Quick Takeaways

- You can earn more than your federal salary: 60% in the first year, 40% after, plus up to 80% of current position pay from private sector work.

- Denials are common but appealable: 99.9% success rate through the reconsideration process with proper representation.

- This is a pretty long process: It’s important to just trust us, trust your case manager. We are working diligently to get this all done and completed for you.

- Those deadlines are really important: We’ve got to keep an eye on all of those deadlines and be aware of them.

- If you get denied you do have options: it is scary but we’re here to help and we’re here to walk through those different options with you.

Common Questions

Q: What medical conditions qualify for Federal Disability Retirement?

A: Your injury or illness must be expected to last at least 12 months and prevent you from performing at least one essential function of your federal position, even with reasonable accommodation. The condition must be tied to a service deficiency at your agency.

Q: Can I work while receiving Disability Retirement benefits?

A: Yes, you can work in the private sector as long as you stay within your medical restrictions and don’t exceed the 80% earnings cap of your former position’s current salary.

Q: What happens if my application gets denied?

A: You have 30 days to request reconsideration. Your case gets assigned to a different medical specialist, and most denials are overturned at this stage.

Q: Do I have to apply for Social Security Disability?

A: Yes, it’s required before submitting your Federal Disability Retirement application. You must apply but don’t need to be approved – just show proof you applied.

Q: How long does the entire process take?

A: Typically, 10-20 months total: 1-4 months for application prep, 1-4 months at your agency, and 8-12 months at OPM [Office of Personnel Management] for final decision. This is subject to change and depends on the situation.

Full Webinar Transcript

Kimberly Bear (Director of Case Processing): I’m really excited to be here today to talk about the federal disability application process and introduce Rose, our senior disability case manager, who is very knowledgeable on this subject.

Rose McFarland (Case Manger Supervisor): Hi Kimberly, thank you for having me. I’m excited to go over this information with everyone.

Kimberly: Today we’re going to cover all kinds of things from just a quick overview of what the Disability Retirement is, the application process, and even go over the decision whether you get the approval or the denial from the OPM.

Understanding Federal Disability Retirement Benefits

Kimberly: Let’s get a base understanding of what the Disability Retirement is so you understand what it is that you’re applying for. The Disability Retirement is specifically for federal employees who are no longer able to work because of an injury or an illness, and this injury is expected to last for at least one year.

This benefit isn’t something extra that you have to pay for – it’s already built into every career FERS employee. This benefit is out there, it’s wonderful, and it’s already there for you. You just need to know how to use it.

Key Point: Some highlights of this benefit include that monthly annuity payment you’ll be receiving while you are no longer able to work, you also have the option to work in the private sector while receiving this benefit, you’re going to be earning those federal creditable years of service while on this benefit, and then that health and life insurance which is really important.

