Quick Takeaways

- Working in the private sector is allowed – and expected: Federal Disability Retirement is designed as income supplementation, not replacement, which is why earning outside income is built into the benefit.

- You can earn up to 80% of your former position’s current salary: That cap tracks the job’s pay overtime, including raises and cost-of-living adjustments.

- Your new job can’t be the same as your old federal role: You need to find work that doesn’t violate the same medical restrictions that kept you from your federal position.

- Private sector time still counts as federal service: Years spent on Disability Retirement are added as creditable service, boosting your regular retirement calculation at age 62.

- OPM reviews are routine, not a threat: Expect an annual income review and occasional medical reviews (stopping at age 60) — these rarely result in anyone being removed from the benefit.

Common Questions

Q: How much does Federal Disability Retirement pay?

A: During your first year, you receive 60% of your high-three average salary. After that, it drops to 40% and continues until age 62.

Q: Can I work another federal job while on Disability Retirement?

A: It’s not recommended. You could risk losing your benefits. Private sector employment is almost always the better choice.

Q: What happens if I earn more than the 80% income cap?

A: You’re considered administratively recovered, which means you lose the Disability Retirement benefit and the creditable service years you earned while on it.

Q: Do I have to get a disability from my job to qualify?

A: No. A job-related illness or injury is not a requirement. Any medical condition that keeps you from performing your federal job can qualify.

Q: What if my disability prevents me from working at all?

A: You may be eligible for Social Security Disability Insurance (SSDI) in addition to Federal Disability Retirement. The two benefits offset to a degree, but together they provide more income than either alone — and the offset disappears at age 62.

Full Webinar Transcript

Nick Child (Director of Client Acquisition): Hey everyone, welcome into today’s webinar. My name is Nick Child and I’m the Director of Client Acquisition here at Harris Federal Law Firm. Really glad to have you here today to talk to you a little bit about Federal Disability Retirement and specifically what it looks like to work in the private sector while on Federal Disability Retirement.

I’m joined here by Grant Ostrander, who is the Director of Operations here at Harris Federal. Grant is a Chartered Federal Employee Benefits Consultant. He’s also a Certified Federal Retirement Consultant, and on top of that he has his life insurance license, so he’s a really great person to hear from. He’s been with Harris Federal since the beginning and has tons of experience working with federal employees and helping them navigate their benefits. So, Grant, really excited to have you here today.

Grant Ostrander (Director of Operations): Thanks for having me, Nick. I’m excited to be here, too.

Nick: So today we’re going to cover a lot of different stuff. We’re going to talk about Federal Disability Retirement and the benefits that go along with it, and we’re going to talk about this idea of working in the private sector, and then also a little bit about what if you can’t work.

What Is Federal Disability Retirement?

Nick: So before we get started on what it looks like to work while on Federal Disability Retirement, let’s understand what Federal Disability Retirement is, just so that everybody has a baseline understanding. Because like I said, I don’t think a lot of people know about this benefit and all the implications it has for them if they’re unable to work. So, Grant, can you walk us through a little bit about Disability Retirement?

Grant: Sure thing. You know, like you said, I’ve been doing this for a little over 17 years and I’m always surprised at how many people I talk to that have still never heard of it before. On a regular basis, there’s a lot of questions that come with it, but it’s just staggering to me how many people have literally never — their HR has never explained one word of this to them.

So the basic idea here is that any career employee that’s been paying into the FERS [Federal Employees Retirement System] retirement system has a benefit built into it that can provide some financial support and basically an early retirement in the case of a medical condition that’s going to keep them from continuing in their federal job. And it lasts until they would have reached their full retirement. So it’s kind of like a bridge between where they are now in their career and their full retirement age.

Nick: Yeah, so the full retirement age being 62, right Grant?

Grant: That’s right. 62 is the full age for FERS employees.

Nick: So what we’re talking about is somebody that can’t work right now because of a disability or illness or injury, and they need a way to get income to get them through that period until they get to regular retirement.

Grant: Yeah, it’s a way to keep a lot of the benefits that you’ve got from your employment. And keep in mind — you said they can’t work — some of these people are still working. It’s just that they can’t continue to work in their federal job anymore.

Nick: So like Grant said, this benefit comes from your FERS package. This is a benefit that’s built into it. Also the CSRS [Civil Service Retirement System] has this built in too, but anybody that’s still under the CSRS system would be aged out of this benefit by now.

