Quick Takeaways

- Interim payments start immediately upon approval: You’ll receive approximately 80% of your calculated annuity while OPM finalizes your benefits, which typically takes about 5 months.

- Back pay dates to your last paycheck: Any time you weren’t receiving income from your agency or workers’ compensation qualifies for back pay—but accepting even one day of paid work resets this date permanently.

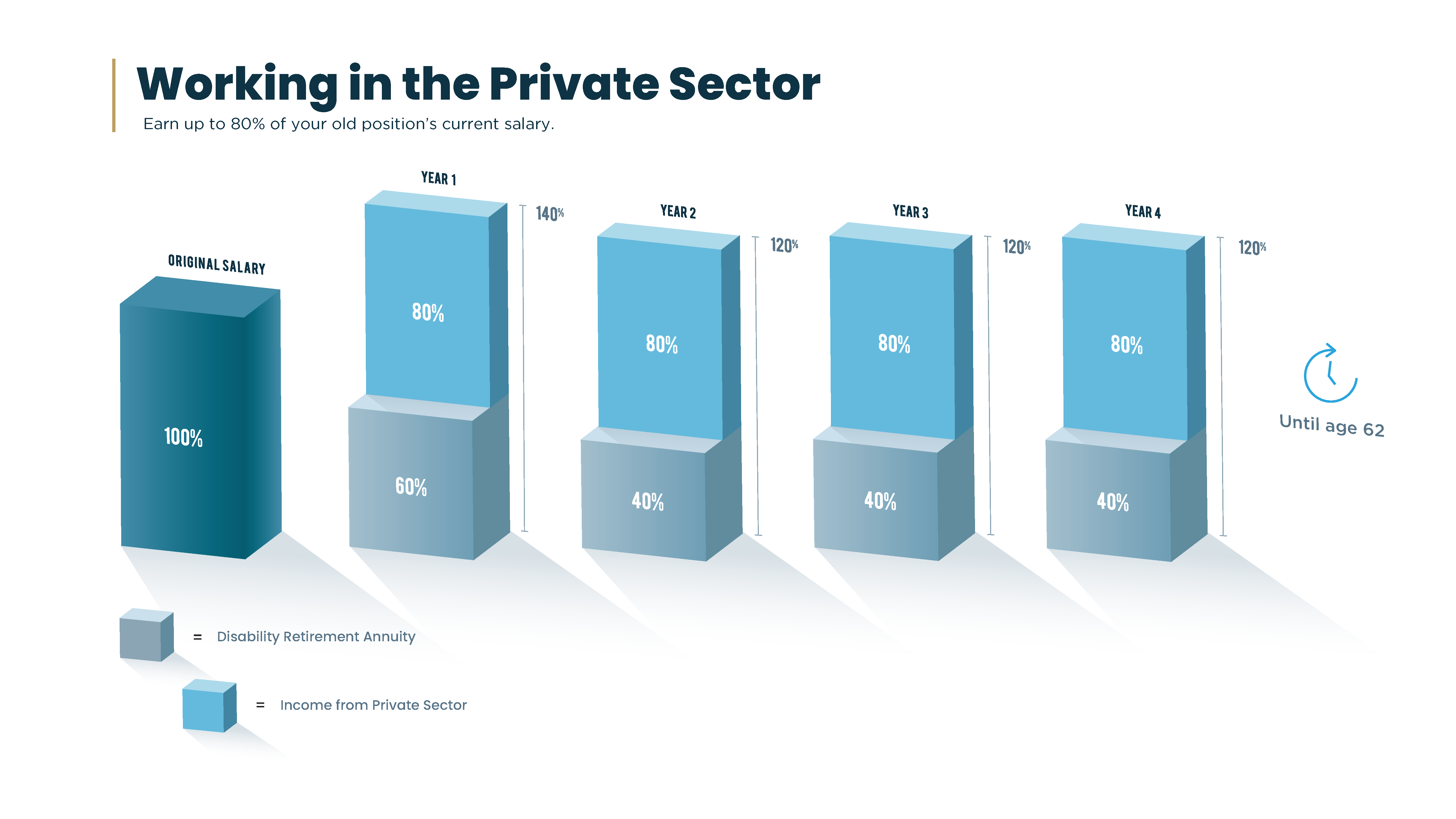

- First year on Disability Retirement pays 60%, remaining years pay 40%: Your annuity is 60% of your high-three salary in year one, then drops to 40% until age 62 when it recalculates as regular retirement.