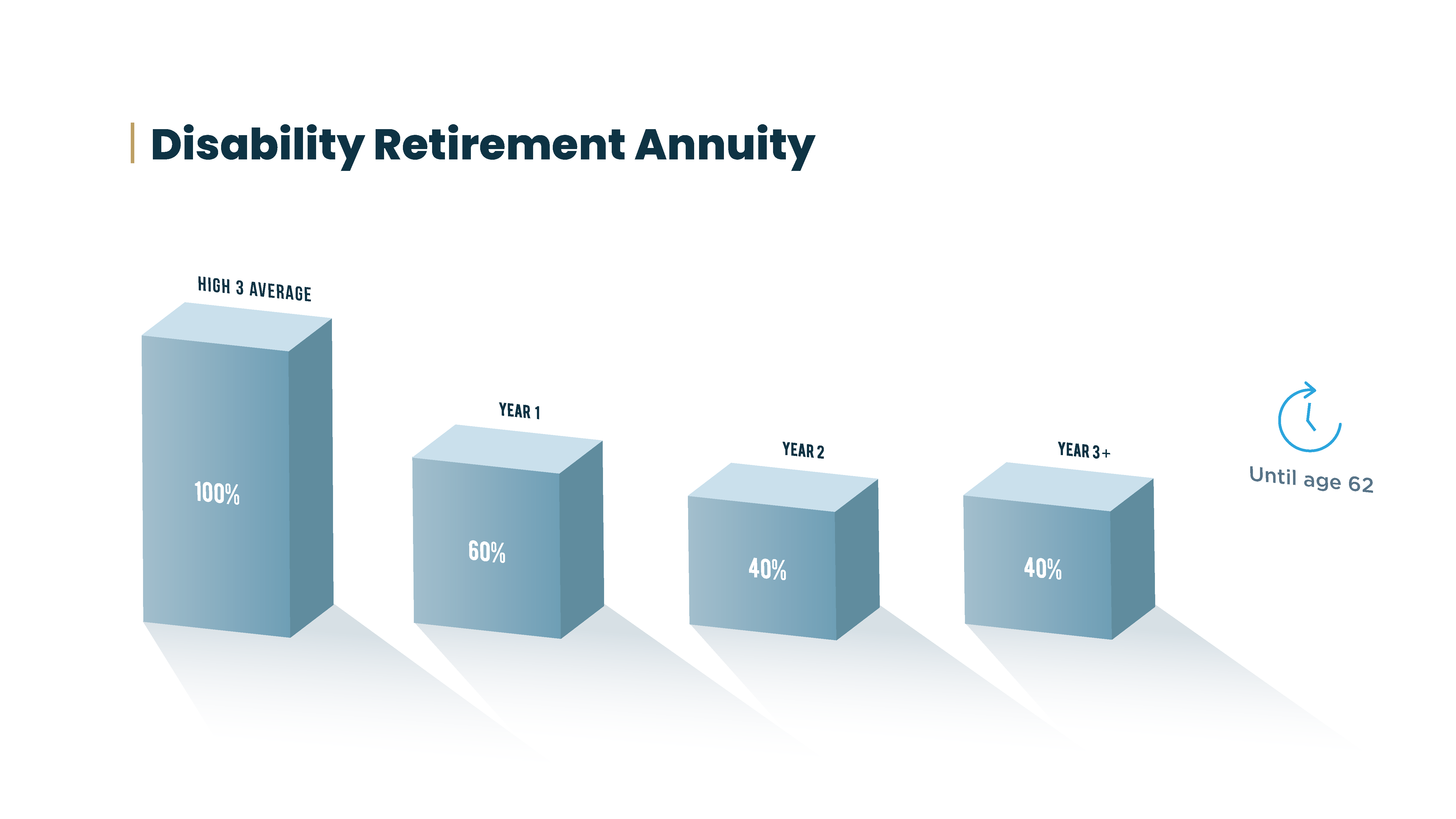

Rose: Once you’re approved for the Disability Retirement benefit you are going to receive 60% of your high three salary the first year and 40% of your high three average salary every year after that until you reach age 62. It’s important to remember that this is taxable income.

Clients often ask how their high three is calculated. They will calculate your high three by your highest 36 consecutive months of basic pay throughout your entire federal service career.

Kimberly: You can see in that first bar your high three average – that’s 100% of your salary. For year one it shows you what your 60% is going to be, and then your second year and every year after until the age of 62 you’ll be receiving that 40% of your high three average.