Grant: Yeah, effectively there aren’t any people who were hired under the original Civil Service system. There may be one or two stragglers out there that left federal service and came back or something, but for the most part we don’t see any more CSRS folks. They’ve all reached their full retirement age anyway.

Nick: And so we leave this on here just to be as accurate as we possibly can as to who is covered under this. So we’re going to talk about the main highlights of this benefit. There’s a lot more detail and a lot more nuance to all of this, but these are the top four things that you need to know, and then we’re going to walk through each of those real quickly so that we can get to this idea of working in the private sector.

So there’s a monthly annuity — monthly income that this benefit offers. The ability to work in the private sector and earn income in the private sector. Continued creditable years of service, which is a really significant benefit. And health and life insurance — the ability to continue those.

How Much Federal Disability Retirement Pays

Nick: So, let’s get into this real quick and talk about how much it pays.

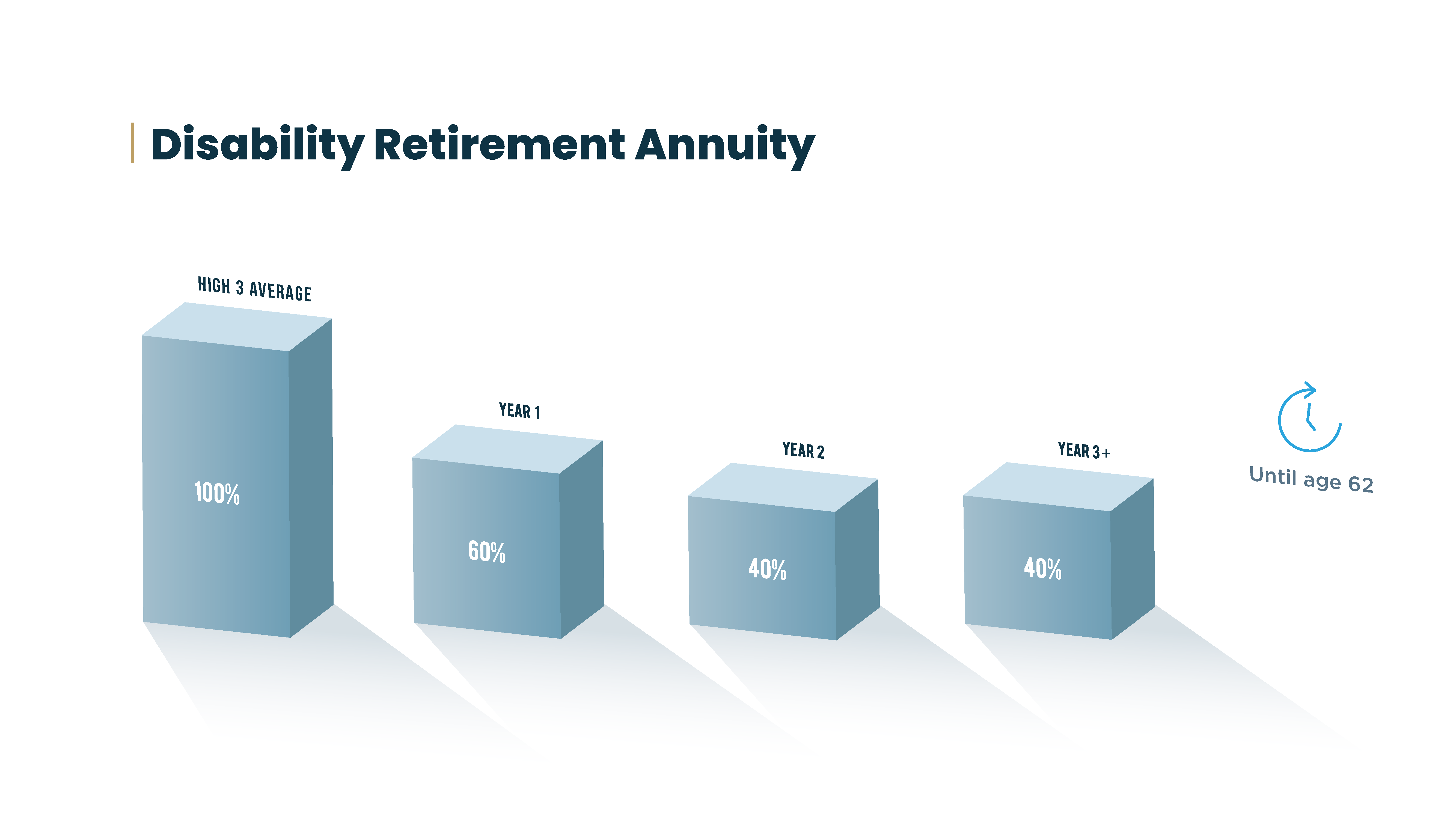

Grant: Yeah, so Federal Disability Retirement for FERS employees is what we’re going to focus on here. During the first year of eligibility, the benefit will pay 60% of that employee’s high-three salary. After that first year, it drops to 40% of that high-three salary, and that number continues until their 62nd birthday.