- You can work while receiving benefits: The 80% earnings cap means you can make up to 80% of what your former position currently pays, potentially earning more total income than before.

- Overpayments are your responsibility to repay: If Social Security or other benefits aren’t properly offset, you may end up being overpaid—save part of your back pay as protection.

Common Questions

Q: When do I start receiving money after my Federal Disability Retirement is approved?

A: Immediately upon approval, you enter interim status and begin receiving interim payments representing about 80% of your calculated annuity. This continues for approximately 5 months while OPM finalizes all calculations.

Q: What is back pay and how much will I receive?

A: Back pay is a lump sum payment covering any period you weren’t receiving income from your agency or workers’ compensation. The amount depends on the time between your last date of pay and your approval date, calculated at your annuity rate.

Q: Can my agency reset my back pay date?

A: Yes—and this is critical. If your agency puts you on paid status for even a single meeting after you’ve stopped working, your last date of pay resets immediately. You’ll lose all accumulated back pay time, and there’s no way to recover it.

Q: How much can I earn if I work while on Federal Disability Retirement?

A: You can earn up to 80% of what your previous federal position currently pays. This is combined income from all sources, and because you’re also receiving your annuity, you may actually earn more total income than you did working full-time.

Q: What happens to my benefits at age 62?

A: Your Disability Retirement benefit recalculates into regular retirement annuity as if you’d been working the entire time. All years on Disability Retirement count as creditable service years, often qualifying you for the enhanced annuity calculation in retirement.

Full Webinar Transcript

Ashley Withers: Today we’re going to be talking about back pay and interim payments in regard to Federal Disability Retirement. We’re going to cover where this benefit comes from, how much money it pays out to those who are approved, benefit highlights, interim payments, back pay, overpayments, and we’ll get into financial planning.

Understanding Federal Disability Retirement

Ashley: Anna, can you give us an overview of what Federal Disability Retirement is?

Anna Barnes: Sure, and I’m going to start with who this benefit helps. It’s specifically designed for federal employees who are struggling to do their job because of an illness or injury. This is for a federal employee who has a medical condition that’s expected to persist for more than one year, and that prevents them from performing the essential duties of their position.

Ashley: When federal employees are applying for Disability Retirement, what is the government entity that this is through?

Anna: The Office of Personnel Management [OPM] is the agency that will adjudicate their Disability Retirement claim as well as pay out the benefits. This is a benefit that’s already built into the retirement system. You pay for it as a FERS employee—it comes out of your paycheck each week. You pay into FERS, and so you have these benefits available to you outside of just a regular retirement benefit.

Monthly Annuity and Income Benefits

Ashley: Let’s break down the highlights of this benefit. Can you give us a picture of what this benefit looks like in regard to income?

Anna: Absolutely. The first year that you’re on Disability Retirement, you’re going to receive 60% of your high-three salary, and then each year after that until you turn 62, you’ll receive 40% of your high-three salary. It’s important to note that this is taxable income, so it is subject to federal income tax and state income tax depending on your state. You’ll also have a choice to keep your life insurance benefits, your health insurance benefits, and you can make an election for a surviving spouse.

Key Point: Your “high-three average salary” is not just your yearly salary—it’s an average of your highest 36 consecutive months of basic pay, calculated by OPM at the time of approval.

Ashley: How long does this benefit last for federal employees?

Anna: If you’ve been in our webinars before, you’ll probably have heard this term “a bridge to 62.” We like to call it that because the Disability Retirement annuity will pay you until you turn 62, at which point it’s going to recalculate into a regular retirement annuity as if you had continued working for the federal government the entire time.

Working While Receiving Disability Retirement

Ashley: There is another pro to the Federal Disability Retirement benefit, which is that you are still able to continue working while receiving this. Can you give us the parameters of working while on Disability Retirement?

Anna: Sure. When you’re on Disability Retirement, it’s considered to be an occupational disability, not a total disability. So, you are able to go out and work in the private sector, and we’ve seen people go on to become teachers, realtors, start their own business—there are a lot of different options out there.

The limit on what you can make in the private sector is going to be 80% of what your previous position is currently paying. And it’s really interesting because you have the potential here to actually make more money than you were just working in your federal position.

