefit and you get them every year. And while you may not find a job in the private sector, or you may have a medical condition that prevents that type of work to where you could earn that additional amount of money—

Nick: Yeah, right Grant. Like maybe they have a hobby that they love that they’ve always wanted to do, and so now they can do it because they have a little bit of income to facilitate that.

Grant: That first almost half of your income is paid by the benefit, and therefore the amount that you need to make to make ends meet and have a successful career is lower. That burden is lowered. And so some folks really find some freedom in that second career to do what they’ve always wanted to do, what they’ve always loved to do, without having the pressure of earning quite as much as they had previously.

Nick: So yeah, so hopefully you can see there that that can really bring you a significant amount of income as you move into the future. And like we said, we know that not everybody can go work, right? There’s going to be some people that cannot work in the private sector, and there are some additional options like Social Security Disability out there for you. But we wanted to make sure that everybody’s aware of this because you just need to see how big that can be.

Creditable Years of Service

Nick: Another really big part of Federal Disability Retirement is what’s called creditable years of service. And if you haven’t heard about this before, this can be one that really pays huge dividends when you get to that age of 62.

Grant: I think one thing that gets overlooked about creditable years of service and the addition to your existing service record is that at age 62 when this bridge gets you to your full retirement age, if you had to stop mid-career you wouldn’t have built a big enough retirement to sustain you on into the future. But by adding these additional years of service that you’re not working onto your existing service record, when you hit age 62, you’ll have kind of the maximum amount you would have been able to get by then anyway. And that changes how you can look at the long-term effects of a retirement—whether or not you’ll be able to actually have a financial future that’s stable and secure. And of course, at age 62 you’re eligible to start receiving Social Security benefits, so the combination of adding the existing service record and the additional creditable years spent on the disability retirement to a Social Security payment can provide that kind of really solid retirement that everyone wants at age 62.

Nick: Yeah, and I’m a very visual person, so I need to really look at this and see it laid out in front of me. So hopefully this slide will help you understand this a little bit more.

So what we’re looking at here when we’re talking about creditable years of service is let’s imagine that somebody was hired into their federal position at the age of 30. They worked in their federal position for 10 years—that’s what you see here in the gray area, so 10 years. And then at age 40, for whatever reason, they had to get on Federal Disability Retirement, and they’re going to be on that from age 40 to age 62. So what you’re looking at here is 22 years on that benefit. And what we’re saying here is that you are going to receive creditable years of service for the 22 years that you are on the benefit. So it’s going to look like you had been working for the federal government from the age of 40 to 62.

So once your retirement is recalculated at the age of 62, it’s gonna look like you had worked there for 32 years.

Grant: That’s huge too, because at age 62 if you have more than 20 years of service, you get a 10% bonus on your service time. And that’s what happens on Disability Retirement—on your 62nd birthday, if you’ve got over 20 years of total federal service including this bit that gets added, then you receive the bonus. That’s huge.

Nick: Yeah, so not only is Federal Disability Retirement helping you now, it’s going to continue to help you in the future while you’re on it.

Maintaining Health and Life Insurance

Nick: So let’s move to the next slide—maintaining health and life insurance. This is what we’re here to talk about today. We have a lot of webinars that go deep into Federal Disability Retirement, all the benefits, but today we want to talk specifically about this one and the considerations that you need to make while you’re thinking about getting on Disability Retirement and what health and life insurance could look like.

So just so that you’re aware, once you move on to Federal Disability Retirement, you have the option to maintain your current health and life insurance elections.

Health Insurance Options

Nick: So let’s talk about health insurance specifically first and what that looks like.

Grant: So health insurance for federal employees, oftentimes referred to as FEHB [Federal Employees Health Benefits], is something that they pay for a portion of your premiums. You’re in a giant group and it’s a good insurance plan. Usually, it’s Blue Cross Blue Shield and it allows you to have a really good benefit for you and your family.

