Quick Takeaways

- Your annuity is structured in two phases: You receive 60% of your high-3 average salary in year one, then 40% every year after until age 62.

- You can work while receiving Federal Disability Retirement: Earn up to 80% of your current federal position’s salary in the private sector while collecting your annuity.

- You must apply for Social Security Disability: The OPM requires you to apply for SSDI, but approval isn’t necessary—it’s just a checkbox requirement.

- Your TSP stays yours with three options: Leave it to collect interest, roll it over, or cash it out (though early withdrawal may have penalties).

- Reasonable accommodation requests are mandatory: You must exhaust all reasonable accommodation efforts with your agency before applying for Disability Retirement.

Common Questions

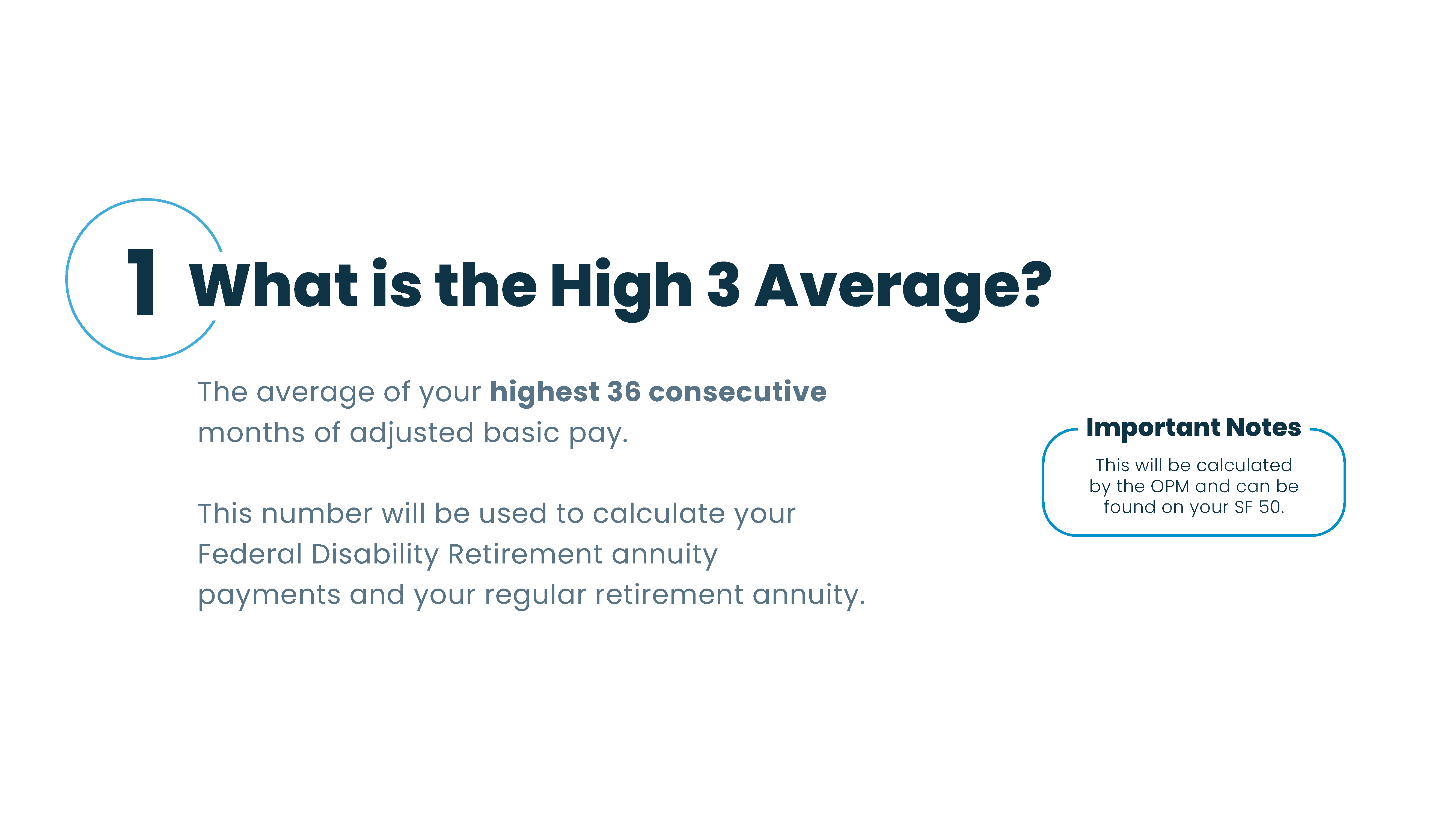

Q: What exactly is my high-3 average?