Creditable Years of Service

Ashley: Another thing that we want to talk about for Disability Retirement annuitants is the creditable years of service. Can you give us some information on this?

Anna: Like I said, when your benefit recalculates at age 62, it’s going to include all of the years you spent receiving Disability Retirement because those years count as creditable years of service. So those get added to any pre-existing creditable years of service you had before going on the benefit.

Ashley: And this is for when annuitants are calculating their regular retirement?

Anna: That’s correct. They’ll use the regular retirement calculation, and they’ll just include all of their creditable years of service—the ones they actually worked plus the ones they got for being on Disability Retirement.

Example: If a federal employee went out on Disability Retirement at age 40 after working 10 years, by the time they turn 62, they will have accrued 32 years of federal service. They’ll get that additional 22 years of creditable service while they’re on Disability Retirement.

Anna: This is going to dramatically change their retirement calculation because instead of receiving 1% for each year of creditable service, they’re now eligible to receive the 1.1% calculation on their creditable service.

Ashley: Anna, that can be so important for so many federal employees—that percentage can make such a big difference when they are planning what they’ll receive over the years in their regular retirement.

Maintaining Health and Life Insurance

Ashley: In addition to the income that federal employees can receive on Disability Retirement, there’s also an option to maintain health and life insurance. Can you talk about what that looks like?

Anna: Absolutely. If you carried health and life insurance as a federal employee and you’re approved for Disability Retirement, you can continue those benefits in retirement. The health insurance premiums that your agency was paying will move to OPM, and then you’ll continue paying the same premiums that you’ve been paying. Your life insurance premiums will stay the same, but those do tend to go up as you get older.

Ashley: And another really important aspect of these insurance benefits is that employees’ families are able to stay under their insurance, correct?

Anna: That is absolutely correct. You can have a spouse and dependents on your health insurance benefits, and then you can designate your beneficiaries for your life insurance benefits.