One thing that’s important to note here is that when you’re on FEHB benefits and you want to carry them into your retirement, you have to have been on that benefit for five years or all eligible time. So if you were only a federal employee for four years, then you need to have been on there for all the time that you were eligible to be a member of that program. And that’s true whether it’s Disability Retirement or regular retirement.

Nick: Yeah, so this is something that a lot of people are concerned about when they’re getting on this, because they’re in a position where they’re injured or disabled and they’re worried about, well, how are they going to keep health insurance?

Grant: That’s right. Especially if it’s not a work-related injury and you don’t have a third-party means of paying for that medical care, this is for any kind of illness or anything else that would arise after retirement that you need. So it’s a way to get off of being dependent purely on Medicaid and having a private insurance carry you through your retirement.

Nick: Yeah, so this can really ease a lot of people’s fears about moving into the future.

So a couple things that you need to consider is what happens once you’re approved for Federal Disability Retirement. What’s that going to look like? So let’s talk first about being on the rolls—what’s that going to look like?

Grant: Yeah, so if you’re still employed by your agency and your benefits haven’t been terminated yet, then you can just continue your health insurance right on into retirement. Nothing really changes. They just shift from taking your premiums out of your paycheck to taking them out of your annuity.

Nick: Yeah, and then a lot of people are wondering if they’ve been terminated or separated from service and their insurance has been stopped, right? What’s that look like?

Grant: If your benefits have been terminated after a separation from service, you can apply to have them reinstated. And if they are—which they typically are—they’re reinstated retroactively. You owe them the premiums for that time period, but it’s usually coming out of some sort of retirement back pay, so it effectively always still comes out monthly. It just may come out in a chunk if they have to pay you a chunk.

Nick: Yeah, and that would include any medical expenses that you had to pay. They would go back and—

Grant: You gotta retroactively file those claims and go through the insurance.

So yeah, so if you had to pay for some health expenses or doctor visits out of pocket, those can go back and be retroactively put in the insurance and the claim be paid.

Nick: Got you. Okay.

USPS Employee Premium Changes

Nick: All right, so one other thing that we wanted to make sure that everyone’s aware of—specifically USPS employees—is that the standard federal employee pays their portion of their premiums and the federal government takes care of the other portion.

[Editor’s Note: As of January 1, 2025, USPS employees transitioned to the Postal Service Health Benefits (PSHB) Program with different contribution rates. View current USPS health insurance information here.]

Spouse and Dependent Coverage

Nick: So let’s get into real quick what everybody’s probably thinking if you have a spouse or dependents—are they going to be able to continue to receive health insurance just like they have been? And the answer is yes. It’s just that simple. Just like they currently have been and what you’ve currently been paying, they’re going to be able to receive those.

Grant: That’s right. There is this one big kind of caveat though, and it’s important to kind of talk about it right now. You can’t add benefits right here. You can only subtract benefits. So if you haven’t had your spouse and kids on there, you can’t necessarily add them on unless there’s an open season coming up. And if you’ve never had this benefit—like we said earlier—you have to have had it for five years prior to the retirement.

But maybe even more importantly, there are—there’s a part of your retirement called a survivor election, a survivor annuity. And the survivor annuity is a form of insurance that leaves a payment to a surviving spouse in the case of your death. And woven into the choice that you make about your survivor annuity is a little piece of the health insurance puzzle that states that your spouse and dependents cannot stay on the benefit—the health insurance benefit—after your passing if you haven’t elected at least a partial survivor annuity.

So it’s a little bit complex, but we won’t talk about it in detail here so you can understand it. The maximum survivor annuity for a FERS employee is going to pay your surviving spouse 50% of your unreduced federal retirement. In order to pay for that, it’s going to take a 10% reduction of the gross monthly annuity.

A partial survivor annuity works the same way, but it’s a 5% reduction in your monthly annuity for a 25% benefit paid to your surviving spouse.