A: Your high-3 average is the average of your highest 36 consecutive months of adjusted basic pay. The OPM calculates this, but you can also find it on your SF-50 form.

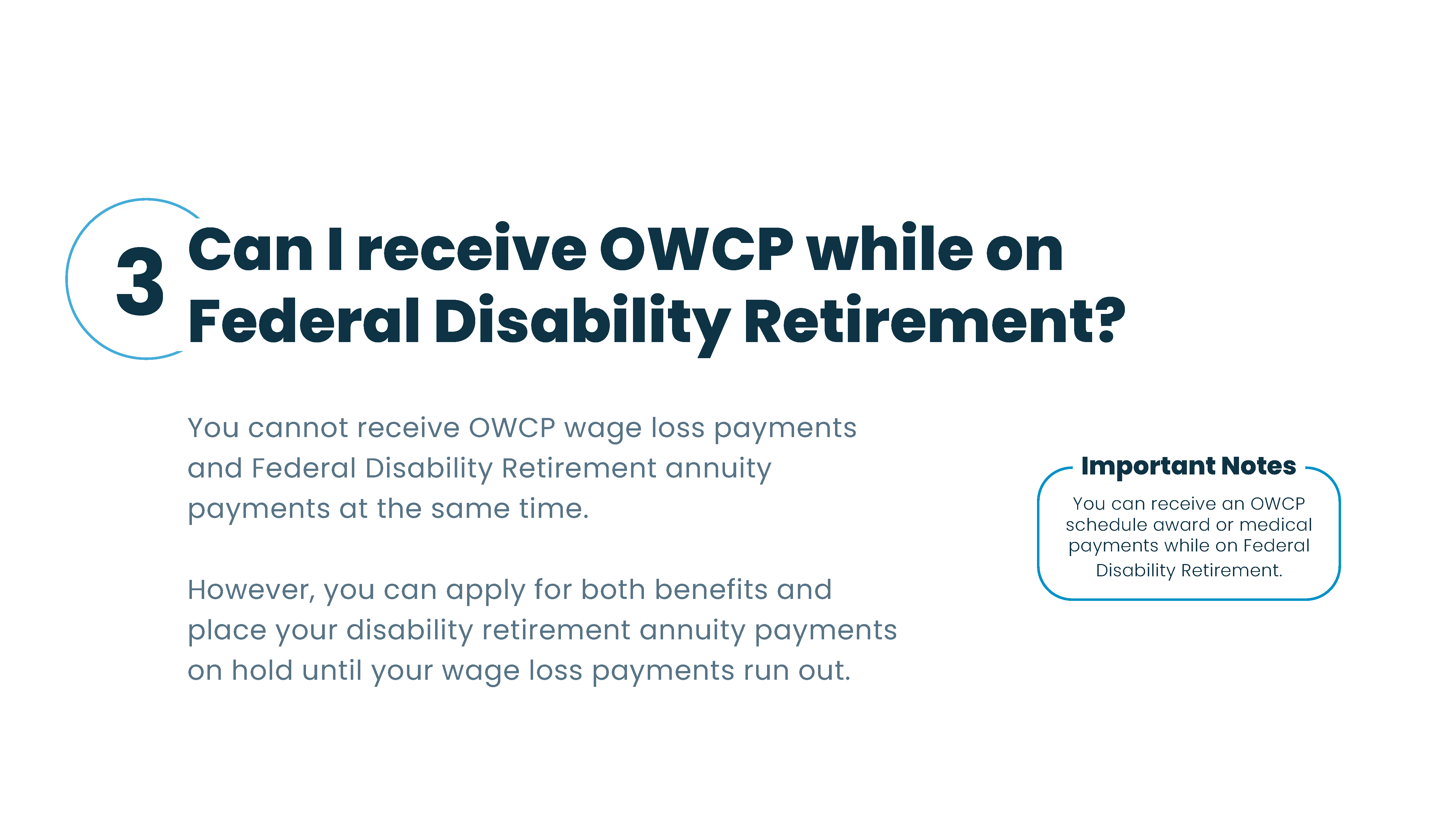

Q: Can I receive workers’ compensation (OWCP) and Federal Disability Retirement at the same time?

A: No, you cannot receive OWCP wage loss payments and Federal Disability Retirement simultaneously. However, you can apply for both and place your Disability Retirement on hold until your wage loss runs out. You can receive schedule awards or medical payments while on Disability Retirement.