Working While on Disability Retirement

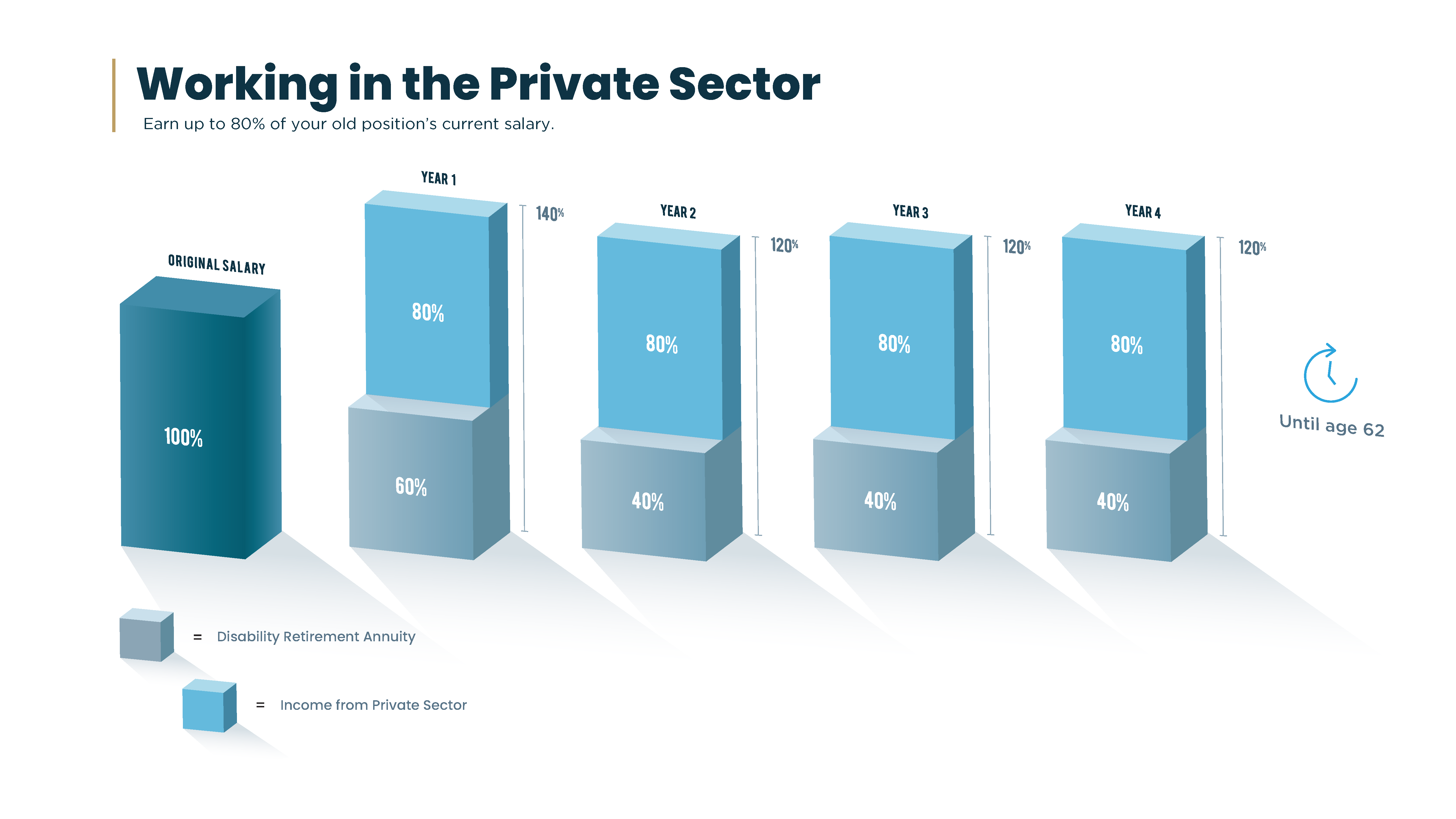

Kimberly: You might be thinking that 40% isn’t enough, that you’re not going to be able to survive. This benefit does allow you to work in the private sector while receiving that Federal Disability Retirement because it’s an occupational disability and not a total disability. You do have that ability to work in the private sector and earn up to 80% of what your old position’s current pay is.

Rose: One thing I often tell my clients to remember is that this acts as a supplemental income. It is not intended to fully replace the income as if you were still working full-time for the federal government.

But one thing great about the benefit is it does allow you to work as long as it falls within your medical restrictions and within the earnings cap, which is that 80%.

We really encourage our clients to find work outside of the federal government. I’ve had clients that go on to further their education, teach in the field from where they retired from when they’re unable to actually perform those same functions, start their own businesses. There’s really so much you are able to do.

Kimberly: Similar to our last graph, you can see here your original salary at 100% and the lower darker bars are that 60% and 40%. But the top bar, that light blue, is the 80% that you could earn in the private sector. If you’re looking at year one, two, and every year after, you can potentially make even more than you did in the federal government while receiving the Disability Retirement and working in the private sector.