Then the third option is no reduction, no benefit for a spouse. But if you don’t choose the maximum or the partial, your surviving spouse cannot continue to receive or stay on the FEHB benefits after you pass.

Nick: Yeah, and that’s a really important thing to remember and to think about. And that’s what we’re talking about here today—is to show you all of the options. This is different for everyone in whatever situation that they’re in. You really need to be considering these things in the context of your situation, because there’s no one-size-fits-all for everybody.

Grant: And I can’t possibly emphasize enough—you should not watch this webinar and then go make your elections. You should watch this webinar and probably think, “I need to talk to somebody who deals with insurance,” or talk with us about what your options are. That’s one thing we really do walk through with people is understanding these things on an individual basis so they can at least make a really informed decision about what’s best for them in their life.

Nick: So one thing I just want to make sure is very clear here when we’re talking about a survivor annuity—we’re talking about that monthly income that would come after your passing to your spouse, right? Now if for some reason your spouse passed away before you, that money would essentially be gone. It doesn’t go to your dependence upon your passing, right?

Grant: The survivor annuity is only for a spouse. The health insurance continuation can be for dependents, but if you’re still alive it’s irrelevant.

Nick: Yeah, so I just wanted to make sure that was clear—what we were talking about there when we talk about a survivor annuity—because we know this can be confusing. But like I said, we just want to give you all of your options so you can really start thinking about what could be the best choice for you and your family.

Life Insurance Options

Nick: So real quick, let’s get into life insurance options and understanding what those options are and how they could play out on Disability Retirement.

So let’s talk about FEGLI first.

Grant:So Federal Employee Group Life Insurance, or FEGLI, is tossed around as a pretty generic term for group life insurance offered through the federal government. And there’s multiple formats, but the ones that are most common that you’re going to see is your Basic life insurance. And that’s going to be an amount of money equal to one year of your salary rounded up to the next thousand plus $2,000. And that’s the most common type out there.