Understanding Interim Payments

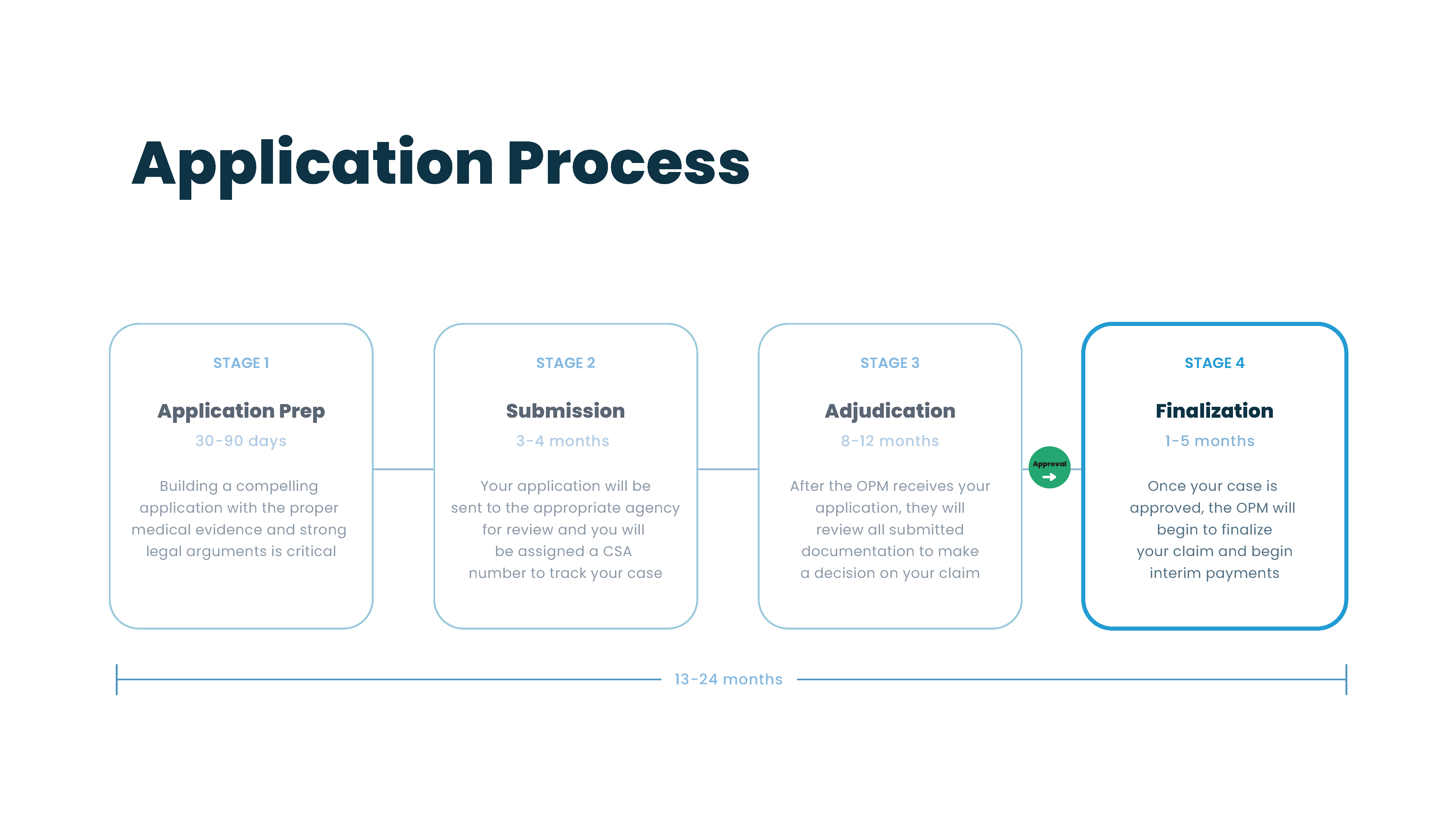

Ashley: Let’s get into understanding interim payments—when you get to the approved process, what it looks like for how much you’ll be receiving, when you’ll actually be receiving that money, and all the things that you’ll be dealing with with OPM.

Our office walks our clients through the application process from start to finish. We work on building an application, get all the proper medical evidence together, submit those applications, deal with the federal agencies, and work with OPM as they start that adjudication process. Anna, once a client is approved for Federal Disability benefits, can you talk about when those benefits start to come in?

Anna: Absolutely. Upon approval for Disability Retirement, you go into what OPM calls interim status, and all this means is that they’re working out exactly what your benefit is going to look like—they’re calculating everything down to the penny. But they don’t want you to go without income for that entire time, right? So, they will begin paying you what they call interim payments.

Key Point: Interim payments represent about 80% of what your annuity is going to be, just so you have some type of income while you’re waiting for OPM to finalize the benefit. Interim payments are only subject to federal income tax—nothing else comes out of interim payments.

Ashley: Once the interim payments process is complete and they’ve actually finalized those benefits, OPM just will make up the difference in that first payment?

Anna: You’re exactly right. If they underpaid you during the interim status, they will make up the difference for that. It’s important to keep in mind that this process can take about 5 months, and that can be longer or shorter depending on OPM’s backlog, but what we’ve been seeing recently is right around the five-month mark.

Back Pay Explained

Ashley: Something else that federal employees may be eligible for is back pay. Can you talk about what back pay is and at what point in this finalization process that back pay comes in for an employee?

Anna: Back pay is going to be a lump sum payment that is paid once you’ve been approved, and that pay is for time that you were not receiving any pay from your agency or workers’ compensation. Back pay is going to be dated to your last date in pay status, so any income you receive from your agency or wage loss payments from workers’ compensation count as pay in this situation.

Ashley: This is something that federal agencies and OPM work together on?

Anna: That’s exactly right. Your employing agency will provide OPM with your last date of pay, and from there OPM will determine how much back pay you’re going to be owed.