Nick: Okay, so you might be thinking, what’s the high-three average? That’s confusing — not everybody has heard of that, obviously. So your high-three average is just your highest 36 consecutive months of basic pay. Now that’s something that the OPM [Office of Personnel Management] calculates for you. It might be your most recent 36 months of pay, but it isn’t always. And this is also something that you can find on your SF-50.

Grant: Right. And before anybody asks, the number one question I get is, well what about my mandatory overtime, or what about my LEAP pay, or what about all these different situations for certain types of employment? The truth is, if you have a type of employment that has mandatory overtime or some kind of pay structure that is automatic, that’s going to be counted in your basic pay most of the time. So it is case by case and job by job to a great extent, but basic pay is the way the law is written. It includes things that are built into employment for certain types of jobs.

Nick: So you can see it’s a unique way to look at it, but it is in fact how the OPM measures that and calculates this Disability Retirement. So let’s look at this graph real quick and hopefully this will give you a good visual of what that 60 and 40 percent of the high-three average looks like.

This graph here is going to show you what you stand to gain on this benefit once you’re on it. So if you look there in that first bar, we’re talking about 100% of your high-three average. The first year you’re on this benefit, like Grant said, you’re going to have 60% of that come in a monthly annuity. And then every year after — there you see year two, year three-plus — until you reach the age of 62, you’re going to receive 40% of that high-three average.

So like Grant mentioned before, this is only going to last you until you’re 62, and at that time it’ll convert over to a regular retirement. This is what you would have gotten if you had been working there the whole time until 62. So this is intended to get you through that period of time until you can get on regular retirement.

Key Point: Federal Disability Retirement pays 60% of your high-three average salary in year one, then 40% every year after until age 62, when it converts to a regular retirement.

Keeping Your Health and Life Insurance

Nick: You also have the ability to maintain your health and life insurance, and I think this is a pretty significant benefit that a lot of people are worried about, don’t you, Grant?

Grant: Yeah, I think it’s a massive part of the retirement structure — to be able to keep some of these benefits into retirement and not be fully dependent upon Medicaid or some sort of supplementary plan. So the federal group health insurance plans — it’s called FEHB [Federal Employees Health Benefits] — and FEGLI [Federal Employees’ Group Life Insurance] for the life insurance plans are part of this retirement package. So if you elect to continue your benefits, you can carry those on into your full retirement age and really all the way through the rest of your life if you choose.

I think another part of this benefit that’s really helpful is when people are looking at a Disability Retirement, they’re generally suffering some major medical problems and are dealing with some chronic conditions. So, health care, life insurance, taking care of their family, are in the forefront of their mind because they’re not in optimal health. If they were, they probably wouldn’t be looking for a disability claim. Being able to keep those things and keep some continuity on how they’re able to get care and take care of their family can bring a lot of peace of mind.

Nick: Yeah, and that’s what we’re really talking about with this benefit — is peace of mind. It’s never perfect, but it does bring a lot of peace of mind to people.

Creditable Years of Service

Nick: And another significant aspect of this benefit that most people, when we talk to them about this, like, can’t believe that this is a thing — the creditable years of service. So if you are approved for this benefit and you’re on this benefit, you’re going to continue to receive creditable years of service like you had been working for the federal government that whole time.

Grant: Yeah, it’s hard for people to understand exactly what that looks like. But when you think about the idea that the average age for someone to call us is in their 40s or 50s, they might receive in the neighborhood of 15 to 20 years of additional federal service onto their existing record without working another day in their life. So that when they turn 62, they get all the benefits added on as if they had just continued working for the federal government all the way up to their original full retirement age.

Nick: Yeah, so significant benefit there. As they get into that regular retirement, what that calculation is going to look like — it’s really going to add on a lot of income into retirement. So that’s something that you really need to be aware of and really think about and consider when you’re looking at this.

Working In The Private Sector

Nick: But let’s get into why we’re really here today — is to talk about working in the private sector. So, you know, that creditable years of service flows directly into this. We’re talking about you being able to go and work in the private sector in a new job, a new career, and still earn income while being on the Disability Retirement benefits. Extremely unique opportunity here.