Accumulating Years of Service

Kimberly: While you’re receiving this benefit you still will receive those credible years of federal service. What this means is that every year on the Disability Retirement will count as an earned credible year of federal service, and this will all add up until the age of 62.

Rose: Let’s look at this graph – this is a great visual of how the years of service calculation works. You’ll see someone at the age of 30 who started their federal service go to age 40. At age 40 they became unable to perform those essential functions and that gave them 10 years of federal service.

However, once they applied for the Disability Retirement and were approved, that means that every year until age 62 would count as a creditable year of service, giving them 22 years on the Federal Disability Retirement benefit. At age 62 that would give them 32 years of federal service, which is huge when calculating those regular retirement rates.

Kimberly: I just want everyone to take a moment to look at this because this is very significant. Instead of ending your career at 10 years of federal service, this person on this chart will now retire with 32 years of federal service. That is a significant difference and that’s going to pay huge dividends when they reach that regular retirement age.

Health and Life Insurance Benefits

Kimberly: Another benefit with the Federal Disability Retirement is you do have the option to maintain that health and life insurance once you’re approved. That does give you some peace of mind that you have some different options into this early retirement.

Application Process Overview

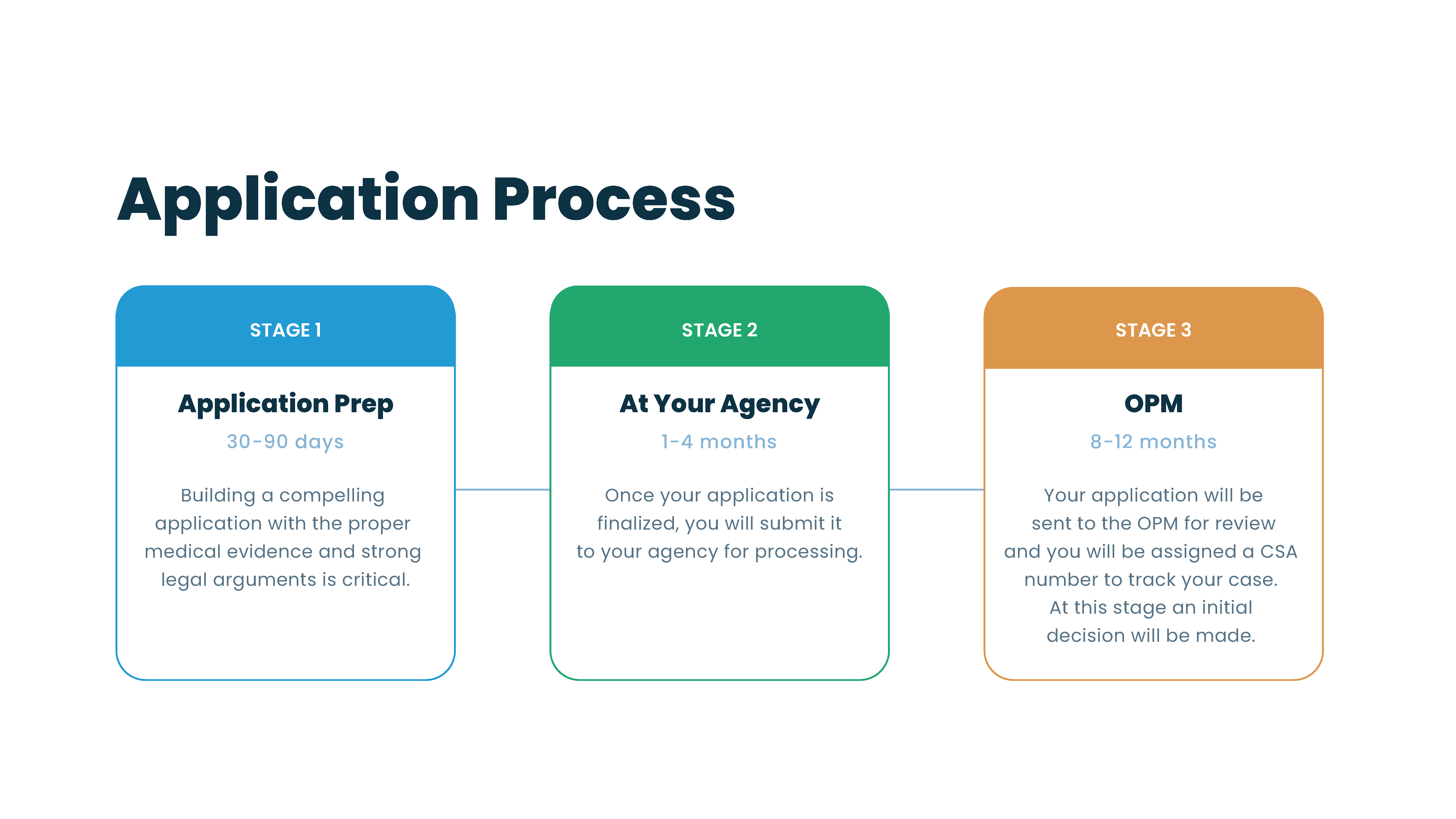

Rose: For the application process you’re going to see three main stages. Stage 1 is application prep, Stage 2 at your agency where your application goes prior to being submitted to OPM, and then Stage 3 – the OPM phase – which is when your application is at the OPM awaiting adjudication.

Stage 1: Application Prep

Kimberly: The first stage, the application prep, is where we will work directly with you and your assigned case manager on building your application and making sure that the forms are correct, everything that’s necessary is in them, and that we have a strong case ready to submit.

This prep process while you’re working with us and your case manager typically takes one to four months, just depending on how quick your doctors are and how quick things come in the mail from you.

Social Security Disability Requirement

Kimberly: One thing that is required at this stage is the Social Security Disability Insurance application.

Rose: One of the requirements for a Disability Retirement application is that you must apply for Social Security Disability. This can be really confusing for a lot of people because Social Security Disability generally is harder to get, and if you’re still working it can be an automatic denial. However, you are not required to be approved – only to apply.