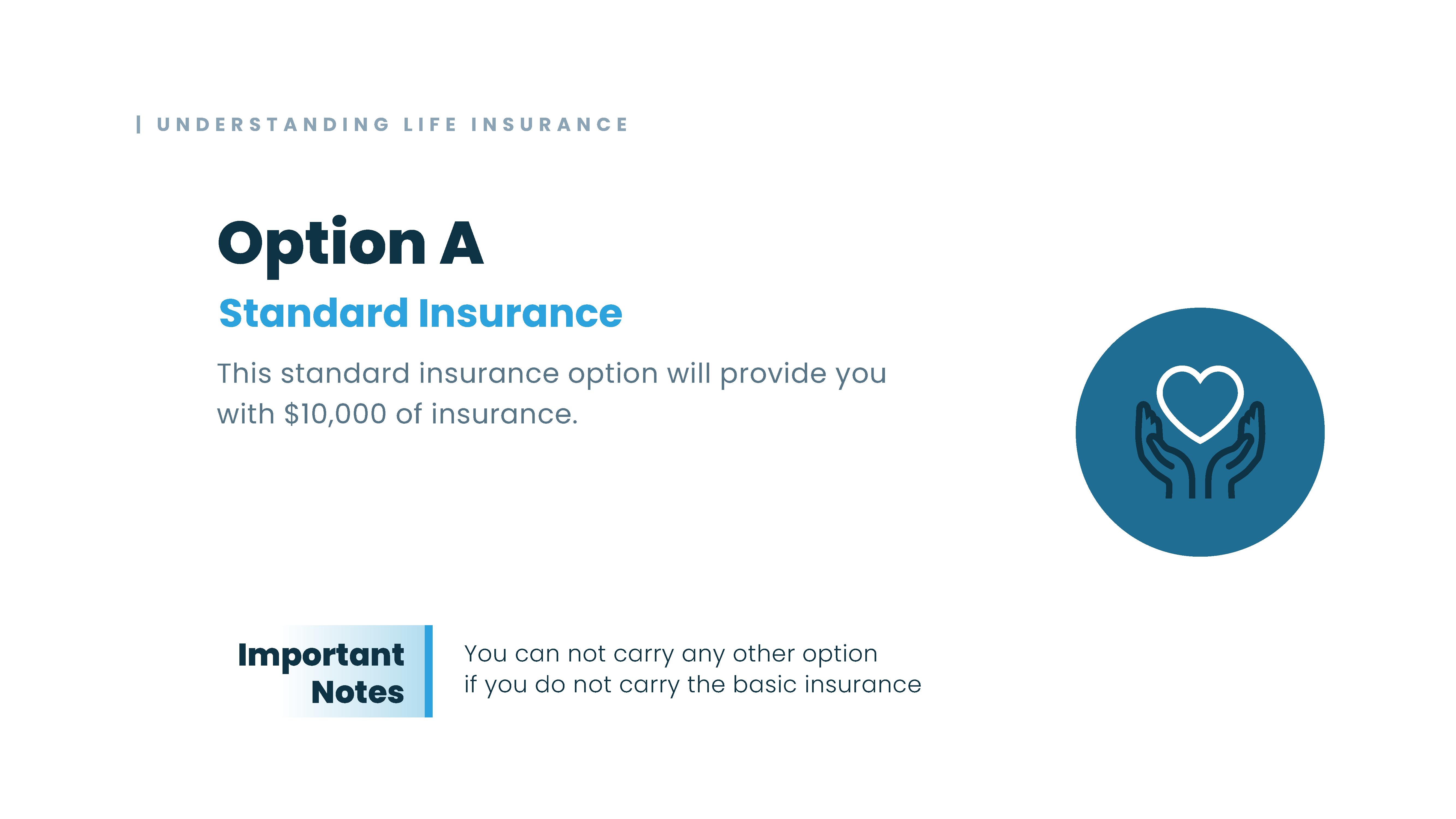

But there’s also an additional three options that you can elect to add. You have to have the Basic to add these, but they’re pretty simply named—Option A, Option B, and Option C. So let’s go through these one at a time.

Grant: Option A is called standard insurance, and it’s just a $10,000 lump that you can add. If you choose Option A, you’re going to pay an additional premium and it’s worth $10,000.