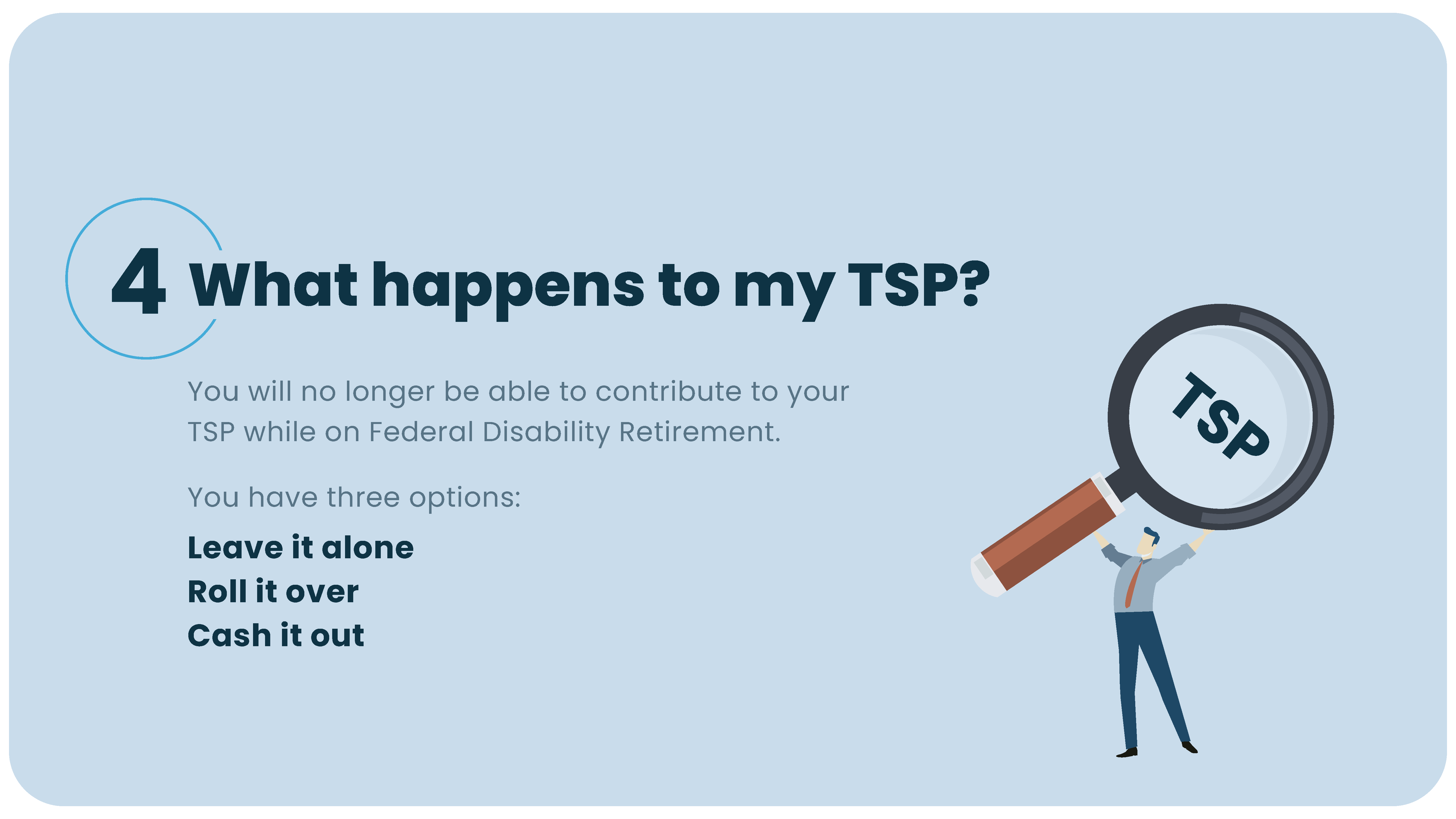

Q: What happens to my TSP when I go on Federal Disability Retirement?

A: You can no longer contribute to your TSP while on this benefit. You have three options: leave it alone to collect interest, roll it over, or cash it out. Contact a financial advisor about potential fees and penalties based on your age.

Q: What counts toward the 80% income cap when working in the private sector?

A: Only earned income from wages in exchange for goods and services counts toward the 80% cap. Passive income does not count, which is why it’s recommended to speak with a CPA about your specific earnings situation.

Q: What happens if my application is denied?