Grant: It is, and it really does come back to that concept we touched on earlier, which is the concept of occupational disability. The benefit is set up not as an income replacement but as income supplementation. So it’s designed to pay you a portion of your salary to supplement income you’d have somewhere else. And that’s where the opening is to work in the private sector — that you could get a job and earn money and have this benefit paid to you. That’s huge. I’d say 75% of people we talk with are in that category and find something in the private sector to kind of take the next step in their career with.

Nick: Yeah, and that’s — for a disability benefit, that’s kind of unheard of.

Grant: Yeah, it’s certainly unique.

Nick: So what we’re talking about here is you could go work in the private sector and earn up to 80% of your old position’s current salary. Now think about that — that’s a mouthful.

Grant: Yeah, but when you think about that, it’s not just what you’re earning today, it’s what you would be earning if you stayed in that position into the future. So 10 years from now, it’s up to 80% of what that job’s making then, after all the different raises and cost of living adjustments that come with that part of it. So it’s a generous cap, let’s call it that. It certainly allows for you to make a healthy living, and then when you marry that to the benefit, it can become very significant.

Key Point: The 80% cap isn’t based on your old salary frozen in time. It tracks what your former position would be paying today, including all raises and cost-of-living adjustments.

Career Opportunities in the Private Sector

Nick: So we find that our clients that we talk to that can go work in the private sector — there’s a lot of different jobs that they could go do. I’ve heard of people going to be teachers and realtors and stuff like that. I know, Grant, you’ve had a lot of people that you’ve worked with specifically.

Grant: There are so many unique jobs to the federal government that people don’t even do in the private sector. There’s also all kinds of opportunity for people with these unique skill sets. Lots of the law enforcement guys we’ve worked with over the years get a job in consulting for defense contracting companies. They’re not required to carry a firearm and fight bad guys anymore, but their knowledge and training that they got from the government is unique. You can’t go to your local community college and take a course in how to fight drug cartels. That’s something you only learn in one of the governmental law enforcement agencies. So those skill sets are really valuable outside of federal service as well, and especially in a job that maybe isn’t nearly as physically demanding and oftentimes not nearly as stressful either.

So these are some examples we’ve got on the slide here, but this is also an opportunity for you to think about something you’ve always wanted to do but never thought you’d be able to support yourself or your family in in some career. Now if you’ve got 60 or 40 percent of your income made up from this benefit, perhaps this new career that you always thought wasn’t quite lucrative enough can be, because you have an opportunity to earn some money on top of a benefit to kind of make up the whole income and necessary income that you have.

Example: What the Numbers Look Like for One Employee

Nick: So as we see all these different jobs that people could potentially do, let’s bring it all together and look at an example federal employee, just to put some flesh and bone to it so that we can see what all this is going to add up to.