Key Point: We’ll walk you through what that would look like. Although we can’t represent on Social Security Disability, we can walk you through what we need for proof. If you are approved for Social Security Disability, this is actually really supportive for a Disability Retirement claim and we would absolutely send that directly to OPM as supportive documentation.

Kimberly: You can apply for this benefit by phone, online, or in person, but we do need this completed before we’re able to submit your application for Disability Retirement.

Medical Documentation Requirements

Kimberly: The next section is going to be that medical support that we work on gathering with your providers. We do need some supportive medical documentation, and this medical support does have to show that your condition is going to last for at least those 12 months and then somehow tie that medical condition to your service deficiency at your agency within your federal position as well.

Rose: This is a place we’re really able to help people. We know exactly what the OPM looks for and we’re pros at knowing those requirements for the approval of a Disability Retirement application. We really look at our clients’ medical conditions, their restrictions, and we offer that one-on-one communication with the facility or with the doctor when we’re able to try to get the strongest document we can get for each particular claim.

Service Deficiency Documentation

Kimberly: The next thing that we are trying to put together while we are building your application in phase one is the service deficiency support. This is where we will reach out to the agencies to gather some required agency documentation, and some of this can also be used to support your case.

There are some specific forms that we reach out for in hopes of getting completed before your application is sent. These would report things like whatever service deficiency you have – whether it’s absences, inability to perform your job, or conduct issues. These will be included in your application for Disability Retirement as well.

Understanding Reasonable Accommodation

Kimberly: While we’re still talking about what goes into your Disability Retirement application, one subject that will inevitably come up is going to be the reasonable accommodation process, and that is something that we can walk you through as your case manager.

Rose: The reasonable accommodation process is very confusing for many of my clients, and with good reason. It can be a confusing process for sure. Basically, the OPM wants your agency to show that you are unable to be accommodated in your current position of record as a result of your medical condition.