A: You can submit an appeal for reconsideration within 30 days of your denial letter. Additional medical evidence and documentation can strengthen your claim. If denied again after reconsideration, you’ll request an appeal and meet with the MSPB [Merit Systems Protection Board] in a hearing.

Full Webinar Transcript

Understanding Federal Disability Retirement as a Benefit

Hannah Spahn (Client Experience Specialist): We’re going to be talking about the top 10 Federal Disability Retirement questions. Today in this webinar we’re going to go over what is Federal Disability Retirement, provide a brief benefit overview, discuss your high-3 average, your TSP and what happens to it while on Federal Disability Retirement, and then we’re going to talk about requesting reasonable accommodations.

First, we’re going to talk about understanding Federal Disability Retirement—what it is and what it can do for you. Kyleigh, can you tell us a little bit more about this benefit?

Kyleigh Adams (Senior Disability Consultant): Of course, Hannah. Federal Disability Retirement is a benefit that is made specifically for federal employees who pay into the Federal Employee Retirement System. The OPM [Office of Personnel Management] requires that you have 18 months of credible service, and they’re the ones that ultimately decide if you are approved or denied for this benefit.

The Four Main Benefits

Hannah: Federal Disability Retirement provides four main benefits. You’re going to receive a monthly annuity, credible years of service until age 62, the ability to work in the private sector, and the option to maintain your health and life insurance.

Now everyone always asks how much am I going to receive. On Federal Disability Retirement, the first year you’re going to be receiving 60% of your high-3 average, and every year after you’re going to receive 40% of your high-3 average.

Kyleigh: You’re exactly right, Hannah. Keep in mind that this benefit is also taxable income.

How the Annuity Structure Works

Kyleigh: If you take a look at our visual representation, you have a pile of coins representing your high-3 average. Moving on to year one, you’re going to be receiving 60% of your high-3, and then the years following until you are age 62, you’ll be receiving 40% of your high-3 salary.

Hannah: This is a secure monthly annuity that you’re going to be receiving until age 62. But during this time you also have the option to work in the private sector and earn additional money.

Working While on Disability Retirement

Hannah: For Federal Disability Retirement, you’re just proving that you have an occupational disability, not necessarily a total disability. So, this allows you to find a new job in the private sector that falls within your medical restrictions.

Kyleigh: Exactly, Hannah. You can earn up to 80% of your old position’s current salary as long as it is within your medical restrictions. You could be a delivery driver, an attorney, a teacher, a realtor—the options are limitless.

Hannah: Looking at a visual representation of your private sector work, you can earn up to 80% of your old position’s current salary. As you can see, the coins represent your Disability annuity that you can receive on top of your 80% in the private sector. The combination of both of these benefits will equal more than you were originally receiving in your old job.

Accruing Service Time Without Working

Kyleigh: On the topic of working while you are receiving Federal Disability Retirement, you are still accruing creditable years of service into your regular retirement. This is something that you will really want to pay attention to whenever you are deciding if this is an option that you want to pursue.

For instance, if you were to medically retire at age 42, you would be accruing an additional 20 years into your regular retirement without working for the federal government. This results in an excellent pension once you turn 62.

Health and Life Insurance Benefits

Hannah: Another great benefit to Federal Disability Retirement is the ability to maintain your health and life insurance. This can make a huge difference to federal employees covering the cost of their medical condition.

Top 10 Questions About Federal Disability Retirement

Question 1: What Is the High-3 Average?

Hannah: We mentioned this earlier when talking about calculating your Federal Disability Retirement annuity, but your high-3 average is going to be the average of your highest 36 consecutive months of adjusted basic pay. This number will be calculated by the OPM, but it can also be found on your SF-50.

Kyleigh: Exactly, Hannah. Knowing your high-3 average is super important before you get started with this whole process.

Question 2: Do You Have to Be Approved for SSDI to Qualify?

Kyleigh: Do you have to be approved for Social Security Disability to qualify for Federal Disability Retirement? Short answer is no, you do not have to be approved. However, the OPM does require that you apply for this benefit. It does not matter if you are approved or denied—it’s just a box that we have to check to make sure that we meet all of the requirements set in place by the OPM.

Common Misconception: Many federal employees think they must be approved for SSDI before applying for Federal Disability Retirement. This is not true—you only need to apply for SSDI, not receive approval.

If you are approved for Social Security Disability and you are approved for Federal Disability Retirement, there is an offset to the amount of money that you would receive. This is something that we can discuss during your consultation.