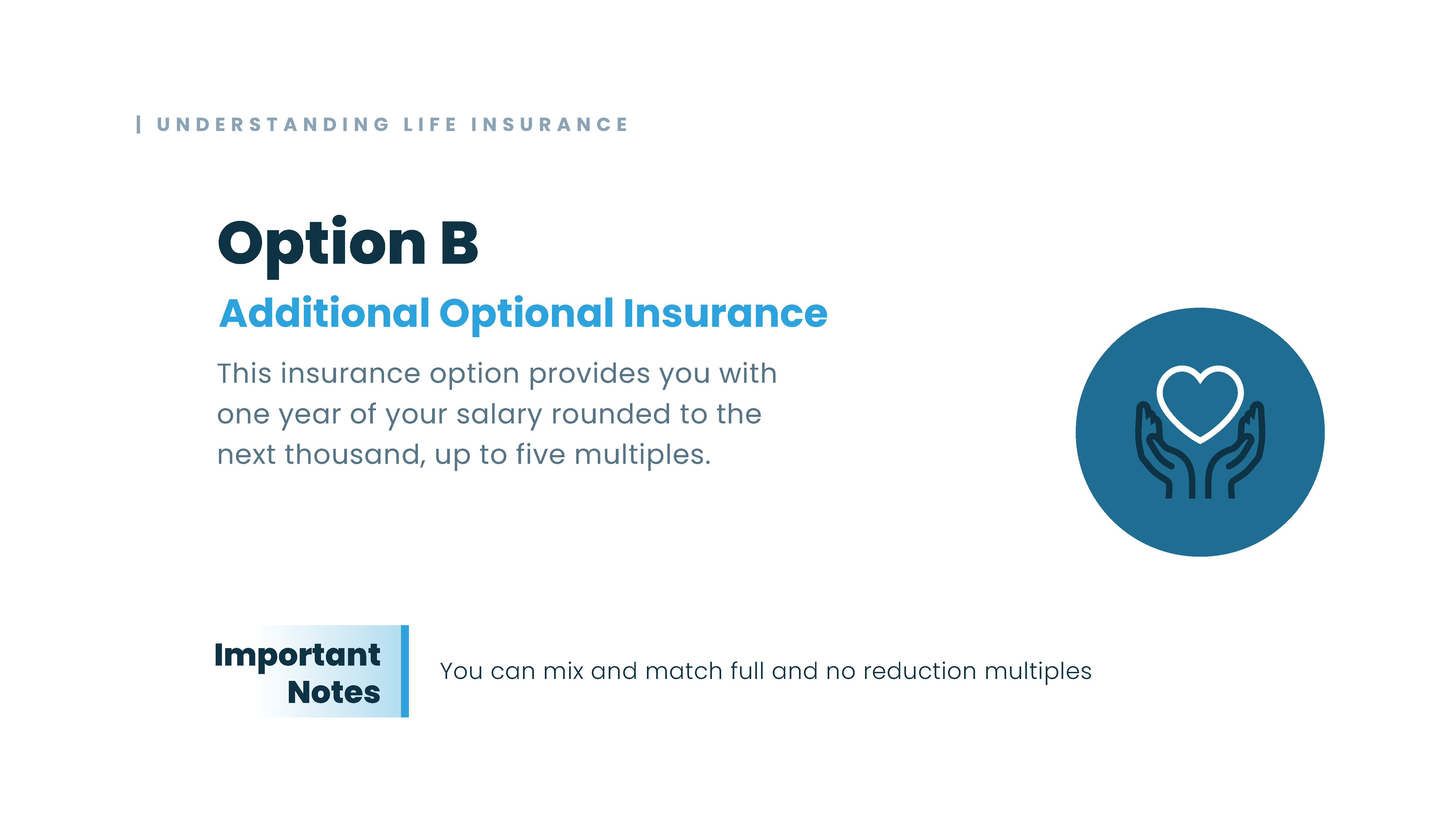

Option B is called additional optional insurance. This one’s a little bit more complex, but essentially you can add additional multiples of your salary up to five total multiples. And each time you add a multiple, obviously the premium goes up.

Nick: So let’s just say you made $100,000. What we’re talking about is a maximum of $500,000.