What that means is we need to show that even if your agency were to provide a sit-stand desk or telework, you still wouldn’t be able to perform at least one essential function. Each agency processes the reasonable accommodation differently. Some require certain forms completed – that’s where we step in.

Key Point: Although we don’t technically represent on the reasonable accommodation process, we really do as much as we can with our clients as far as completing forms, offering direction and guidance. The reasonable accommodation process can provide a lot of really supportive documentation that is great to include in an application.

Stage 2: Submitting Your Application

Kimberly: Now that we know what goes into your application and how important that information is, we would move on to the next stage – Stage 2, which is submitting your application. This stage can vary at each agency. Typically we see that it takes one to four months just because each agency does process a little bit differently.

We do work with all of the agencies so we are pretty aware of how each one processes, just so that we can keep things moving a little bit smoothly.

Special Processing for USPS and Military Agencies

Rose: Two agencies that we deal with often are USPS [United States Postal Service] and several different military federal agencies.

For USPS employees, your application is sent directly to HR Shared Service Center where it is processed. They’re a little bit more difficult to communicate with and they’re very strict on only communicating with their employees. This is where we work with you directly and tell you what to say and work with you to get information we need, but we’re of course with you every step of the way.

Military agencies – if you are employed by a military agency you will be sent to their civilian benefits center. Every agency is different, every HR is different, but we have a lot of experience with just about every agency so we’re here to walk you through every step of the way.

Separated Employees

Kimberly: If you are separated and you’re submitting this application for Disability Retirement, this would actually bypass phase two and be submitted directly to OPM.

Important: One important thing to know is that you have to submit your application for Disability Retirement within one year of your date of separation. The OPM is very strict on this and there is no getting around it – you have to submit your application within one year of being separated from your agency.

Stage 3: OPM Review Process

Rose: Once your application gets to OPM you will be issued a CSA number. This generally is given via mailed letter directly from the OPM. Once you’re issued that CSA letter, your application is put into a holding until you’re assigned to a medical specialist who will eventually adjudicate the claim.

OPM can oftentimes request updated medical or they can request certain documentation that they want for review. All of that’s very normal and no reason for concern. We work with our clients to make sure that everything OPM requests gets there in a timely manner.

Additionally, we also like to submit medical and supportive documentation even if the OPM doesn’t request it. Anything we’ve received from the date your application was submitted to the agency, we will review it and if it’s supportive we’ll go ahead and send that directly to OPM through some direct contacts we have, that way it’s able to be added to your file so your medical specialist has all the supportive documentation available to make that positive adjudication.

Kimberly: Although this phase can take 8 to 12 months, we strongly advise you not to reach out to OPM directly. Please reach out to us for any updates as we’ve got that direct communication with them.

Decision and Next Steps

Approval Process

Kimberly: Once OPM has reviewed your application, the next thing that you can expect is to get either an approval or a denial letter from the OPM. Of course, we hope that we get that first initial approval.

If you are approved from the OPM, they do start the process of finalizing your benefits and this will include those interim payments which you will typically receive until your full benefit is finalized, which can take up to five months. During this time, if you’re not already separated from the agency, this is when you would be separated, and the agency will finalize your file and send everything over to the OPM.