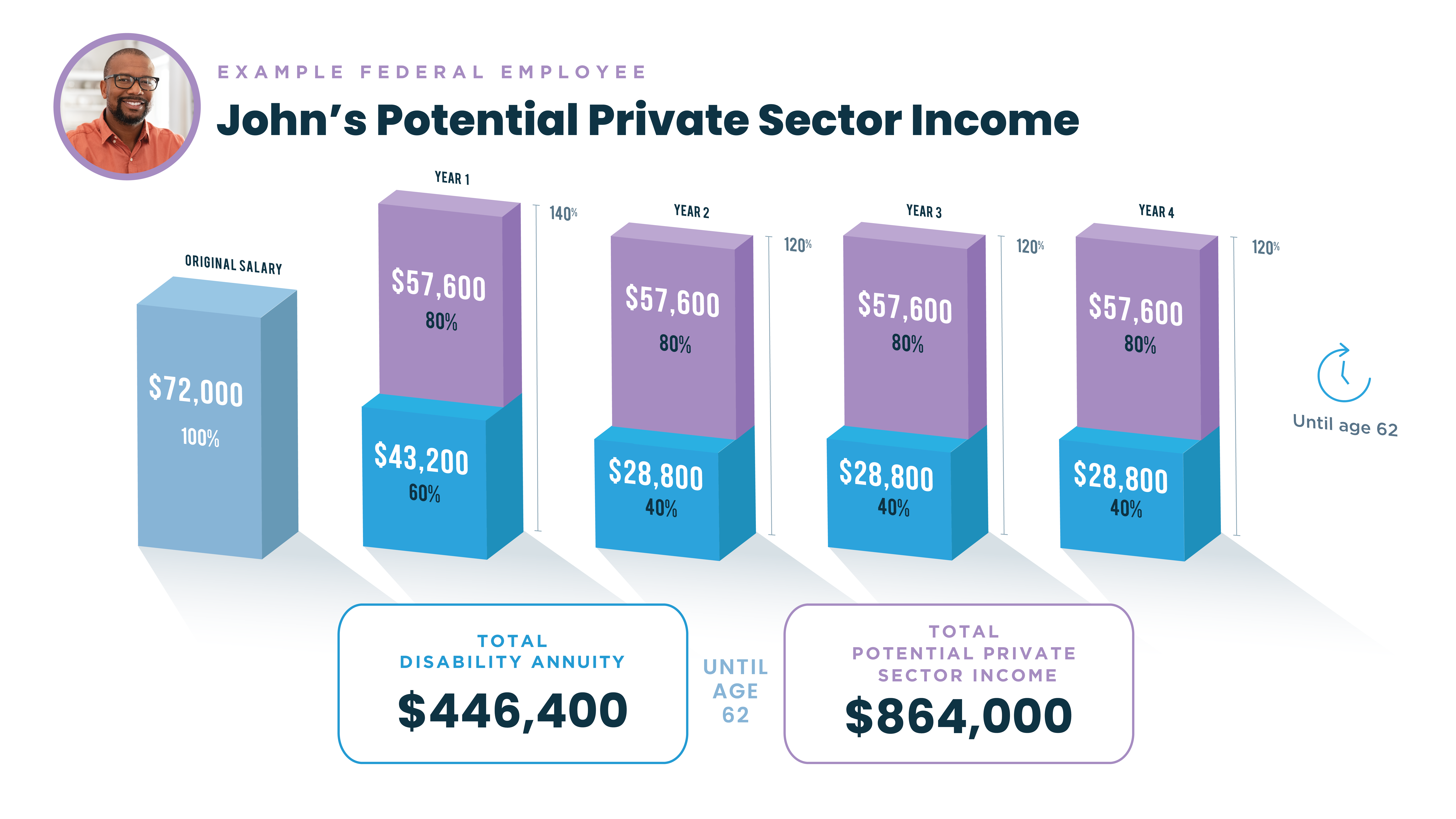

So let’s look at John here. He’s 47 years old. He has a high-three average of $72,000 a year. He’s a letter carrier with the USPS. 15 years of federal service. He’s married and has two children. Now John severely injures his knee in his job while working at the USPS. Now I want to make it clear — John’s injury was caused by his employment, but that’s not necessarily the case for everybody that could apply for Disability Retirement.

Grant: Absolutely not a requirement to have a job-related illness or injury. Could be anything.

Nick: So he undergoes surgery but he’s never able to return to full duty. And what do we mean by full duty there, Grant?

Grant: Yeah, that would be a return to doing all of his normal work and essential functions without any medical restrictions at all.

Nick: Yeah, so what we’re saying is there’s even one part of his job that he’s unable to do. And he’s asked for an accommodation within his medical restrictions with USPS, and they’re unable to meet that accommodation. So, John can get Disability Retirement. Now let’s see what that looks like with his disability annuity and his private sector income.

Private Sector Income: John’s Numbers

Grant: Right, so John’s 47 and with 15 years of service. That’s actually kind of an ideal spot in a lot of situations for this benefit. He’s young enough to be able to get out and get another career started and moving. He’s not close enough to retirement where he’s just trying to make it for a year.

So in this situation, he’d have his original salary of $72,000 a year. During the first year of eligibility for the disability benefit, his retirement pay from FERS would be $43,200. In addition to that, he’d be able to work in the private sector and earn $57,600 on top of that. So that’s a good start, right? That gets him up to $100,800 of potential income during that first year.