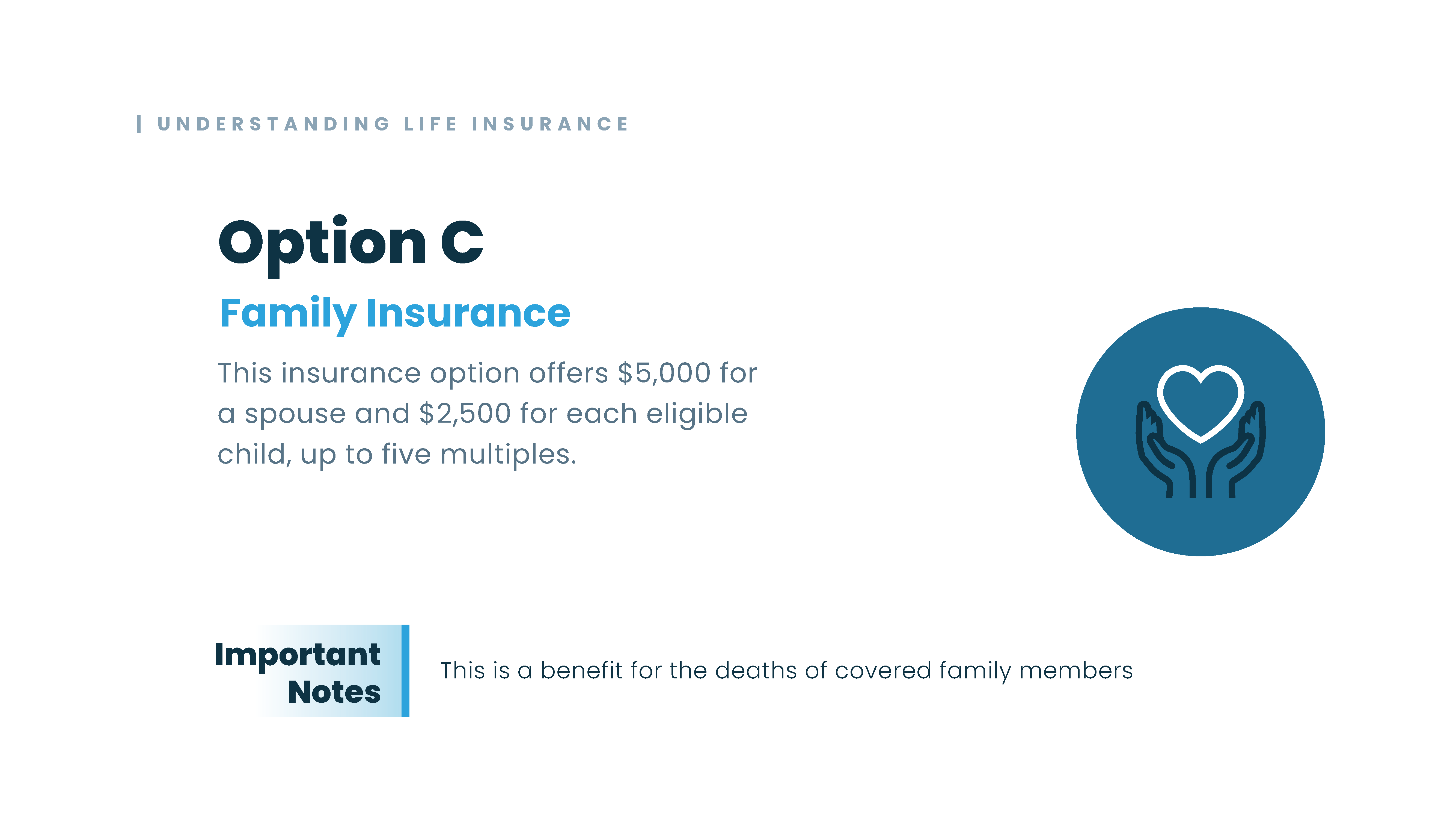

Grant: It would be a maximum of an additional $500,000. That’s right, in addition to your Basic. So the last option is Option C, and it’s not based on your salary. It’s a standardized amount and it’s for members of your family if they were to pass away untimely. You can also add up to five multiples of this. Each multiple would pay out $5,000 for a spouse or $2,500 for each eligible child, up to five multiples.

Nick: So just to make sure everyone’s clear, this has to be something that you are already enrolled in and have elected for once you’re approved for Disability Retirement, right?

Grant: That’s right. You have to have been enrolled in FEGLI for five years, and there isn’t even a waiver for the all-eligible. So, it really has to be five full years in FEGLI to be eligible to take that into retirement.

Nick: Okay, that’s great. I just wanted to clear that up so everyone understood that.

What Happens at Age 62

Nick: So we’ve talked a lot about that 62-year-old age mark here, and Grant mentioned it being so important earlier. So let’s talk about what happens at age 62 so that you know what to expect and what to be thinking about.

The first thing is your retirement is going to recalculate into a regular retirement. So, what you would be on is a Disability Retirement, and at age 62 that’s going to convert over to a regular retirement. And that’s going to recalculate based on your service. And like we mentioned before, you would have some creditable years of service to add to that since you’ve been on the benefit.