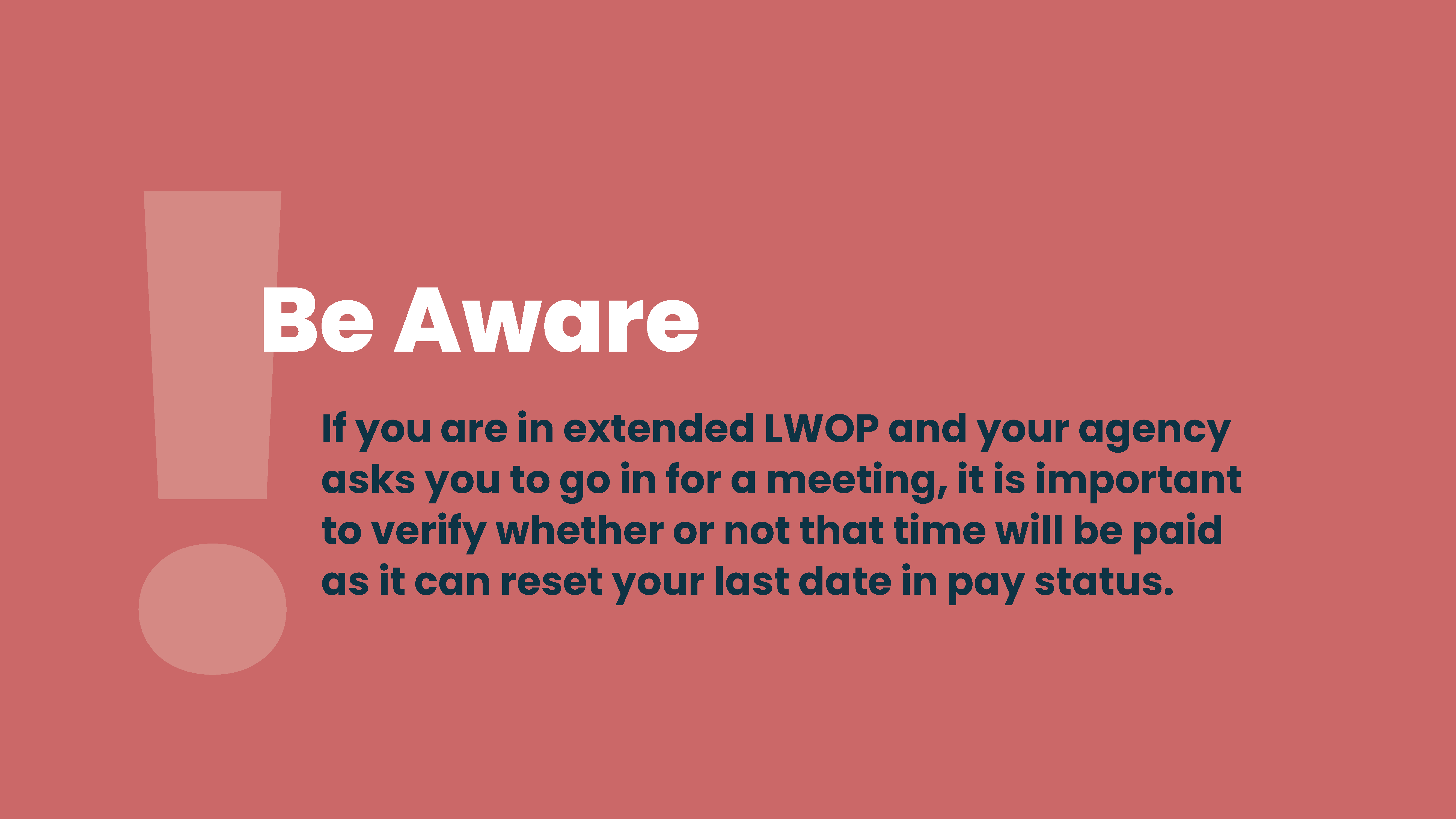

Critical Warning About Last Date of Pay

Ashley: Something that we really want our clients to be aware of is that when you are in an extended leave of absence from your agency and you have not been receiving any kind of income, verify with your agency at any point if they ask you to come in for a meeting—whatever it may be—that you will not be put on a paid status, as that can reset your last date of pay.

Common Mistake: If you’ve been off work for four months and your agency asks you to come in for a meeting and they put you on the clock, you will lose those four months of back pay.

Anna: That’s exactly right. It’s really important to know this information. We’ve seen a lot of people who have been put in unfortunate circumstances because they lose months and months of backpay because they didn’t realize that they were going essentially on the rolls with the agency again.

Ashley: Anna, there’s no way to get that lost money back, correct?

Anna: That’s correct. Once your agency has paid you, your last date of pay is automatically reset. It’s an automated issue, and they will report that date to OPM, and there’s very little to nothing that can be done to change it.

Using Back Pay Wisely

Ashley: There are a lot of things that back pay can be beneficial for. Can you give just a couple highlights of what we typically see federal employees use this money for?