Question 3: Can I Receive OWCP While on Federal Disability Retirement?

Hannah: Can I receive OWCP workers’ compensation while on Federal Disability Retirement? You cannot receive OWCP wage loss payments and Federal Disability Retirement at the same time. However, you can apply for both benefits and place your Disability Retirement on hold until your wage loss runs out.

OWCP wage loss is typically more of a short-term benefit, while Federal Disability Retirement is long-term, so we want you to maximize your retirement as much as possible.

Kyleigh: Exactly. You can receive a schedule award or any medical payments while on Federal Disability Retirement, though.

Question 4: What Happens to My TSP?

Hannah: What happens to my TSP? This is one of the biggest changes to your benefits. While you are receiving Federal Disability Retirement, you are no longer able to contribute to your TSP while you are on this benefit.

With your TSP, you have three options:

-

- Leave it alone and let it collect interest

- Roll it over

- Cash it out

It is important to note that if you do cash it out, there are fees and penalties that you may have to pay according to your age. That’s why we suggest you contact a financial advisor to get the best advice for your current situation.

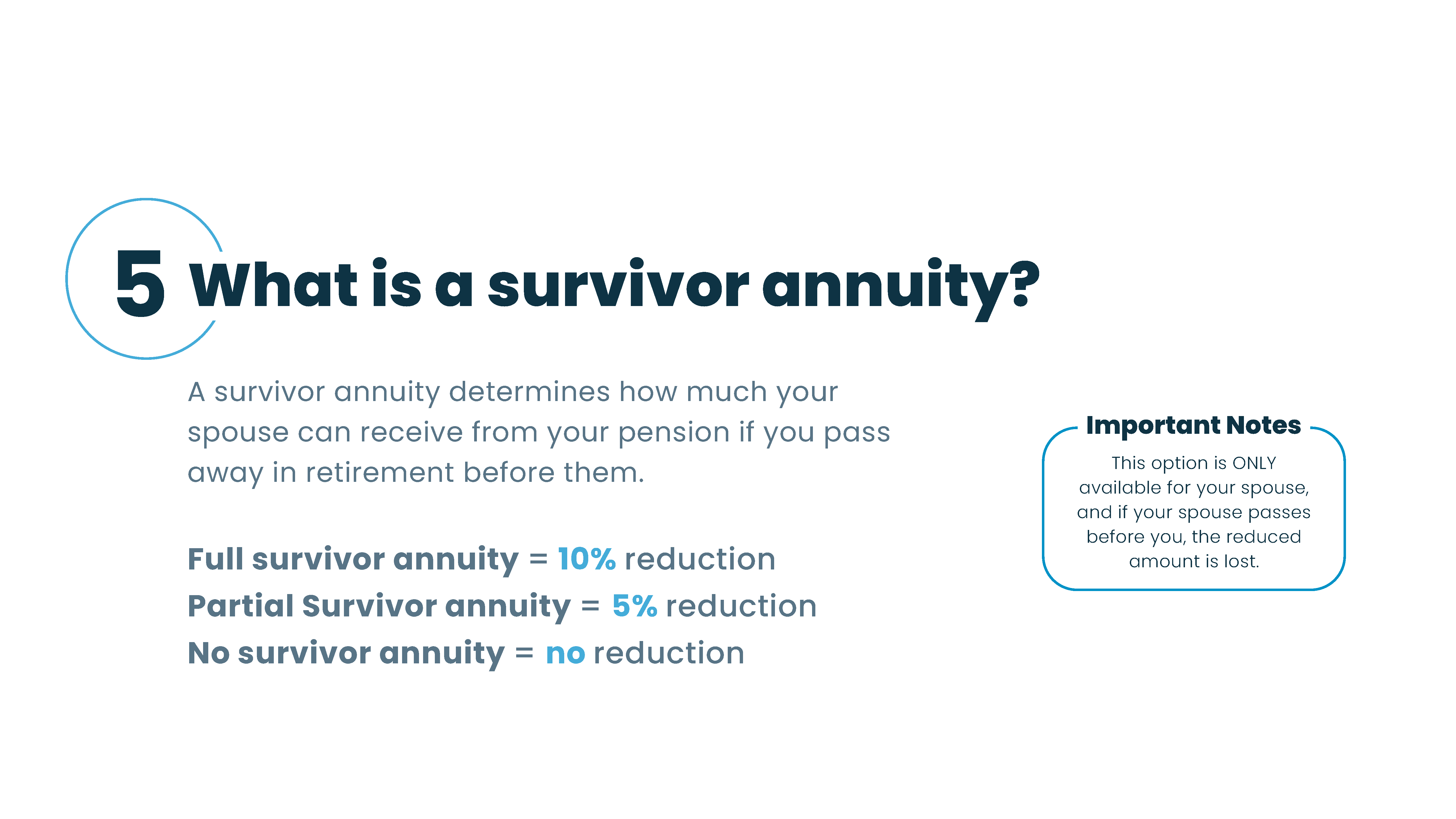

Question 5: What Is a Survivor Annuity?