And additionally, you’d be eligible to start drawing regular Social Security. And that’s something that you really need to talk to a financial advisor, specifically one that has experience with federal employees, that understands all the benefits that you’re looking at as a federal employee and to know when the right time for you to take that is.

And then like we mentioned here, once you turn 62, you’re going to be able to maintain that health and life insurance like you would if you were just retiring normally. But you might have some considerations to make with your life insurance there, because those premiums are really going to take off once you get to that age.

Grant: Yeah. I don’t know if there’s anything that’ll blow your mind more than how quick the premiums go up in FEGLI once you hit your full retirement ages. So, it’s definitely an advisable idea, no matter what age you are, to at least look into the idea of getting your life insurance situation taken care of outside of the federal government. The younger you are and the more insurable you are—meaning the less life-threatening your disabilities are—perhaps the better deal you might find on the open market.

This is a really good benefit for people who are going to have a hard time getting insured or are closer to this 62-year-old age at the time they’re going through this period of switching to a Disability Retirement.

So, every situation really is different, and we want to walk through that with everybody individually. But the truth is, keeping your FEGLI later on into your life does become cost prohibitive.

Nick: One thing that we talk about a lot is not risking your future. And we don’t say that as a sales pitch—it’s because you have so much at stake when it comes to income and finding a secure future with these benefits.

Grant: Yeah, I think that’s one thing we really want to do—is we want to give away information as much as possible, and it’s a free consultation if you want to call us and let us at least kind of walk through with you. Because one thing I know about this is I know you’ve just watched a webinar. You may have watched a lot of our webinars before, and hopefully you’re getting something out of them that’s really helpful to you. But without it being specific to your situation, it can be a lot of information—like trying to drink from a fire hose. And when you have all of that going through your mind, it can be difficult to understand what really is at risk or if I do this in this order, do I drop any balls.

And that’s one thing we want to make sure—that everybody who has questions can get those questions answered, at least figure out what the best plan is. That’s a value that we offer for free because we really do think it’s worth it for you to know. And if it makes sense for us to be on your team, that’s when we move forward in that case.

Nick: Yeah, it’s just like we recommend people talk to a CPA about doing their taxes, right? Now imagine if you had a tax return that was worth maybe a million dollars. You definitely want to talk to a CPA at that point and make sure that you’re getting all that money from the federal government. So, it’s something that we really really enjoy helping people walk through and finding what they need in that benefit.

Key Takeaways

Nick: So, to just kind of wrap up here, I want you to remember all the basics that we talked about with Federal Disability Retirement—that monthly annuity it provides you, the ability to work in the private sector, the creditable years of service. Don’t forget about that one. That one’s really important when you’re thinking about this. And then obviously what we’re here to talk about today—all of your health and life insurance options, the things that you need to be thinking about and considering as you move into this Disability Retirement.

So really take the time and invest in your future by taking the time to consider these and talk to professionals that can show you how all of this is going to play out as you move into retirement.

Nick: So we’re excited to talk to you about this. We’re happy to sit down and have a consultation with you and talk to you more about all of this.

If you have questions right now, go to that chat box in the bottom right corner. We have people here that are taking questions and providing answers as quickly as they can. Sometimes those questions get a little bit specific to certain situations, and they might tell you to give us a call. And that’s just so that we can get all the details to know how to guide you the best way possible.

Thanks everybody for being here today. Like I said, check out our website where we have tons more resources. We have a YouTube channel that’s full of videos just like this, FAQ videos to help you walk through all those questions you might be having as you look for a benefit like this. So we appreciate you all being here today and we look forward to seeing you here next time. Thanks.

Grant: Yeah, absolutely. Thanks for having me, Nick.

If you want to discuss your options, give us a call today for a free consultation!