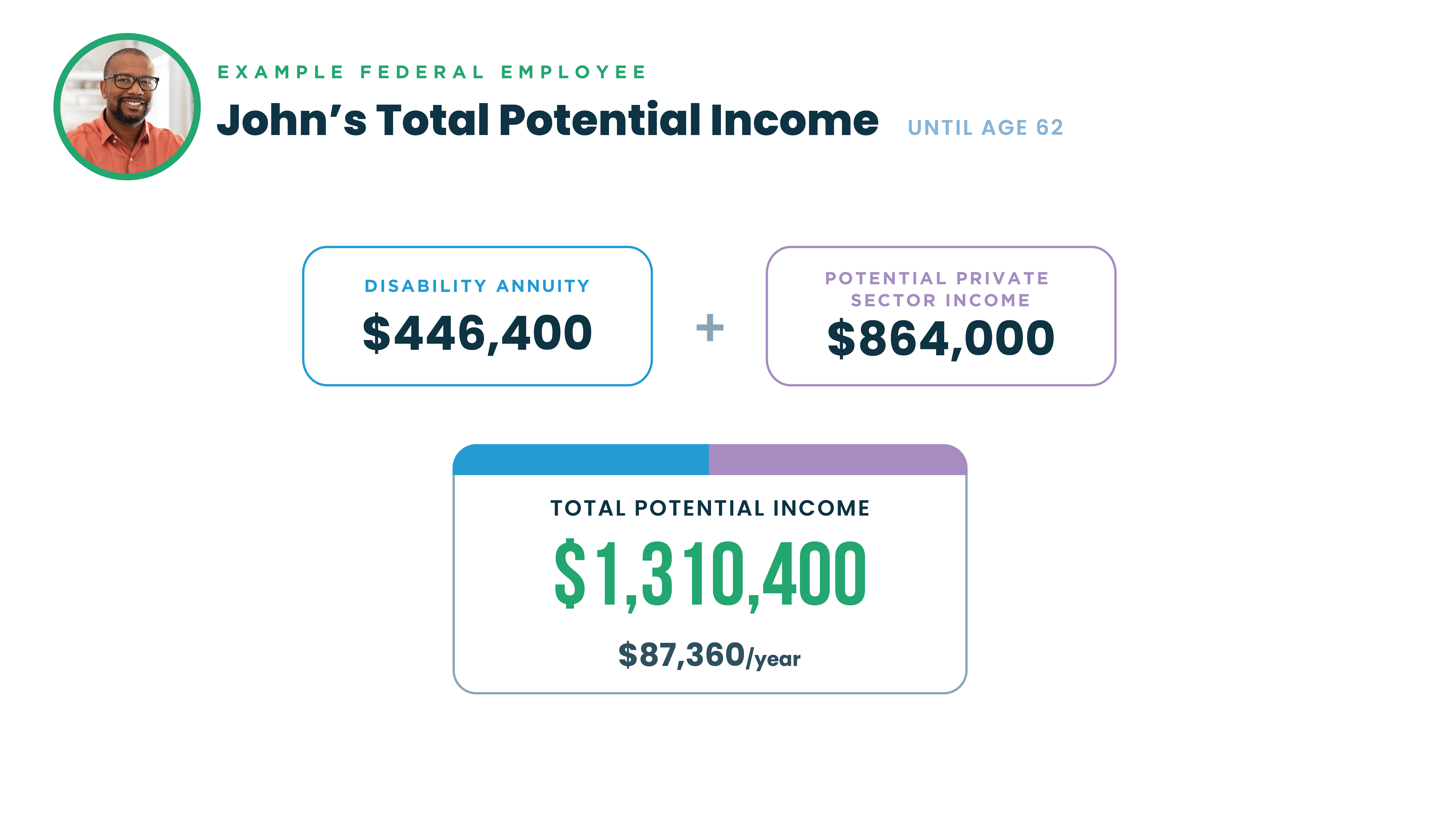

After the first year, he’s still allowed to earn that $57,600 in a private sector position, but the first benefit drops from $43,200 down to $28,800 annually, and it would stay that way for him an additional 14 years until he turned 62 years old. So in that time frame, the disability annuity would have paid him $446,400, and his total private sector income potential is $864,000. And that brings his grand total to over $1.3 million over that 15-year period.

When we look at his potential earnings and benefits combination, you can see it takes him well over his old high-three number from when he worked for the Postal Service.

Nick: And on top of that, Grant, he already has 15 years of federal service, and he’s going to be on this benefit for an additional 15 years. That’ll be creditable years of service. So, when he goes on to regular retirement at 62 years old, it’ll look like he’s worked in the federal government for 30 years, right?

Grant: Which is huge. And the combination of having a career that’s 20 years or longer and retiring at age 62 actually triggers a bonus 10% onto your retirement calculations, and you get that on Federal Disability Retirement on your 62nd birthday. So, in John’s particular situation here, on his 62nd birthday, not only will he have his 30-year career, he’ll have a 10% bonus added on.

Nick: Yeah, so huge potential income here for John. And like I said, I want us all to remember that when we’re talking about this 80% on top of your Federal Disability Retirement annuity — we are talking about potential income. This isn’t guaranteed. You do have to go find a job in the private sector. But as you can see, this is a significant benefit that can really bring you some peace of mind in a really turbulent time in your life.