Hannah: A Survivor annuity determines how much your spouse can receive from your pension if you pass away in retirement before them.

-

- If you elect a full Survivor annuity, your annuity will be reduced by 10%

- If you elect a partial Survivor annuity, your annuity will be reduced by 5%

- If you do not elect a Survivor annuity, your annuity will not be reduced and your spouse will not receive any benefit

Keep in mind, in order to elect a partial Survivor annuity or no Survivor annuity, your spouse is going to have to sign a waiver.

Kyleigh: It’s also important to note that this option is only available for your spouse, and if your spouse does pass before you, the reduced amount is lost.

Question 6: Can I Work After I Retire?

Kyleigh: Can I work after I retire? The answer is yes, you can. That’s one of the best things about being on Federal Disability Retirement—you’re able to work in the private sector while you’re receiving your annuity payments, as long as you are not earning more than 80% of your old position’s current salary and you are working within your medical restrictions.

Hannah: However, it is not recommended to return to work in the federal government, as it can affect your annuity.

Kyleigh: I’ve spoken with a lot of clients in the past and they have found their new passion and they’ve started a new chapter in their life. I actually spoke with a client a few months ago and they told me they were going to pursue their passion in zookeeping. So, the options are truly limitless.

Question 7: What Is Counted Toward the 80% Income Cap?

Hannah: What is counted toward this 80% income cap? Only earned income counts toward this 80% income cap while working on Federal Disability Retirement. This is any income earned from wages in exchange for goods and services.

This does not, however, include passive income, which is why it’s recommended to speak with a CPA to learn more about your earnings.

Question 8: What If I Am Denied?

Kyleigh: What happens if I am denied? This happens sometimes, and it’s a process that we are familiar with. We have a whole team at our firm that just works on appeals.

If you are denied, you can submit an appeal for reconsideration within the first 30 days of your denial letter. From there, we can submit additional medical evidence and further documentation to strengthen your claim.

If you are denied after your reconsideration, you will have to request an appeal and meet with the MSPB in a hearing with our attorney.

Hannah: While it’s not a requirement, it is highly recommended to have legal representation at the denial stage, as there’s going to be a lot of legal jargon and processes that are difficult to go through alone.

Question 9: Can My Benefit Be Taken Away?

Hannah: A lot of our clients are worried if their benefit can be taken away. Kyleigh, can it?

Kyleigh: It actually can be taken away. The OPM will perform annual income and medical reviews to make sure that you are still qualified for this benefit.

Hannah: To help ensure that you do not lose your annuity, it’s important to stay under the income cap and continue seeking treatment with a medical professional.

We often recommend seeking treatment every six months just to keep up communications. Reviews by the OPM are completely normal, and it’s rare to lose your benefit during an annual review.

Question 10: Do You Have to Request a Reasonable Accommodation?

Kyleigh: One of the requirements for Federal Disability Retirement is requesting reasonable accommodation at your federal workplace. You must exhaust all reasonable accommodation efforts with your agency before applying for Disability Retirement.

Hannah: If you are separated before you can request an accommodation, you will then have to prove that there is no accommodation that would allow you to fully perform your job. This is often a difficult task, which is why it’s recommended to request reasonable accommodations as soon as possible.

Kyleigh: If you have already exhausted all reasonable accommodation efforts, then Federal Disability Retirement may be your next logical step.

Final Recap

Kyleigh: Federal Disability Retirement really can be confusing to understand, but we’re here to educate all federal employees on the benefits that they are entitled to.

Hannah: Don’t forget that you have three options for your TSP, three options for your Survivor annuity, and you can continue to work. You must request a reasonable accommodation to have the strongest Federal Disability Retirement case.

Kyleigh: We understand that applying for Federal Disability Retirement is a huge step for most employees, which is why we provide expert guidance. Our familiarity with Federal Disability Retirement, the OPM, and agency involvement has changed nearly 6,000 lives.

If you’ve still got questions, or you’d just like to walk through it together 1 on 1, give us a call today to set up a free consultation.