Anna: Yeah, definitely. The biggest thing that we see is just financial assistance in general. Many of our clients have been out of work for a long time, and so they’ve really been struggling to keep up with their finances. This back pay can be a lifeline for them to help them get caught up on different things that they may be behind on—bill payments that they’ve accrued, either medical bills or credit card bills that they’ve racked up while they’ve been waiting for this decision. Back pay can be really, really critical for a lot of our clients.

Ashley: And this is one lump sum payment that comes in the first month of the finalized benefit that they receive?

Anna: That’s exactly correct.

Understanding Overpayments

Ashley: Also, something that we want our clients just to be aware of is that there is such a thing as overpayment. This typically comes from OPM overpaying you for benefits that were not offset correctly. It can also happen with workers’ compensation benefits or just issues with dates provided from the agency to OPM. Can you give us a little bit more information on overpayments?

Anna: Absolutely. One of the most common times we see an overpayment situation is with a Social Security disability benefit that hasn’t been offset properly, just like you said. It is really important to be aware that you, as the annuitant, you are the one who is responsible for paying back this overpayment.

Critical Warning: OPM, Social Security, and workers’ compensation—whoever the overpayment is with—they are not willing to work with people on overpayment. If you’ve been overpaid, it’s going to be your responsibility to pay it back.

Anna: Which is why we really recommend that our clients put aside a portion of their back pay, or if you feel like your annuity is too high, to look into it, because there’s a good chance that that might actually be the case. You don’t want to be put in a situation where you owe thousands of dollars back to the federal government.

Ashley: Because also sometimes it can take them several months to figure out that error, correct?

Anna: That’s correct, and we’ve seen it time and time again that somebody did not know that they were being overpaid for months on end, and then one day they got a bill for thousands of dollars that they’re just expected to pay back.

Ashley: This is why you need to make sure that OPM is aware and up to date on all the information of the benefits that you’re currently receiving, so when they’re finalizing those benefits they have all the correct information and can hopefully prevent any kind of overpayment.

Anna: That’s exactly right.

Creating a Strong Financial Plan

Ashley: There are multiple things that come into play when you are creating a strong financial plan for the future. Anna, can you just kind of touch on these points?

Anna: Absolutely. There are a lot of things outside of your annuity payment that you want to consider as you’re coming up with this financial plan.

Key Financial Planning Considerations:

- Thrift Savings Plan (TSP): Your TSP is another aspect of your retirement plan, so it’s really important to learn what you can do with your TSP upon retirement. It’s really beneficial to probably look into some private sector financial products—you know, what are the best options for you? Everybody’s different and unique, so looking into these private sector products can be a really big help.

- Social Security Benefits: You can contact Social Security to get a breakdown of what your payments will look like depending on when you elect to start receiving those. That’s something that you should look into and share with a financial planner.

- Managing Your Back Pay: This is really important. With the overpayments, you want to make sure that in the event that there’s an overpayment you don’t know about, you’re covered on being able to pay that back and leveraging that back pay to the best of your ability after going through the Disability Retirement process.

Ashley: Typically, we really recommend speaking with an experienced financial advisor when you’re trying to piece together all the different benefits that you may be receiving and the benefits that may be coming into play later and how those can offset or benefit one another.

Anna: That is really great advice, Ashley. We really, really highly encourage you to talk with an experienced advisor, as there are so many moving parts to not only this benefit but other benefits that you’re entitled to down the road.

Summary of Key Points

Ashley: Just to summarize what we’ve talked about today:

-

- Federal Disability Retirement benefits come through OPM

- They pay out 60% of your high-three salary the first year and 40% every year after

- You start to receive interim payments following approval while OPM is finalizing those benefits

- Upon finalization, OPM will pay you out one lump sum of back pay based on your last date of income with your agency or workers’ compensation benefits

- We talked about overpayment and the things that you need to be looking out for in regard to benefit offsets

- We touched on financial planning and all of the ways that you can prepare for your future and all the benefits that you may be entitled to

Anna: That’s exactly right. Thank you so much, Ashley. I think we went over a lot of really good information, and again I want to stress that there are so many pieces to this that speaking with a financial advisor is going to be in your best interest for sure.

Ashley: Absolutely, Anna. Thank you so much for joining us and thank you for all of this beneficial information that you went over with us today.

Anna: Thank you, Ashley. It’s been a pleasure to be able to share this information with federal employees who might need some guidance.