Reemployment in the Federal Government

Nick: But a couple of things we just want to make sure that we mention here that you do need to be aware of.

Grant: One thing that we get asked a lot is if you can go work at another position in the federal government, and we don’t generally recommend that. It’s highly complex and a little bit silly, but effectively, instead of adding a federal salary to your disability, in this case they actually deduct the disability payments from your new federal salary. So it’s almost never a good idea financially to be re-employed in another position in the federal government. It’s almost always better to be re-employed in the private sector.

In addition to that, this is something else we want to stress. When you get a job in the private sector, you can’t get a job doing the exact same thing the exact same way that you did in the federal government. And that’s because you’ve just proven that you can’t do that job anymore and that there’s some part of that job that you can’t complete. Now, this question gets asked in a variety of formats and people have all kinds of little caveats — but in my situation this and that. It’s true every case is a case-by-case situation. Every person’s situation is a little bit different. But the key to remember is, what part of your job couldn’t you complete, or what restrictions did your medical providers give you that make it impossible for you to continue in that federal job? And if those exist, and exist on a permanent basis, then obviously you need to find a job in the private sector that is not barred by those same restrictions. So if you just look for a situation where you’re not violating your medical restrictions, that should be okay.

Staying Under the 80% Income Cap

Nick: That’s really good to think about. And while we’re talking about these things that you need to be thinking about, here’s just a few more things to consider once you go on to Federal Disability Retirement. We’ve talked about that 80% income cap a lot. So you need to stay under that if you go work in the private sector. If you go over that 80%, you are considered administratively recovered, right?

Grant: That’s right.

Nick: So what you’re saying there is, okay, I can go work in the private sector and find gainful employment — and so you would lose out on your Federal Disability Retirement benefit. And any creditable years of service you had received while you were on the benefit would essentially get wiped away, right?

Grant: That’s right. All of the other benefits will cease. So going over that 80% income cap is not advisable unless you truly have a position that’s going to restore you to full earnings and full benefits and all those things in a private sector job.

Nick: Sometimes we see people that go on to be even more successful in their private sector job, and it’s actually a great thing for them to be administratively recovered because — sure, maybe they’re making double now. We don’t know what that looks like, but there are situations where that’s a really good thing for people.

Grant: Absolutely. We just want to make you aware of it, and that it’s just something to think about.

Key Point: If your private sector earnings exceed 80% of your old position’s current salary, you are “administratively recovered” — you lose the Disability Retirement benefit and any creditable service years you earned while on it.

OPM Income and Medical Reviews

Nick: So another thing that you really need to consider while you’re on Federal Disability Retirement is a couple reviews that the OPM is going to do at different times while you’re on the benefit. The first one’s an income review and then a medical review. So let’s just talk a little bit about the income review and what that entails.

Grant: Well, this is really important, and here’s another question we get all the time. And I want to use this word — it’s in bold here on the slide — you’ll see the words earned income. The 80% cap applies only to income that you earn in some kind of work. If you have income from investments, that doesn’t count against the 80% cap. So this is just about income that you got for your work, for you doing something to earn it.

You can talk to your tax professional about what qualifies. I’ve heard the question a million times: well, what about my rental property, and how does that work? But those really come down to how you take care of those things, and working with your tax professional will get you kind of straightened out pretty quickly on that.

An earned income review really comes every year, just to make sure that you haven’t gone over that earnings cap. Keep in mind, this is not a place to fudge numbers. You’re going to have your information from your employer in your private sector job by then, and man — this is not a place to not be really honest about it. Because not only can you lose the benefit if you do this wrong, you can be in jail if you’re not careful. So this is just a chance for you to report, kind of like doing your taxes, what your earned income was for the previous year. So you’ll get that annually.

Nick: And then at other increments throughout the time that you’re on Federal Disability Retirement, the OPM can request a medical review, right? So this is similar to the income review, but now they’re going to look at those medical restrictions that you’ve been talking about.

Grant: Right, and effectively here you’re not proving again you’ve already proved that you meet the medical requirements. You’re just getting an update from your providers about whether or not you could return to that old federal job, or if the medical condition that you had still exists.

Nick: So we just want you to be aware of these, because they do come up. They’re things that you have to do and take care of, but these are very normal. So if you get them or you hear about them, we don’t want you to be fearful of those at all. Those are normal things that happen. Very rarely are federal employees removed from Federal Disability Retirement after these types of reviews.