Handling Denials

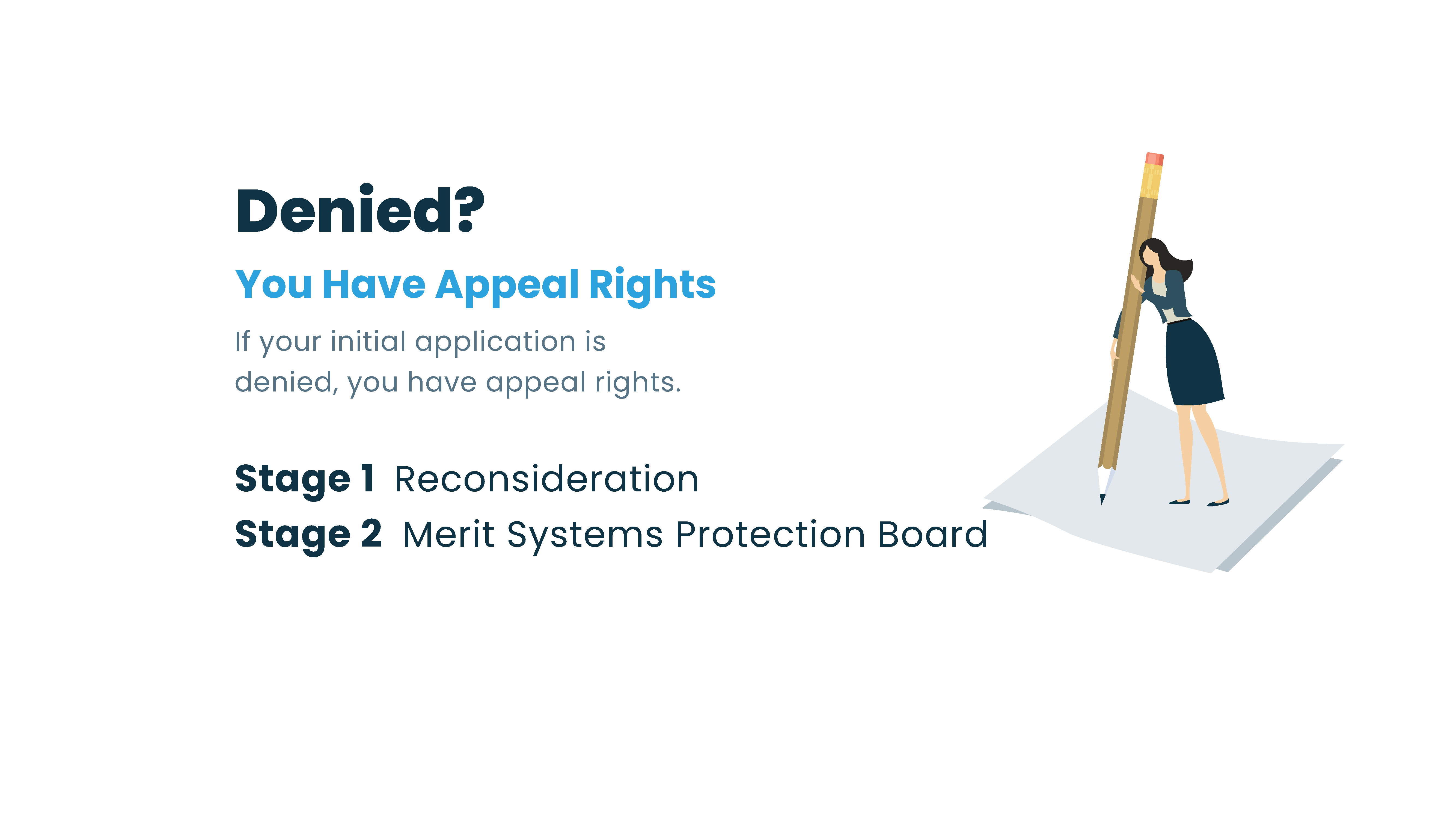

Rose: Denials – no one wants to see a denial, and I completely understand. I know it can be disheartening to open that letter when you’re hoping for a favorable decision. But one thing to keep in mind is denials can be common, and that’s why we carry you through these various levels of representation because we don’t submit applications for Disability Retirement that we don’t feel can be won.

Once you’re denied, send us a copy of that denial letter if we haven’t reached out to you first, and you’ll then be given to our attorney in the office. She walks you through that reconsideration phase – it’s very similar to the initial application phase. She’ll get some new information from you and just see what needs to be done to combat the decision from the OPM for that denial. She’s wonderful at what she does, which is why we have a 99.9% success rate.

Reconsideration Process

Kimberly: A couple of things to keep in mind: if your application is denied you do have 30 days to request that reconsideration, and by doing that you also can request that additional 30 days. During this time is when we’ll work with you to continue building on your claim, writing up the appeals, and just getting everything submitted to OPM that’ll get you that approval.

One more thing to note about the reconsideration level that might make you feel a little bit better is that your application does get bumped to a different medical specialist, so you’ll have a new set of eyes reviewing and making this new decision at this level.