Grant: And they can only do this every couple of years, and they have to stop once you turn age 60. So it’s not even guaranteed that it’s every two years — it’s just up to as often as every two years can they ask you for that medical review.

Nick: So all that being said, reviews are very normal and something that you shouldn’t be fearful of.

What If You Can’t Work?

Nick: So what if you can’t work? Let’s get to this part, because I’m sure there are some of you that are listening to this and they’re like, this sounds great, but I can’t work anymore. I have a total disability that leaves me unable to work. So this is a long-term benefit and it’s extremely unique, right Grant?

Grant: Yeah, so the Federal Disability Retirement is considered to be permanent, but it’s not, like I said earlier, designed to be an exclusive benefit to make up all of your income needs if you have to use it. But it does work well with other benefits, whether it’s a VA disability or military retired pay, or if you have a permanent and total disability which extends beyond the occupational disability we discussed earlier, you’re likely eligible to go after a Social Security Disability claim in addition to this benefit.

Nick: So yeah, if you were able to receive both of those — SSDI [Social Security Disability Insurance] and Federal Disability Retirement at the same time — they are going to offset to a certain extent, but essentially you would be receiving a little bit more income over the amount of time that you’re on both of those benefits.

Grant: Absolutely. And this is important, because whenever we’re talking about not having the ability to earn any income, then I want people to be able to get every penny that they’re entitled to because that’s the exclusive way they’re going to get paid. So when you’re approved for both Social Security Disability and Federal Employees Retirement System disability, they work together and you can receive benefits from both. And so the total is more than you’d receive from either benefit by itself, and over the life of a benefit could be significantly more money, along with also receiving those additional creditable years of service and being able to keep those health and life insurance benefits.

And then once you turn 62, it’s significantly more money in the long-term period. Because once you click into that regular retirement calculation, the offset goes away. So that’s another time that’s extremely valuable. Even if you spent 15 years making a little bit more money every month, once you turn 62, it’s going to go up significantly, especially again in a time in your life when the ability to accumulate more income is going down.

Nick: So like we said, this is a benefit that’s really supposed to be supplemental. It’s not perfect — it’s not ever gonna be perfect — but it’s a significant benefit that federal employees have the opportunity to utilize, that is very very different from what a private sector employee would be looking at.

Grant: Yeah, and incredibly beneficial. Again, like you said, there’s no benefit that’s just going to make every worry anyone has go away. But this is a stabilizing force in a time when there’s often a lot of things up in the air, and it allows you to know that you’ve got a baseline that you can’t go below — a safety net.

Nick: Yeah, a safety net. That’s really really powerful.

Final Thoughts and Key Takeaways

Nick: So all that being said, this is what we do every day. This is what we help people walk through every day. If you’re applying for this benefit or looking at this benefit, you’re in a situation that you never thought you’d be in. We know people aren’t necessarily looking forward to trying to get on this, but we hope that you can see that there’s some hope — that there is a future, that you can find some security with this benefit, and something that you’ve worked really hard for.

So when we talk about that future, we always tell people to not risk that future. There is a significant amount of money on the line, like we talked about when we looked at that example employee. A significant amount that we don’t want you to put up in the air without going about applying for it the correct way.

So, a couple key takeaways from this that we just want you to remember. This is a benefit that you have in your current FERS package that you can utilize if you’re unable to work in your position due to a disability or injury or illness that’s keeping you from working.

With that, this benefit’s going to offer you some monthly income in the form of an annuity. You’re going to be able to maintain that health and life insurance that so many people are worried about and thinking about — you’re going to be able to maintain what you currently have.

And what today was all about was talking about working in the private sector. If you have the capacity to go work and still make an income in a different position, you have the ability to go do that. And hopefully you could see how big of an impact that could have on your income and kind of building that on top of this Disability Retirement annuity.

We want you to remember that the OPM is going to ask for some reviews of your income and your medical restrictions, and those are normal. Those aren’t something that you have to worry about. And then remember, like we said, if you can’t continue working, that’s understandable, and there’s a lot of people that can’t. This might not feel like the perfect benefit for you, but like we said, it is a benefit, it is a very unique one, and can really help you get through a really tough period of your life.

I’m really glad that you guys got to hear from Grant today. Hopefully you could hear his expertise and experience with all of this information. So, thanks for doing this, Grant.

Grant: Happy to do it. Thanks for having me, Nick.

If you would like to talk with someone about what Disability Retirement might look like for you, give us a call today for a free consulation.