MSPB Appeals

Kimberly: If you were to get that denial at the reconsideration stage, you do move on to the MSPB [Merit Systems Protection Board] stage, and this is something that we do walk you through as well. We’ve got experience here as well, so you are still in good hands.

You do have appeal rights at this stage if you’re denied at that reconsideration level. We’re able to request to appeal to the MSPB within 35 days. This does mean that your claim will be assigned to a judge, and an appeal will require a telephonic attendance with the judge and the agency representative which was assigned by the OPM.

If you are denied at this stage, you do have the ability to reapply for the Disability Retirement as long as you are still employed with the agency and we could then prove that your condition has worsened or caused a further service deficiency.

Additional Benefits and Decisions

Survivor Benefits Options

Rose: When you’re speaking with your case manager during the application appointment, they’re going to get to a point where they’re going to ask you about a survivor annuity and ask you to elect one. This can catch a few people off guard depending on if they’ve done their research prior.

You’re going to have three options here:

- Option 1: Maximum survivor annuity – in the event you were to pass away before your spouse, your spouse would receive 50% of your unreduced annuity every month. However, while you’re living the OPM will reduce your payments by 10% every month.

- Option 2: Your spouse will receive 25% of your unreduced annuity payments every month upon your death. However, while you’re living the OPM would reduce your payments by 5% monthly.

- Option 3: No survivor annuity – if you were to pass away before your spouse they would not receive any of those monthly retirement payments, but in return OPM would not take anything out of your check for this particular benefit.

Key Point: This isn’t life insurance, this isn’t your other retirements – this is strictly referring to your Federal Disability Retirement payments. It’s also important to note that if you’re choosing option one or two and you have those payments reduced, if your spouse were to pass before you, you don’t get that money back. You are able to change that choice so they no longer reduce your payments, but you will not get that money back.

Insurance Options

Kimberly: You do have the ability to maintain your health insurance once you’re approved if you’re eligible. You are going to still be responsible for paying the portion of the premium – it will come out of your Disability Retirement from the OPM.

One thing to note on the survivor election is if you choose option three that there is no survivor annuity, this does mean that your spouse would no longer be eligible to carry over those health benefits if you were to pass first.

Rose: With the federal life insurance that you are able to keep in retirement, you have three different options in addition to your basic life insurance:

- Option A: Standard additional $10,000

- Option B: Additional option insurance – allows you to have up to five multiples of your salary

- Option C: Family life insurance – up to five multiples and it’s $5,000 for a spouse and up to $2,500 for each child

You can drop coverage at any time after approval, but keep in mind once coverage is dropped you can never go back up with coverage or get it back once it has been dropped.

Important: Once you reach age 55 the premiums for your life insurance do climb, and from our experience it can become a very expensive benefit to keep in retirement. This might be a great point to look into different options or reducing your coverage so it makes it more affordable in your retirement.

Kimberly: All of these benefits are fairly permanent once that decision is made – they are going to carry over through your regular retirement. You only have 30 days from the day your Federal Disability Retirement is approved to make any changes to your survivor benefits, health and life insurance, and things like that.

Final Recommendations

Kimberly: Everything needs to be complete and accurate and submitted the first time around because this is really important to your future.

Rose: It is a whole lot of information to take in initially. While you see the general overview and averages, one thing to keep in mind is that every application and every process can be different. Every day we’re looking at emails or correspondence from agencies asking us questions, or perhaps your local HR isn’t informed on the process and we kind of have to help them through it as well.

You can trust our expertise in making sure that when we ask for certain documentation or when we’re asking you to walk through a certain process, it really is for your benefit.

Our goal is to create the strongest application initially as opposed to having to do damage control once something has already been submitted.

Kimberly: We always advise our clients not to risk their future. We’re here to help and we’re here to get this benefit filed correctly and approved for you.

Thanks for taking the time to read this webinar! We hope this information has been helpful. If you’ve got any questions about your case, or you’d like to learn more, call us today for a free consultation or check out our YouTube page for more resources, educational material, and helpful webinars like this.